Morning Lineup – Mixed Data on Jobs

Happy July 4th! US futures are indicating a higher open this morning ahead of the holiday-shortened session. Treasury yields are lower, and the latest data hasn’t really done much to halt that slide. Mortgage applications slid, Private Payrolls released by ADP were weaker than expected, and Jobless Claims were only slightly lower than forecasts. There’s still a lot more data left on the calendar, though. Factory Orders, Durable Goods, and the ISM Services report will all be released at 10 AM Eastern. Stay tuned.

Read today’s Morning Lineup to get caught up on news and stock specific events ahead of the trading day, as well as updates on the latest Services PMI data around the world.

Bespoke Morning Lineup – 7/3/19

As mentioned above, the ADP Private Payrolls report missed expectations this morning coming in at a level of 102K versus forecasts for 140K. This month’s weaker print follows an even weaker reading of 41K last month. That takes the two-month rolling total of growth in private payrolls growth to 143K, which is the weakest two-month rate of growth since April 2010. Two months may not necessarily make a trend, but Private Payroll growth has fallen out of the longer-term range that it was in.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Morning Lineup – No Fireworks Yet

Quiet is the word this morning. There are no major economic reports on the calendar, no major earnings releases, and little in the way of volatility in overseas markets. China and Japan were basically flat overnight, most of Europe is little changed, and the yield on the 10-year Treasury is unchanged from yesterday. Even bitcoin is down just 4% after several days of 10%+ daily moves. The only major news headlines concern tariff threats (what else is new), but this time on European imports, and then talk that Saudi Aramco is looking to revive the IPO process.

Read today’s Morning Lineup to get caught up on news and stock specific events ahead of the trading day, as well as updated charts on the technical state of the market.

Bespoke Morning Lineup – 7/2/19

One indicator we track in order to asses the internal health of the market is the percentage of S&P 500 stocks hitting 52-week highs on a daily basis. In June, there were two days where the daily percentage of stocks hitting new highs clocked in at a healthy 20%, but in yesterday’s rally to new highs, the percentage of stocks that hit new highs only got as high as 11.9%, which is a relatively weak reading for a day when the S&P 500 breaks out to all-time highs. Going forward, we will be looking for stronger readings, especially on a positive market day like Monday.

In terms of the percentage of stocks in the ‘pipeline’ for new highs, the chart below summarizes where S&P 500 components finished yesterday relative to their 52-week highs. 20% of S&P 500 components are currently within 2% of a 52-week high (red bar), while another 21% are more than 2% but less than 5%, so on a strong market day there is certainly the potential for new highs to surge, but with futures indicating a slightly lower open, it’s unlikely we will see that surge today.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Morning Lineup – And They’re Off!

It’s hard to imagine a stronger way to start off the second quarter as US equities and risk assets around the world are surging following what is being billed as a cease-fire in the US-China trade war and President Trump’s meeting with North Korean leader Kim Jung-Un over the weekend.

While the news surrounding trade has been positive, the reality on the ground remains less optimistic. Manufacturing PMIs for the month of June continued to show weakness around the world, and this morning’s ISM Manufacturing report for the US will kick off a busy week of economic data in the US that will go a long way in determining whether the market is correct in its pricing of 100% certainty that the FOMC will cut rates at the end of the month.

Read today’s Morning Lineup to get caught up on everything you need to know ahead of the new trading day including a recap of overnight trading in Asia and Europe as well as a rundown of all economic data released.

Bespoke Morning Lineup – 7/1/19

The S&P 500 SPY ETF is set to gap up more than 1% this Monday morning, so we wanted to highlight a few stats surrounding similar types of moves.

Since 1993 when SPY began trading, there have been 255 gaps up of 1%+, which accounts for 3.8% of all trading days. On these 255 days, SPY has averaged a further gain of 0.20% from the open to the close of trading after the initial jump at the open.

Today is also a Monday morning, and there have been 49 Monday mornings since 1993 in which SPY began the trading week with a 1%+ jump at the open. On these 49 Mondays, SPY has averaged a further gain of 0.18% from the open to the close of trading. Notably, though, returns one week from the open following Monday gaps up of 1% have been poor, with SPY down an average of 1.12% five days later.

It’s also the first trading day of the month. Since 1993, SPY has gapped up 1%+ on the first trading day of the month 16 prior times, which is about 5% of the time. The average open to close change on these days has been positive at +0.34%.

And what about Monday gaps up of 1%+ to start a new month? That has happened 9 times since 1993, which is 7.4% of the time. On these 9 trading days, SPY has basically been flat from the open to the close of trading.

Finally, there have been just 4 starts to a new quarter that have seen 1%+ gaps higher at the open for SPY, and on these 4 days, SPY has continued higher from open to close twice (50%). Five days later, though, SPY has been higher every time.

