The Bespoke Report – Go Big or Go Home

The market may abhor uncertainty, but even with an abundance of it, US equities had their best week in months. The health of the President, the progression of COVID, the ultimate outcome of the election, and the status of another round of stimulus are just a few of the issues facing investors right now, but this week the market was able to grin and bear it and push higher.

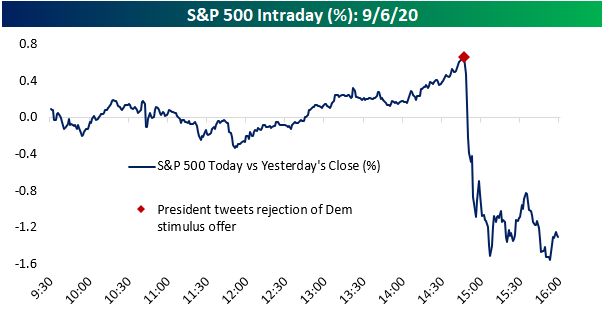

That wasn’t necessarily the case on Tuesday, though. What was looking like a good day for equities abruptly headed south after the President put the kibosh on hope for a stimulus deal when he tweeted that he had instructed “representatives to stop negotiating until after the election when, immediately after I win.” With that, the S&P 500 erased a 0.5% intraday gain and finished the day down over 1%. While the reversal was scary to watch, as we noted in our Morning Lineup on Wednesday, “while it’s often tempting to read into these types of late-day sell-offs as an early ‘tell’ for further market weakness, the summary results don’t bear that out.” By the close on Wednesday, the S&P 500 had erased all of Tuesday’s losses, only adding to those gains on Thursday and Friday.

Part of the reason for the recovery in equity prices was the fact that President Trump backtracked on his comments from Tuesday, and by Friday was tweeting and telling Rush Limbaugh that he wanted to “Go Big” with an even larger stimulus bill than the Democrats were proposing!

Where these stimulus talks end up is anyone’s guess, and we’re not sure anything even gets done, but there’s also a lot more to cover in the markets this week. We just published our weekly Bespoke Report newsletter, which covers all of the major events of the week, including the economy, sentiment, the Covid outbreak, key group performance, and the upcoming earnings season. To read the report and access everything else Bespoke’s research platform has to offer, start a two-week free trial to one of our three membership levels. You won’t be disappointed!

The Bespoke Report — October Silly Season

We got a major October surprise to close the week, and it really does feel more like silly season than a surprise. We discuss the implications of the President’s positive COVID test for both markets and the election. Speaking of November’s election, we break down the outlook based on national polling, discuss the Senate and why a split Congress might be a disaster for the prospects of fiscal stimulus, and the growing evidence (including insistence from FOMC officials) that more easing is necessary. That evidence includes this week’s jobs report and the personal income and spending numbers released earlier in the week, both of which we discuss in detail. Seasonality, international markets, co in this week’s Bespoke Report.

This week’s Bespoke Report newsletter is now available for members.

To read the report and access everything else Bespoke’s research platform has to offer, start a two-week free trial to one of our three membership levels. You won’t be disappointed!

The Bespoke Report — Equity Market Pros and Cons: Q4 2020

This week’s Bespoke Report is an updated version of our “Pros and Cons” edition as we get set for the fourth quarter of 2020.

With this report, you’re able to get a complete picture of the bull and bear case for US stocks right now. It’s heavy on graphics and light on text, but we let the charts and tables do the talking!

On page two of the report, you’ll see a full list of the pros and cons that we lay out. Each bullet point is not meant to be weighted equally, but the fact that there are more cons than pros indicates that the market is entering Q4 facing plenty of headwinds instead of having the wind at its back.

To read this report and access everything else Bespoke’s research platform has to offer, start a two-week free trial to Bespoke Premium. Enter “THINKBIG” at checkout to receive a 10% discount once the trial ends. You won’t be disappointed!

The Bespoke Report – Was It Something I Said?

This week’s Bespoke Report newsletter is now available for members. Well, it was looking like a positive week. After two strong days for the S&P 500, Wednesday was looking like a third positive day as the equity market was poised to put the sharp declines of the first two weeks of September behind it. All we had to do Wednesday was get through the Fed at 2 PM, and then it would be smooth sailing. When the Fed released its statement at 2 PM Wednesday, the market initially rallied. So far, so good. But then Chairman Powell stepped up to the podium. True to form, within 15 minutes of the start of Powell’s press conference, the S&P 500 made its high for the day and ultimately the week. By Friday, any hopes for gains this week were a distant memory.

Chairman Powell may go down as the scapegoat for this week’s sell-off, but there was nothing really new in the Fed’s statement. Some have suggested that the Fed wasn’t dovish enough in its comments, but that’s a bit of a stretch. We would put more weight on the fact that the calendar says September than anything the FOMC said.

We just published our weekly Bespoke Report newsletter, which covers all of the major events of the week, including the economy, sentiment, and the Covid outbreak. To read the report and access everything else Bespoke’s research platform has to offer, start a two-week free trial to one of our three membership levels. You won’t be disappointed!

The Bespoke Report — Momentum Matters Most

It was a rough week to own stocks as the Nasdaq 100 dragged down the broader US equity market. While the failure to introduce a new bill to continue easing fiscal policy has been ignored by markets for the most part, the breakdown of upward momentum coupled with that policy flop clouds the outlook…even as the economy is improving and the spread of COVID also eases. Broken moving averages and weak technical set-ups don’t mean markets are poised to crash, but the backdrop has gotten worse over the past week. We discuss all these items in detail along with economic data in the US and around the world, low rates in the US, and how the COVID pandemic has impacted Americans in this week’s Bespoke Report.

This week’s Bespoke Report newsletter is now available for members.

To read the report and access everything else Bespoke’s research platform has to offer, start a two-week free trial to one of our three membership levels. You won’t be disappointed!