Oct 21, 2022

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“In the history of every great catastrophe, you will find that some masterly bit of stupidity sets fire to the oil-soaked rags.” – Edwin Lefèvre

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

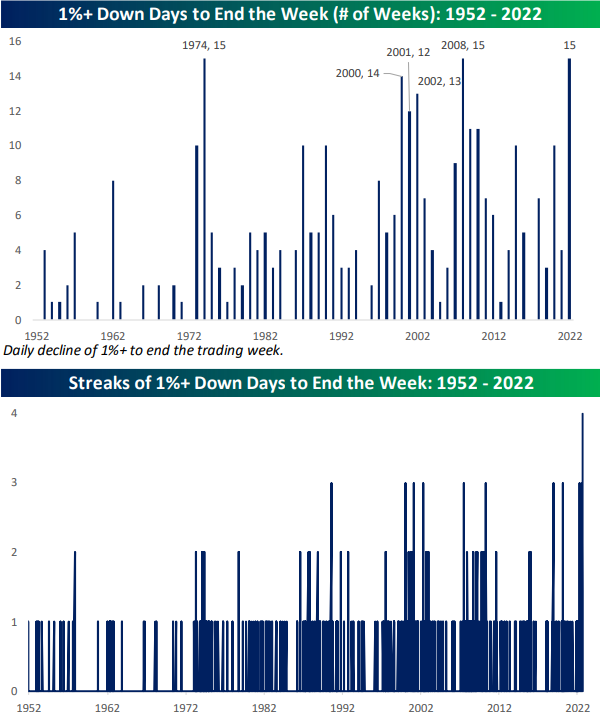

It’s Friday, so yes, US equity futures are down. As shown below, the S&P 500 has already seen 15 weeks end with a 1%+ down day in 2022, which is tied for the record seen back in 1974 and 2008. A 1%+ down day today would make it a record 16, and there are still 10 weeks left in the year! Keep in mind that we’ve also seen four straight weeks end with a 1% down day coming into this week, which would extend to five if the S&P indeed falls 1%+ again today.

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Oct 20, 2022

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“It is clearly now the will of the parliamentary Conservative Party that there should be… a new prime minister.” – Boris Johnson 7/7/22

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

Just over three months ago, Boris Johnson resigned as UK PM, and now this morning, his successor, Liz Truss, just announced she will be stepping down as PM. Do you think she had enough time even to unpack her bags? After trading lower throughout most of the night, S&P 500 futures had flipped modestly into positive territory this morning, but in the immediate aftermath of the resignation announcement, they pulled back closer to unchanged while Nasdaq futures are lower. Treasury yields have been behaving with nothing more than modest moves higher in yields across the curve. Crude, however, is rallying an additional 2%+ and back above $87 per barrel while copper is also up over 2%. Over in China, there was some positive news that the country is considering a reduction of the required quarantine time required for travelers in the country.

Here in the US, the general trend in earnings remains primarily positive, but there have been some duds. Tesla (TSLA) is trading lower after reporting weaker-than-expected sales raising concerns over demand, and Allstate (ALL) dropped over 10% after announcing Q3 catastrophe losses of $673 million. Lastly, Alcoa also reported weaker-than-expected EPS and sales and lowered forecasts for shipments, but anyone following the company over the years knows that it is hardly a bellwether.

In economic data this morning, Initial Jobless Claims came in lower than expected (214K vs 233K) while Continuing Claims were only slightly higher than forecasts (1.385 million vs 1.378 million). Also, the Philly Fed Manufacturing report for October improved less than expected rising from -9.9 to -8.7 versus forecasts for a reading of negative five.

This week’s equity market performance has been the opposite of the pattern we have seen this year. Heading into the week, the S&P 500 has averaged negative returns on every weekday this year except Wednesday when the average gain has been 0.20%. This week, the only down day (so far) was Wednesday, and on Monday and Tuesday, the S&P 500 was up well over 1%. While it’s still early, equity futures are once again modestly positive heading into Thursday’s trading. There’s still plenty of time left in the week but wouldn’t that be a welcome trend?