Today would be the first time in its history that SPY has gapped up 1%+ at the open on the first trading day of July.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Morning Lineup – Partying Like it’s 1995

Why party like it’s 1999, when you can party like it’s 1995 instead? With futures indicated higher on the day, the S&P 500 is on pace to finish the first half with a gain of over 18%, while long-term US Treasuries are flirting with a gain of over 10% on the year. Heading into the last trading day of the half, the major focus is obviously on the weekend meeting between President Trump and President XI. Expectations are low heading into the meeting, but we should have a better idea of how things are going to play out as the day goes on and into tomorrow. To bad Xi doesn’t have a Twitter account too!

While China trade talks are a major issue, there is also a decent amount of economic data to contend with today and into next week. Then, after the July 4th weekend, we’ll start to kick off second-quarter earnings season.

Read today’s Morning Lineup to get caught up on everything you need to know ahead of the new trading day including a recap of overnight trading in Asia and Europe as well as a rundown of all economic data released.

Bespoke Morning Lineup – 6/28/19

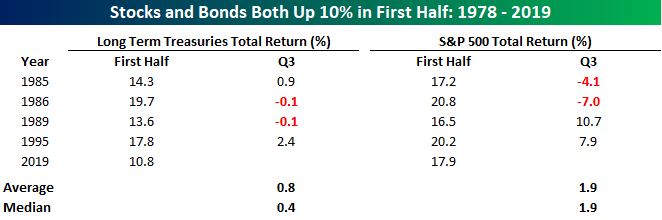

As mentioned above, 2019 is on pace to be the first year since 1995 where both long-term Treasuries (as measured by the Merrill Lynch Long-Term Treasuries Total Return Index) and the S&P 500 were up more than 10% in the first half of the year. Going back to 1978, this is also only the fifth year where both saw double-digit gains in the first half.

In the table below, we highlight each of those five years and show the performance of both asset classes in Q3. In the case of both asset classes, Q3 saw middling returns with periods of positive and negative returns evenly split.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Morning Lineup – Conflicting Headlines

Dow futures are under a bit of pressure this morning due to weakness in Boeing (BA), which is trading down nearly 3%. S&P 500 and Nasdaq futures, meanwhile, are both indicating a positive open although they too are off the highs of the overnight session. The more optimistic tone earlier was due to some positive headlines regarding this weekend’s meeting between President Trump and President Xi, but some of the air was let out of the balloon following a less optimistic tone from the WSJ.

Please read today’s Morning Lineup to get caught up on everything you need to know ahead of the new trading day including the latest news on trade, Sentiment among Korean businesses and in the EU, as well as the latest on the Brexit saga.

In economic news, GDP was slightly worse than expected (3.1% vs 3.2%), while Jobless Claims were a bit higher than expected (227K vs 220K expected).

Bespoke Morning Lineup – 6/27/19

Semis have been one of the most negatively impacted groups from all of the trade disputes between the US and China, but yesterday the group got a reprieve on the back of Micron’s (MU) big 13%+ gain. Overall, the Philadelphia Semiconductor Index (SOX) rallied over 3%, and while the S&P 500 sold off in the afternoon, semis managed to hold up much better. In fact, all 30 stocks in the SOX traded higher yesterday, which was the fourth time this month that we have seen every stock in the index trade higher on the same day.

While there have now been four days this month where every stock in the SOX traded higher on the day, there hasn’t been a single day where every stock traded lower. Going back to 2009, this is only the second month where we have seen a net of at least four days where breadth in the SOX was 100% positive. The one other month was back in July 2009 in the early stages of the bull market. Conversely, there has only been one month in the last ten years where there was a net of four days where every stock in the SOX traded down on four separate days in the same month. That month was March 2018 when the index also saw its high for 2018.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Morning Lineup – Trade Optimism Bubbles Up Again

US equities are attempting to get back on track this morning after three straight days of declines. Futures are currently indicated to erase about half of yesterday’s decline as sentiment regarding this weekend’s trade talks between the US and China was given a boost following some comments from Treasury Secretary Steve Mnuchin. Whether there is really anything to those comments remains to be seen.

Please read today’s Morning Lineup to get caught up on everything you need to know ahead of the new trading day including the latest news on trade, Asian markets, and confidence in Germany.

Bespoke Morning Lineup – 6/26/19

After hitting a new all-time high on Thursday, the S&P 500 comes into today having had three straight daily declines. Looking back over history this is not a very common occurrence. As we highlighted in The Closer last night, going back to 1928, there have only been 11 other periods where the S&P 500 closed at a 52-week high (after not having done so in the prior four weeks) only to follow it up with three straight days of declines.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.