Sep 29, 2022

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, We begin tonight with a look at the VIX (page 1) followed by a look at which stocks made new lows today (pages 2 – 4). We then provide a rundown of the latest revision to GDP (page 5) with a closer look at GDI (pages 6 -7). We finish with a look at consumer sentiment (page 8) and investor sentiment (page 9).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Sep 29, 2022

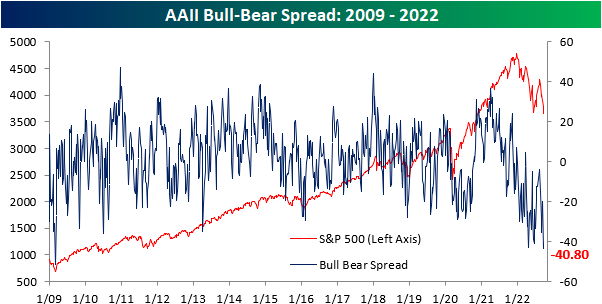

Although the S&P 500 hit 52-week lows for the first time since June this week, bulls actually stepped back up to the plate (in a very small way). Bullish sentiment, according to the AAII sentiment survey, rose back up to 20% after a low of 17.7% last week. Even with that modest increase, bullish sentiment remains historically muted at 17.7 percentage points below the historical norm.

Bearish sentiment likewise remains elevated and hardly improved. The latest reading dropped marginally from 60.9% to 60.8% marking the first time on record that there have been back-to-back readings of 60% or more as we noted in an earlier tweet. The only other times bearish sentiment came in above 60% were in March 2009, October 2008, and August and October 1990.

Given the near record high in bearish sentiment coupled with the slight increase in bullish sentiment, the bull-bear spread improved rising from -43.2 to -40.8. Again, in spite of that improvement, the latest reading shows that bears continue to heavily outweigh bulls to a historic degree.

Given both bulls and bears are at extremes, recent moves have borrowed heavily from neutral sentiment. That reading has fallen sharply over the past three weeks and is back below 20% for the lowest reading since April 2020. The 9.5 percentage point decline over the past three weeks has been the largest drop in such a span since May pointing to investors being increasingly polarized.

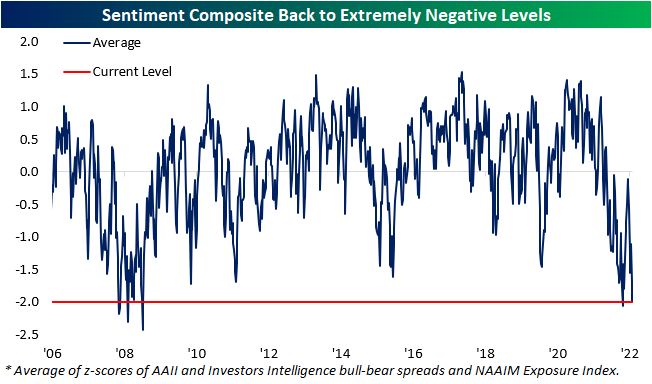

The AAII survey may have moved slightly less bearish this week on net, but other sentiment surveys saw the opposite results. The Investors Intelligence survey saw bulls hit the lowest level since 2016, and the NAAIM exposure index showed the least long exposure to equities since March 2020. Standardizing and then combining each of these surveys shows that the average reading is now two full standard deviations below the historical norm. That is slightly better than the June low with the only other period with as depressed a level of sentiment being the financial crisis years. Click here to learn more about Bespoke’s premium stock market research service.

Sep 29, 2022

Adding ammunition to the hawkish tone out of the Fed, this week’s initial jobless claims number showed yet another decline to already impressively low levels. Not only was last week’s reading revised down by 4K to 213K, but this week’s reading fell back below 200K. Now at 193K, claims are back to where they were in April after having fallen for six of the last seven weeks. With a drop back below 200K, claims have fallen back below the range from the couple of years prior to the pandemic. Outside of lows earlier this year, that would be some of the best levels for claims since 1969.

Before seasonal adjustment, it is an even equally impressive low. For the comparable week of the year, this most recent reading of 156.1K was the lowest since 1969 and was only slightly above the seasonal low from a couple of weeks ago. While it does not steal from how strong claims have been, we would note that the current week of the year does have some seasonal tailwinds with a decline roughly 70% of the time.

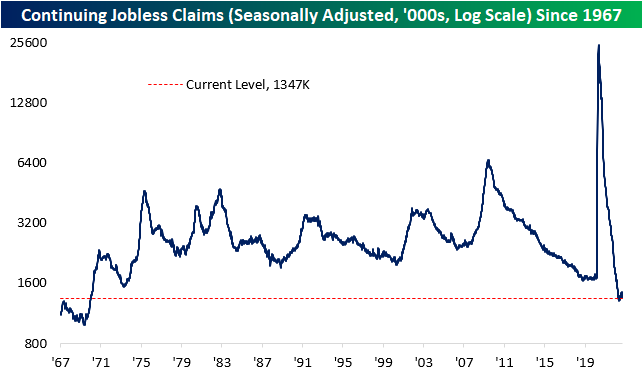

Continuing claims are lagged an additional week to initial claims making the most recent print through the week of September 16th. Claims fell for the sixth consecutive week to reach 1.347 million, the lowest level since the first week of July. Click here to learn more about Bespoke’s premium stock market research service.

Sep 28, 2022

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we start out looking at the historic moves across fixed income markets (page 1) followed by a principal component analysis of eight different assets (page 2). Turning to macro data, we highlight the trade deficit surge (page 3), the latest CFO survey (page 4), and EIA data (page 5). We finish with a rundown of the 7 year note auction (page 6).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!