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Oct 19, 2022

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“It’s the nearest thing to a meltdown that I ever want to see.” – John Phelan, NYSE Chairman (1987)

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

35 years ago today, US stocks experienced their largest single-day decline in history as the Dow dropped 22.6%. Back then, before most Americans had 401Ks, the stock market wasn’t nearly as enmeshed in the lives of Americans as it is today, but the plunge still was THE story of the day prompting questions over whether it was a repeat of 1929 and the depression that followed. With the benefit of time and hindsight, the market and economy quickly moved on from the 1987 crash, and it barely even registers as a blip on long-term stock charts. Since the close on 10/19/87, the S&P 500 has had an annualized total return of 10.71%. Even more notable, though, is that had you invested in the S&P 500 on the Friday before the crash, you’re annualized total return over that span would have still been just short of 10% (9.99%). Not bad for the worst-timed trade of all time.

Moving to the present day, 2022 has actually been worse than 1987. After the crash in 1987, the S&P 500 was down less than 8% YTD. Today, even after a gain of nearly 4% over the last week, the S&P 500 is down more than 20% YTD or twice the decline of the S&P 500 at this point in 1987.

This morning, futures are in the red after trading higher overnight as yields surge with the 10-year nearing 4.10%. Building Permits and Housing Starts were just released and came in mixed relative to expectations with starts missing forecasts while starts came in a bit higher than forecast. Mortgage applications continue to decline, though, suggesting that the sector will continue to face pressure.

It’s now been a week since the S&P 500’s closing low on 10/12 (the intraday low was on 10/13), so we wanted to take a bird’s eye look at where things stand at the index and sector level. Of the Russell 2000 (IWM), Nasdaq 100 (QQQ), and S&P 500 (SPY), IWM probably looks best from a technical perspective. Of the three indices shown, it is the only one that didn’t violate the June lows on a closing basis and is also the only one that made a higher high even if it was just on an intraday basis. For both QQQ and SPY, the charts look very similar as last week’s lows represented lower lows, and the rally over the last few days has yet to make a higher high.

At the sector level, Financials have been leading the charge, rallying more than 6% over the last week. Of the remaining ten sectors, the only one not up more than 2.5% is Utilities. Despite the gains from the last week, though, the only sector that has managed to retake its 50-day moving average is Energy, and four sectors (Technology, Real Estate, Consumer Discretionary, and Utilities) still remain at oversold levels.

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Oct 18, 2022

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Though I am often in the depths of misery, there is still calmness, pure harmony and music inside me.” – Vincent Van Gogh

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

Stock futures are pointing sharply higher for the second day in a row this morning. While there are no specific catalysts, better-than-expected earnings against a backdrop of extremely oversold markets provide fuel for at least a short-term rally. Sentiment towards the market has been very negative as well. The latest example is the BofA Fund Manager Survey which showed the highest allocations to cash since 2001. Despite the rally in stocks, bonds are behaving as Treasury yields are modestly lower. In the commodities space, crude oil is little changed while gold is down modestly.

In the stock market lately, it’s either the end of the world or the beginning of a new bull market. In yesterday’s rally, the S&P 500’s net advance/decline (A/D) reading came in at +455 which followed a reading of negative -442 on Friday and +438 Thursday. With futures up nearly 2% this morning, it’s looking like another positive day of everything coming up roses (for now). We classify any day where the S&P 500’s net A/D reading is above positive 400 or below minus 400 as an all-or-nothing day. In the 1990s, all-or-nothing days were generally uncommon. There were seven years in the decade where there wasn’t more than one occurrence in an entire calendar year, and there were three with none.

As ETFs became more popular at the turn of the century allowing investors to buy or sell every stock in the index with one trade, the frequency of all-or-nothing days really picked up and peaked during the Financial Crisis when there were four straight years with more than 45. With all-or-nothing days occurring at a much more regular frequency in the last several weeks (and especially days), 2022 is giving some of those years from the Financial Crisis a run for their money. After three straight occurrences in a row (matching the total for all of 2017), the S&P 500 has now had 38 all-or-nothing days this year, putting 2022 on pace for 48. At that rate, this year would rank tied for third with 2010 trailing only 2011’s total of 70 and 2008’s total of 52.

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Oct 17, 2022

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“There is no more miserable human being than one in whom nothing is habitual but indecision.” – William James

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

A move by UK finance minister Jeremy Hunt to reverse most of the provisions of his predecessor’s ‘mini-budget’ have global equities and bond prices rallying this morning after Friday’s disappointing negative reversal. No major headlines out of China (good or bad) coming out of the country’s national party congress has also helped to contribute to the positive tone. So far, there hasn’t been much in the way of earnings flow, but earnings from Bank of America (BAC) were better than expected and the stock is trading up a bit more than the broader market. The only economic report of the day was Empire Manufacturing, and that report was weaker than expected coming in at -9.3 versus forecasts for a reading of -1.0. Given the massive swings of the last several days, what do you think an average investor’s confidence level is that the gains hold throughout the day?

