Sep 4, 2020

This week’s Bespoke Report newsletter is now available for members.

The Nasdaq 100 was more than 30% above its 200-day moving average on Wednesday, which was the most extended it has been above its 200-day since the Dot Com boom of the late 1990s. Even after a big two-day pullback to close out the week, the Nasdaq 100 remains 22% above its 200-day. You know an index is extended when a bear market decline of 20% wouldn’t even put it below its 200-day!

In this week’s Bespoke Report, we analyze the market’s drop over the last two days and try to determine whether it’s the start of a longer-lasting correction or simply a blip within a long-term uptrend.

We also take a look at this week’s big economic releases, including Friday’s better-than-expected Nonfarm Payrolls report and the monthly ISM manufacturing and services readings for August.

We close the report with a deep dive into each of our Bespoke Model Portfolio holdings. If you want to know why we like each of the stocks in our most popular growth portfolio, this week’s report provides a detailed look.

To read this week’s Bespoke Report newsletter and access everything else Bespoke’s research platform has to offer, start a two-week free trial to one of our three membership levels. You won’t be disappointed!

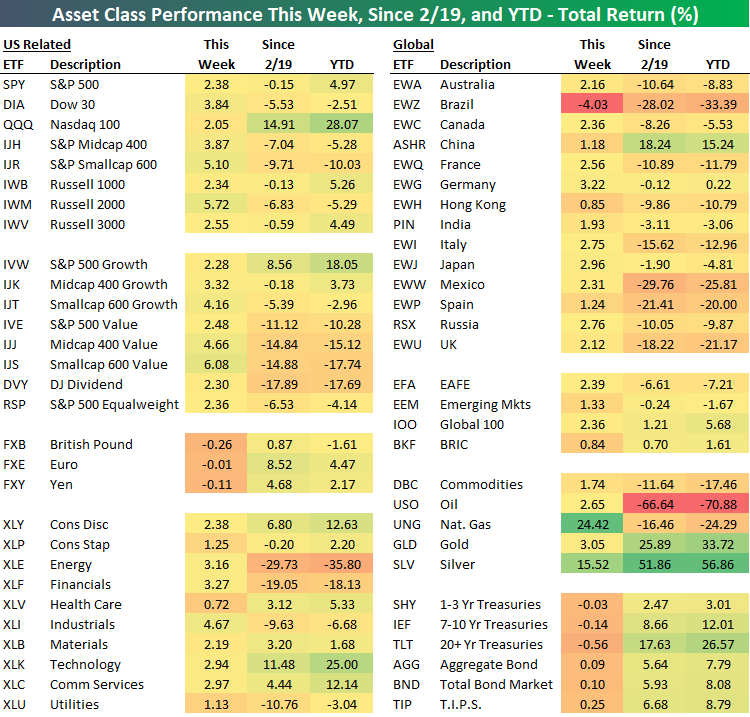

Aug 28, 2020

This week’s Bespoke Report newsletter is now available for members.

We just published our weekly Bespoke Report newsletter, which covers all of the major events of the week, including the economy, sentiment, politics, and the Covid outbreak. To read the report and access everything else Bespoke’s research platform has to offer, start a two-week free trial to one of our three membership levels. You won’t be disappointed!

Below we have updated our ETF Asset Allocation Matrix which summarizes the performance of key ETFs across the spectrum of asset classes this week, this month, and YTD.

Weeks don’t get much more positive than this one. Outside of the Utilities sector ETF (XLU) and a number of fixed income ETFs, every other ETF was up on the week. Leadership this week was centered in large caps, growth, Technology, Communication Services, and even—hold on to your hats– Financials! Among individual countries, Brazil, China, and India all traded up over 3%. Commodities were also strong on the week with all five of the ETFs tracked in our Matrix gaining more than 4%.

Looking through the various MTD performance numbers, they look more like returns you would see for an entire year! The Nasdaq 100 ETF and the Tech sector Spyder (XLK) are both up over 10% MTD. The only laggards of note have been Brazil (EWZ), Long-Term Treasuries (TLT), and the Utilities sector ETF (XLU).

Year to date, eight ETFs are up over 20%, led by Silver (SLV) which has gained more than 50%, while just three ETFs (Energy—XLE, Brazil—EWZ, and Mexico—EWW) are down more than 20%.

Aug 21, 2020

This week’s Bespoke Report newsletter is now available for members.

