Oct 28, 2022

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“We have never said that we’re perfect. We’ve said that we seek that. But we sometimes fall short.” – Tim Cook

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

We’re seeing another day this morning where Nasdaq futures are much weaker than the broader market. The culprit this morning is Amazon.com (AMZN) which is trading down over 13% after dropping as much as 20% in after-hours trading. The Nasdaq is indicated to open down over 1% while the S&P 500 is down by about half that. Treasury yields are higher this morning, and the 10-year yield briefly traded back above 4% before falling following the latest batch of economic data. Another factor contributing to the weakness in the tech sector is a report that the Biden Administration is considering adding additional restrictions on technology exports to China.

It’s been a busy morning of economic data and the Employment Cost Index (+1.2%), Personal Income (+0.4%), and PCE Prices (+0.3%) were all in line with forecasts. Personal Spending (+0.6%) was higher than expected, and at 10 AM we’ll get Pending Home Sales and Michigan Confidence.

What a month it has been for the Energy sector. Since its recent low in late September, the S&P 500 Energy sector has rallied about 30% and is currently within 4% of its early June high. Looking at a longer-term chart of the sector shows that it has consistently found support at the trendline that extends back to the higher low it made in late 2020. The fact that it managed to bounce at that support during the last leg lower was impressive given that it followed what was a lower high for the sector in late August.

With its gain of over 60% YTD, Energy has trounced the market on a YTD basis, and while the sector has yet to take out its high from June, its performance gap with the S&P 500 did manage to make a new high yesterday as it’s now outperforming the S&P 500 by 80 percentage points YTD.

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Oct 27, 2022

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“You should welcome a bear market, since it puts stocks back on sale.” – Jason Zweig

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

It’s a very mixed picture for equity futures this morning with the Dow indicated up pretty sharply while the Nasdaq is down by a similar magnitude driven in large part by shares of Meta Platforms (META) which is down over 20% and struggling to hang on to triple-digits. The ECB just announced its policy decision and hiked rates by 75 bps (as expected). Here in the US, we have a busy morning of economic data, plus big earnings reports from Amazon.com (AMZN) and Apple (AAPL) after the close.

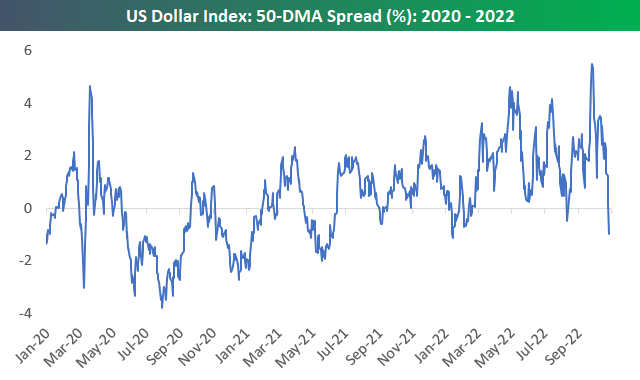

The US Dollar index peaked about a month ago, and its move lower has coincided with the bounce that we’ve seen in US equity indices. The same trend has played out over a shorter one-week time frame as well, which you can see in the Trend Analyzer snapshot below. Over the last five days, the US Dollar Bullish ETN has fallen 2.8% and broken below its 50-day moving average. At the same time, every other area of financial markets has moved higher within its trading range.

Yesterday, the US Dollar Index broke below its 50-DMA for the first time since August, and it traded the farthest below its 50-DMA since early January. As shown below, the August break did not last long, as the Dollar’s uptrend resumed almost immediately.

This morning the Dollar is back up, and a resumption of its uptrend will almost assuredly coincide with a resumption of the equity market’s downtrend. We’ll certainly be keeping an eye on FX today.

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Oct 26, 2022

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Solving big problems is easier than solving little problems.” – Google Co-Founder Larry Page

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

Bulls have finally seen some green over the last couple of weeks. In fact, the S&P 500 has gained 1%+ on six of the last nine trading days. Below is a log chart of the S&P 500 since 1952 (when the 5-day trading week began) with red dots showing prior times the index has gained 1%+ on six of the prior nine trading days (the first occurrence in at least three months). As you can see, it is not common, and aside from the occurrence in March of this year, prior periods where this happened saw massive gains over the next six and twelve months.

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Oct 25, 2022

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“There are a lot of mistakes made in games. That one just happened to be more visible than some of the others.” – Jim Marshall

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

58 years ago today, Vikings defensive end Jim Marshall recovered a 49ers fumble and ran it back to the endzone for a defensive touchdown. At least he thought it was. Unfortunately for Marshall, he ran into the wrong endzone turning what he thought was a Vikings touchdown into a safety. The Vikings still ended up winning the game, so the only people potentially impacted by Marshall’s bonehead play were the gamblers.

Less than two weeks ago, the S&P 500 closed at a new low for the year the day before what was widely anticipated as the most important economic report in weeks with the release of the September CPI on 10/13. That report was a ‘big play’ for the bears as both the headline and core readings came in higher than expected, and the y/y core reading hit a new cycle high of 6.6%. Stocks opened the day of the 13th sharply lower, and bears continued to run with it from there. Like Jim Marshall, though, they went the wrong way! The S&P 500 finished the day of the 13th up 2.6% and is now up 6.3% from its closing low on 10/12.