For all the fireworks of the last two trading days, neither bulls nor bears really have much to show for it. On Wednesday, the S&P 500 closed at 3,577; by the week’s end, the S&P 500 was just six points higher at 3,583. In between those six points, though, there were some historic swings in equity prices. On Thursday, the S&P 500 gapped down over 2% but then quickly erased those losses before noon and kept rallying throughout the afternoon to finish up over 2.5%. On Friday, it looked as though bulls were going to get some follow-through as the S&P 500 rallied more than 1% in early trading. The positive momentum was fleeting, though, and within an hour of the highs, all the gains were erased, and by the end of the day, equities shed another 2.4% erasing nearly all of the prior day’s gains. In the span of two days, the S&P 500 had two extremely rare reversals in completely opposite directions.

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Oct 14, 2022

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Just before you break through the sound barrier, the cockpit shakes the most.” – Chuck Yeager

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

Let the games begin. Today marks the unofficial start to earnings season as the major banks come out of the gate with what have generally been positive results. Of the seven banks reporting, five exceeded EPS forecasts, one (Morgan Stanley) missed and one was inline (US Bancorp). Besides the Financials, UnitedHealth (UNH) also reported and topped forecasts on both the top and bottom lines. It’s still early, but so far, no major disasters. JPMorgan Chase (JPM) is even poised to trade higher in reaction to earnings which, if it holds, would be something it hasn’t done in over two years!

Outside of earnings, it’s a busy day for economic data this morning with Retail Sales (mixed relative to expectations), Import Prices (lower than expected), Business Inventories, and Michigan Sentiment all on the docket between now and 10 AM. If that wasn’t enough, we’ll also hear from three different Fed officials (George, Cook, and Waller). So much for a quiet Friday.

In international news, the German economic ministry said that a recession likely started in Q3 and will last for three quarters. The political situation in the UK continues to be a mess as PM Truss will reportedly reverse her tax plans and allow the corporate tax rate to increase while at the same time sacking her finance minister. That news has pushed the yield on the 10-year gilt down 23 bps and below 4%.

US Futures are still in positive territory, but they are well off their highs, and if the last several weeks have told us anything, it’s that where the market starts the day and where it finishes usually varies widely.

75 years ago today, Chuck Yeager accomplished the ‘impossible’ becoming the first pilot to ever break the sound barrier. Up until that time, the thought among ‘experts’ was that once an aircraft approached the speed of sound it would break apart resulting in the death of the pilot. Not really the way anyone wants to go out. Yeager proved the experts wrong, but in the moments leading up to that point, he remarked that the cockpit of the aircraft starts to shake violently.

Based on Yeager’s description, the market looks like it’s trying to break its own sound barrier. After trading up over 1% in pre-market trading yesterday, the stronger-than-expected CPI erased all the gains and more. Shortly after the open, the S&P 500 had dropped nearly 4% from its pre-market highs before staging an epic rally of over 5%. Even in this ‘all or nothing’ type of market environment, reversals of that magnitude are rare.

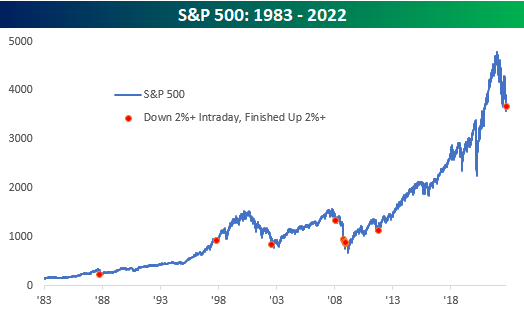

As shown below, prior to yesterday there were only nine other days since 1983 when the S&P 500 fell more than 2% intraday but finished the day up over 2%. The most recent occurrence was over eleven years ago on 10/4/11 and before that, there were five separate occurrences in 2008 alone! The three remaining reversals were in 2002, 1997, and 1987.

We’re not sure when or where the ultimate bottom in stocks will end up, but violent moves like yesterday tend to occur closer to lows than highs. It’s easy to remember the good parts of a bull market where stocks rally, but people usually forget that long-term rallies emerge out of chaos where investors become increasingly convinced that the only viable path if any exists at all, is lower. The early days of bull markets feel like anything but a sure thing.

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.