Jobless Claims Snoozer

Jobless claims continue to be a snoozer. Headed into tomorrow’s nonfarm payrolls report, initial jobless claims were little changed falling 1K down to 217K. Over the past month, claims have been in a relatively tight range of only 12K. That is the tightest one-month range since late June/early July, albeit claims are at slightly healthier levels than back then as well.

On a non-seasonally adjusted basis, claims are at 185.6K, which is the lowest level since 1969 for the comparable week of the year. Claims have been on the move higher as is the norm for the point of the year. In fact, the current week of the year has been one of the most frequent to see week-over-week increases in unadjusted jobless claims with increases 83% of the time since 1967.

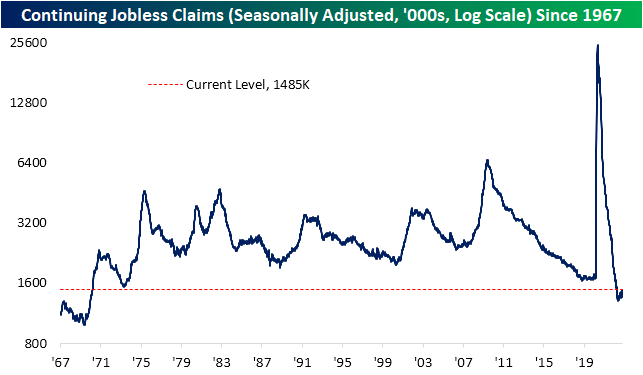

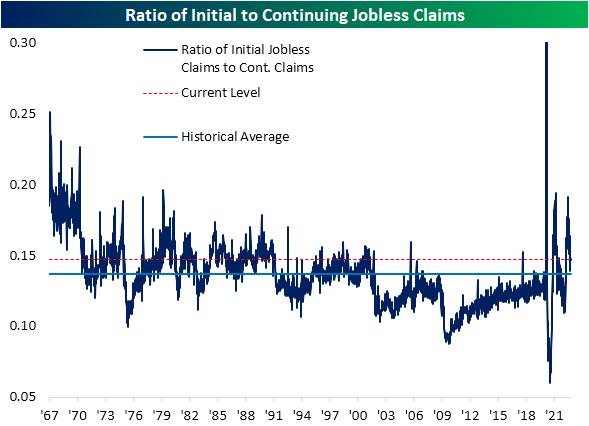

While initial jobless claims have not seen particularly large moves recently, the picture for continuing claims has begun to shift. Although continuing claims are much further below their pre-pandemic range than initial claims, the most recent week saw a move up to 1.485 million which is the highest level since the end of March. As a result, the ratio of initial to continuing claims has moved sharply lower and is closing in on its historical average. That compares to earlier this year when initial claims were running at much weaker levels than continuing claims implying little follow-through on initial claims. Click here to learn more about Bespoke’s premium stock market research service.

Bears Down By 20

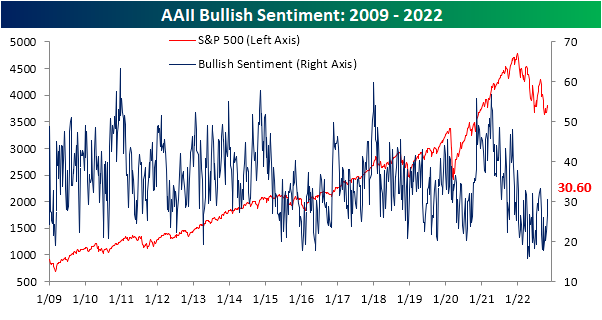

Given the collection period, the latest sentiment data from the weekly American Association of Individual Investors survey would not have fully captured the FOMC meeting yesterday or the market’s reaction to the event. As a result, with the S&P 500 having erased a large portion of late September and early October losses, sentiment took a massive bullish swing. Bullish sentiment gained 4 percentage points for the third weekly increase in a row. Bullish sentiment topped 30% for the first time since the week of August 18th.

Relative to the moves in bearish sentiment, those gains to bulls are outright modest. In the past two weeks, bearish sentiment has seen back to back double digit declines, bringing it from 56.2% all the way down to 32.9%; the lowest level since the end of March. That was the first time that bearish sentiment has seen back to back declines of at least 10 percentage points since 2009, and further back in the history of the survey that has only happened two other times: June 2004 and in the first year of the survey in September 1987.

While back to back double digit declines for bearish sentiment are exceedingly rare, there has been more precedent for bearish sentiment falling at least 20 percentage points in a two week span. In the table below, we show each occurrence that has happened with at least 3 months between the prior occurrence.

As for how the S&P 500 has typically reacted, forward performance has been lackluster.

Given the massive drop in bearishness, the bull bear spread has experienced a massive reversal. At the moment, the spread is only at -2.3. That is the highest reading since the end of March, and the near record streak of consecutive negative readings (31 weeks) appears to be at risk.

Obviously considering only a small share of the losses to bears have gone to bulls, the percentage of respondents reporting neutral sentiment has risen sharply. The reading climbed 8.8 percentage points week over week to 36.5%. That is the highest reading and largest weekly jump since the end of March Click here to learn more about Bespoke’s premium stock market research service.

The Closer – Federal Open Market Confusion: Higher Terminal Rates Ahead – 11/2/22

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we provide a complete rundown of the FOMC meeting including commentary on the FOMC’s confused communications (page 1), the reaction across assets (page 2), as well as a more granular look at the remarkable reaction by stocks (page 3). We then turn over to the latest major earnings reports released after the closing bell (page 4) before closing with a rundown of the latest EIA data (page 5).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!