Jan 19, 2023

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Be brutally honest about the short term and optimistic and confident about the long term.” – Reed Hastings

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

We continue to follow closely an emerging trend of “misses” when it comes to companies that have reported earnings so far this season.

In the year leading up to the current earnings season that began last week, our Earnings Explorer shows 8,424 individual quarterly earnings reports. Of those 8,424 reports, 67% reported EPS that were better than consensus analyst expectations, while 70% reported sales that were better than expected. So far this season, which began last Monday, we’ve seen just 40% of companies beat consensus EPS estimates and just 34% beat consensus sales expectations.

It’s still very early in the reporting period, but so far it looks like analysts — who were already cutting estimates at a rapid pace leading up to this earnings season — may not have cut forecasts enough.

By the end of next week when another 200+ companies will have reported, we’ll have a much firmer look at where beat rates stand this season. Below is a look at the rolling 3-month average of beat rates for both EPS and sales throughout the history of our Earnings Explorer.

After COVID hit, beat rates initially skyrocketed as analysts became overly pessimistic, but we’ve seen downside mean reversion in beat rates for the last 18 months or so. Based on early trends, we could see a return down to the long-term average this quarter, or even a move below average. Over the last 22 years going back to 2001, 59.4% of stocks reporting have beaten EPS estimates, while 56.45% have beaten revenue estimates. As mentioned earlier, we’ve seen a 40% beat rate for EPS so far this season and a 34% beat rate for revenues. We’d note that the only time we saw EPS beat rates fall to the low 50s over a three-month period was in Q1 2009 near the depths of the Financial Crisis lows.

Continue reading today’s Morning Lineup with a new Bespoke Premium trial.

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Jan 18, 2023

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“It seems like people don’t learn from the past.” – Thomas Peterffy

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

Earnings so far this week have been pretty negative, with 10 of the 16 stocks that have reported missing EPS estimates. We won’t get a good read on things until next week when the pace of reports picks up dramatically, but it’s not common to see more EPS misses than beats.

As we highlighted in last night’s Closer, the iShares Europe ETF (IEV) has outperformed the S&P 500 (SPY) over the last three months by the widest margin on record since IEV began trading in 2000. European equities are trading slightly higher once again this morning along with US futures.

As shown below, the charts for European and other international index ETFs now look drastically different than those of the S&P (SPY) and the Nasdaq 100 (QQQ). While SPY and QQQ have yet to break out of long-term downtrends, Europe (IEV, FEZ), emerging markets (EEM), and the all world ex-US ETF (CWI) have formed new uptrends as they break out to six-month highs.

Continue reading today’s Morning Lineup with a new Bespoke Premium trial.

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Jan 17, 2023

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Every once in awhile, you do have a bad day.” – Adam Vinatieri, retired placekicker who holds the NFL career points record.

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

In Friday’s Morning Lineup, we noted the weak pre-market action in stocks that had just reported earnings. A number of key banks and brokers reported Q4 earnings on Friday and initially sold off on the news ahead of the open. But we actually saw nice intraday reversals once the opening bell rang.

Amazingly, of the nine stocks that reported earnings on Friday morning, all nine opened lower when trading began at 9:30 AM ET, and all nine also traded higher intraday from the open to the close. It’s rare to see such a big intraday turnaround across the board.

We’ll be monitoring earnings results closely over the next month or so, but so far since the new year began, numbers have been solid. As shown in the snapshot from our Earnings Explorer, 71% of companies have beaten EPS estimates to start 2023, while 67% have beaten sales estimates. The average stock that has reported has gained 1.31% on its earnings reaction day as well.

This morning both Goldman Sachs (GS) and Morgan Stanley (MS) reported their quarterly numbers, and of the two, MS had the stronger report with a nice revenue beat. Goldman, on the other hand, missed sales expectations due to weakness in investment banking and asset management. The stock is currently trading down 2.4% in pre-market trading. That’s an anomaly for Goldman actually, which has managed to open higher on nine of its last ten earnings reports. The only other time Goldman has opened lower on earnings since mid-2020 was following its January report last year when it gapped down 5.49% at the open. That day the stock continued lower by another 1.57% from the open to the close of trading.

Continue reading today’s Morning Lineup with a new Bespoke Premium trial.

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Jan 13, 2023

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“We ended the year on a strong note growing earnings year over year in the 4th quarter in an increasingly slowing economic environment.” – Brian Moynihan