Despite the rally, 2022 is still a blowout as the S&P 500 remains down over 20% YTD with the Nasdaq down nearly 30%, so, like the “Purple People Eaters” of the early 1960s, the bears can still laugh about the wrong way move. The chances for Bulls this year are still slimmer than they are of Lloyd Christmas ending up with Mary Swanson, but stranger things have happened. Back in Super Bowl LI, the Falcons were up 28-3, and we all remember how that one ended. So “there’s a chance” however slim it may be.

The ‘wrong way rally’ has taken a breather this morning as futures are moderately lower ahead of a relatively busy day for economic data with Case Shiller housing numbers at 9 AM and then Consumer Confidence the Richmond Fed report at 10 AM. With the weakness in equities, treasury yields are lower and crude oil is down about 1%. The pace of earnings reports has really picked up steam and the results this morning have been somewhat lackluster. Of the nearly 40 reports so far this morning, 64% have exceeded EPS forecasts, and 62% of exceeded revenue estimates. Also slightly more companies have lowered guidance than raised it. The first big test of the earnings season will start after the close, though, when Alphabet (GOOGL) and Microsoft (MSFT) report after the close.

It seems as though this year stock prices have been driven entirely by interest rates, but a close look shows that in recent weeks that hasn’t entirely been the case. Take a look at the chart of the S&P 500. While it briefly broke below its June lows in late September and early October, it has recently rebounded and yesterday actually closed more than 3% above its June low.

If interest rates were the primary driver of stock prices, given where the S&P 500 is trading, you would expect to see the US Treasury yields right around or maybe even below the levels it was at in mid-June. That hasn’t been the case though. Take the 10-year yield, for example. At the S&P 500 lows in June, the yield on the 10-year peaked at 3.47%. It eventually fell back down to as low as 2.57% in early August, but since then has surged right through the June highs all the way up to yesterday’s high of 4.27%, or 80 basis points more than the June high. The fact that equities have been able to hang in relatively well despite the surge higher in yields suggests that stocks may be starting to look past the pressure from higher rates.

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Oct 24, 2022

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Diversity in the world is a basic characteristic of human society, and also the key condition for a lively and dynamic world as we see today.” – Hu Jintao

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

It’s been a roller-coaster morning for US equity markets since futures opened for trading last night. After opening sharply higher, futures drifted lower all morning before bottoming out between 4 AM and 6 AM eastern time. Investors remain optimistic following Friday’s surprise WSJ ‘leak’ of the potential for a Fed pause to rate hikes later this year. While the Fed is moving markets this morning, earnings are likely to take a more front-and-center role this week as more than 150 S&P 500 companies are set to report this week, including the largest companies in the index. On the economic calendar, the only reports of note are the Chicago Fed National Activity Index and the flash S&P Manufacturing PMI.

While free markets are all rallying this morning, the same can’t be said for Chinese markets where Xi’s consolidation of power at the national party congress after his predecessor Hu Jintao was unceremoniously escorted out has investors running for the exits. Hu Jintao may have said in his comments that he advocated for diversity, but Chairman Xi has consolidated power into a tight group composed entirely of loyalists to his views. The KraneShares CSI China Internet ETF (KWEB) is trading down below $20 per share today to all-time lows and is down 82% from its all-time high in February 2021. That’s an even larger drawdown than the Nasdaq had from the dot-com bust!

Today’s new low in the KWEB comes from what is poised to be a 12.5% decline at the open, which, if it holds up through the close, would be the largest single-day decline in the ETF’s history going back more than 20 years!

The Chinese currency has also been under considerable pressure lately. In today’s trading, the renminbi exchange rate rose above 7.26 which is the weakest level since January 2008, taking out the lows seen in the year leading up to COVID when President Trump began the trade war with the country.

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Oct 21, 2022

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“In the history of every great catastrophe, you will find that some masterly bit of stupidity sets fire to the oil-soaked rags.” – Edwin Lefèvre

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

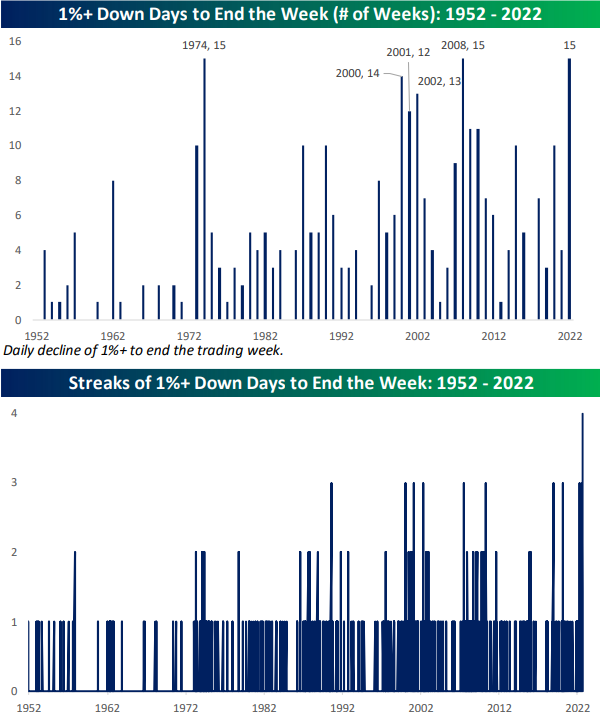

It’s Friday, so yes, US equity futures are down. As shown below, the S&P 500 has already seen 15 weeks end with a 1%+ down day in 2022, which is tied for the record seen back in 1974 and 2008. A 1%+ down day today would make it a record 16, and there are still 10 weeks left in the year! Keep in mind that we’ve also seen four straight weeks end with a 1% down day coming into this week, which would extend to five if the S&P indeed falls 1%+ again today.

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.