US large cap stocks continue to trend higher, even as small caps have retreated to support and other global equities have broken post-COVID uptrends to the downside. All is not lost, though, after an incredibly strong earnings season and with COVID retreating in the US…for now. This week we’re also watching the possibility of a double hurricane in the Gulf of Mexico, booming housing markets and the lumber they’re desperately bidding for, upticks in COVID case counts for a number of other countries, and booming e-commerce sales from major retailers. We discuss all these items in detail along with economic data in the US and around the world, new all-time highs for US stocks, and the outlook for Federal Reserve policy in this week’s Bespoke Report.

To read the report and access everything else Bespoke’s research platform has to offer, start a two-week free trial to one of our three membership levels. You won’t be disappointed!

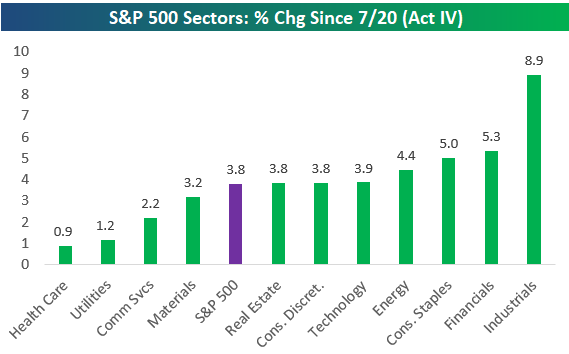

Aug 14, 2020

This week’s Bespoke Report newsletter is now available for members.

Given the rotation we’ve seen into “re-open” areas of the market since July 20th, we can now confidently say that we’re in the midst of “Act IV” of the current bull market.

Below is our chart of the S&P 500 since last December highlighting what is now a four-act bull. Act I was the strongest and led by Tech, Health Care, and Energy. Act II saw huge gains from “re-open” plays as the first wave of COVID subsided. Act III saw sideways action for the broad market but big gains from Tech/FAANG as COVID cases began to rise again. And finally, Act IV has been led once again by re-open stocks in Industrials, Transports, and Financials, while the Tech sector and “COVID Economy” stocks have taken a breather.

We cover markets and the economy in much more detail in our weekly Bespoke Report newsletter. To read the report and access everything else Bespoke’s research platform has to offer, start a two-week free trial to one of our three membership levels. You won’t be disappointed!

Aug 7, 2020

This week’s Bespoke Report newsletter is now available for members.

As shown below in our ETF Asset Class Performance Matrix, August has by all accounts come in like a bull for equities.

Every single equity ETF with the exception of Brazil (EWZ) was up this week. Top-performing ETFs overall this week were Natural Gas (UNG) and Silver (SLV) which saw gains of over 15%.

In the US, every major index ETF was up over 2% this week as small caps led the way higher as IJR and IWM both rallied more than 5%. Despite this week’s outperformance, those two ETFs are still the worst performers YTD and since the February high for the S&P 500. The Nasdaq 100 was uncharacteristically a laggard this week gaining ‘only’ 2.05%. Converse to the small caps, though, this week’s underperformance didn’t put much of a dent in the Nasdaq 100’s lead in terms of performance YTD and since 2/19.

Investors who have been waiting for value to take the lead over growth saw things move ever so slightly in their favor this week as the value-oriented ETFs in each market cap range outperformed their global peers. It was only modest outperformance, but you have to start somewhere!

Cyclical sectors led the way this week as Industrials, Financials, and Energy were the top performers as defensive-oriented sectors like Health Care, Utilities, and Consumer Staples lagged.

We discuss this week’s action across markets in our weekly Bespoke Report newsletter, including a detailed look at election trends and the moves in commodities this week. To read the report and access everything else Bespoke’s research platform has to offer, start a two-week free trial to one of our three membership levels. You won’t be disappointed!

Jul 31, 2020

This week’s Bespoke Report newsletter is now available for members.

Just when they thought Tech was out, they pulled it back in!

Since peaking on July 20th, the Tech sector and FAANG names had been experiencing some downside mean reversion. That downside action came to an end on Friday when Apple (AAPL), Amazon (AMZN), and Facebook (FB) all surged on extremely impressive earnings results.

Below is one chart from this week’s Bespoke Report that shows the strength we’ve seen from the mega-caps in 2020. As shown, the five largest stocks in the S&P 500 have collectively added $1.66 trillion in market cap this year. The other 495 stocks in the index have lost $1.61 trillion in market cap!

We discuss this week’s action across financial markets in our weekly Bespoke Report newsletter. To read the report and access everything else Bespoke’s research platform has to offer, start a two-week free trial to one of our three membership levels. You won’t be disappointed!