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

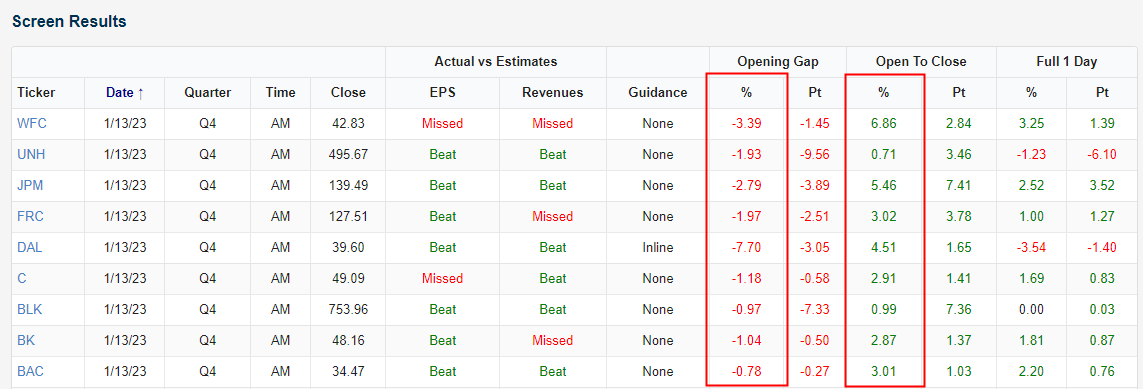

Earnings season has arrived, and it has made its presence known with a thud. Of the eight major reports this morning, all but two (Citigroup and Wells Fargo) beat EPS forecasts, and only two (Bank of New York and Wells Fargo) reported weaker-than-expected revenues. The results don’t appear good enough for investors, though. Six of the eight companies that reported are trading down in the pre-market, and the two trading higher (Bank of New York and BlackRock) have seen just muted gains. On the flip side, stocks trading lower in the pre-market have all declined at least 1%, while Wells Fargo and Delta head into the opening bell with declines of over 4%. Given the weak reactions to earnings, overall equity index futures are also weak and indicating a decline of nearly 1% at the open. Interestingly, despite the fact that none of the major reports have been related to technology, it’s the Nasdaq that is doing the worst in the pre-market with a decline of over 1%

The fact that these companies have seen their share prices initially react negatively to their reports is a bit of a letdown but remember that collectively they have performed well to start the year. Except for UNH, all the stocks are positive YTD with gains of at least 3.5%. Heading into this morning’s report, DAL had rallied more than 20% YTD, so a pullback in response to earnings is completely understandable. UNH, though, is another story. Through yesterday’s close, the stock was already down 6.5% YTD and in oversold territory, so the bar didn’t look especially high to begin with.

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Jan 12, 2023

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“What weather they shall have is not ours to rule.” – J.R.R. Tolkien

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

In weather-speak, they call an atmosphere like this morning, the calm before the storm. Overnight in Asia, stocks were little changed and that was almost literally the case with the Nikkei rising just 0.01%. Chinese stocks were a little more biased to the upside with a gain of 0.20%. In Europe, the mood is considerably better as major benchmark indices in the region are all up over 0.50%. Bond yields in the US are modestly higher, and both crude oil and natural gas are higher after the latter attempts to bounce from 52-week lows reached on Tuesday following a massive three-week decline.

None of these moves really matter, though, as the 8:30 release of the December CPI – “the most important economic release in generations” – will dictate the tone of the trading day. With the President scheduled to speak on inflation later this morning, there is some speculation that the White House got an early look at the report and is looking to spike the ball on the administration’s policies to combat inflation.

If there’s one place where hyperbole rules, it’s in discussions pertaining to the market. We would argue, though, that the recent moves in natural gas may not have been talked about enough given how large the declines have been relative to history.

Let’s start with the short-term. Over the 15 trading days ending yesterday, natural gas dropped 36.9%. That alone is one of the most extreme downside moves in the history of the contract, but a week ago today, the 15-day decline was 46.4% which was the most extreme downside move on record (since 1990).

From a longer-term perspective, the declines have been just as large. In the 100 trading days ending Wednesday, the front month natural gas future declined 59.8% which also ranks as the most extreme downside move on record. The only other times there were declines of a magnitude in the ballpark of the current drop were in 2001 and 2006.

The scatter chart below compares the 15-day rate of change (x-axis) in natural gas prices to the 100-day rate of change (y-axis). The highlighted section at the bottom left with the most extreme downside moves over both a 15- and 100-day period all occurred so far in 2023. Whereas most other large 15-day declines followed periods when natural gas prices were up over the prior 100 trading days, the current period has been a snowball of weakness on top of weakness.

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Jan 11, 2023

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“It is easy to quit; I’ve done it at least a hundred times.” – Unknown

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

Flights across the US are grounded due to an outage at the FAA, but stocks remain airborne as futures are modestly higher across the board, and the Nasdaq is looking to extend its winning streak to four straight days. News flow looks to be relatively light as there are no major economic reports on the calendar, and the only earnings report is KB Home (KBH) after the bell. Tomorrow will be the big day of the week, though, when the December CPI will be released at 8:30. Then, on Friday we’ll start to get the first of the big earnings reports from the major banks.

Back on this day in 1964, the US Surgeon General issued a report on smoking that was thought to be so damaging to the tobacco industry that he waited until a Saturday when markets were closed to release it to limit the potential stock market chaos. The day after the report was released it was front page top of the fold news in the New York Times with a headline reading “Cigarettes Peril Health” and the sub-headlines “Cancer Link Cited” and “Smoking Is Also Found Important Cause of Bronchitis”. Besides the front-page headlines, the Sunday edition was rife with stories on the ‘revelation’ that smoking wasn’t good for you.

As much as the tobacco companies tried for decades to convince consumers otherwise, anyone with a minimal amount of intelligence who had ever smoked a cigarette probably already knew that it wasn’t something you did in order to get yourself into shape or good health. As far back as the 1940s, scientists had already made the link between smoking and lung cancer. Smoking was considered a vice for a reason! Even as many (or most) Americans already knew of the dangers of smoking, an official statement from the Federal government was a big deal, though, and would pave the way for more regulation of the sector. If you owned tobacco stocks heading into that weekend, you probably weren’t looking forward to Monday’s opening bell.

When the bell rang Monday morning, tobacco stocks opened lower, but by the end of the trading day, their performance was a surprise to most. Of the five major tobacco companies at the time, Reynolds American actually finished the day higher, and American Tobacco was unchanged on the day. Of the remaining three major tobacco stocks, none of them even finished the day down 2%. Perhaps the most amusing aspect of the New York Times market recap the following morning was that cigar stocks traded higher on the day as “cigar smoking received a relatively clean bill of health”. It looks like at least one part of the industry had effective lobbyists!

The performance of the cigarette stocks on the first trading day after the Federal Government first officially recognized the dangers of smoking illustrates once again how the market can defy consensus expectations. While the Surgeon General’s report on the dangers of smoking should have been a blow to cigarette stocks, the initial reaction to the report was muted. When everyone is zigging, the market often zags.

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.