Chart of the Day – The Latest Vintage of New Highs

Bespoke Stock Scores — 10/22/19

Dividend Stock Spotlight: United Parcel Service (UPS)

About a month ago, FedEx (FDX) reported disappointing EPS and sales and also lowered guidance. As a result, the stock experienced its second-worst earnings reaction day performance of any earnings day since 2000, falling 12.92%. This morning, another shipping giant, United Parcel Service (UPS), reported their third-quarter results.

In the table below, we show UPS’s earnings results for quarters that FedEx (FDX) has reported a similarly weak quarter to the September report (missed EPS and sales estimates and lowered guidance). Weak FDX quarters have not necessarily preempted UPS would also disappoint. In other words, one company’s weakness is not necessarily indicative of broader slowing in the logistics space. In fact, in 2005 in the face of FDX’s weak quarter, UPS reported the exact opposite with a triple play, and there was only one occurrence where UPS reported the same type of misses and lowered guidance relative to expectations as FDX. Otherwise, there was only one other quarter when UPS missed EPS forecasts and three others (including the most recent) when it missed sales. While UPS didn’t’ necessarily report the same bad results relative to expectations, though, in terms of stock price performance, it has also generally seen weak performance on these days with one-day declines on all but one of the five prior occurrences.

This morning’s report and subsequent reaction have not been strikingly different. UPS’s earnings were a bit of a mixed bag, though were far from as horrifying as FedEx. UPS exceeded EPS estimates of $2.06 by 1 cent as operating profit growth year-over-year topped 20%. Meanwhile, revenues came in $27.4 million below estimates but were up 5% from the prior year. Despite this top-line miss, the company also reported overall domestic volumes were up 9% year-over-year thanks in large part to much higher next-day shipping volumes (up 24% YoY) which is likely a result of online retail. The company also reported that the COO, who was anticipated to be a top candidate for the soon to be available CEO seat, is stepping down. With the good and bad, the stock gapped down 2.26% at the open and remains near those levels as of this writing.

As shown in the snapshot of our Earnings Explorer below, UPS historically has not been the strongest of stocks in reaction to earnings. Of all 72 reports since 2001, the company has beaten EPS and sales only a little better than half of the time, 58% and 53%, respectively. In response, the stock has averaged a gap down of 22 bps and a full day gain of just 7 bps. Over the past several quarters there has not been any consistent pattern to how the stock has traded in response to earnings with today’s negative reaction being the worst since April.

With today’s negative price reaction to earnings, UPS’s chart is still in an uptrend over the past six months and also has a good timing score in our Trend Analyzer tool on account of it teetering into oversold territory. From a dividend standpoint, UPS is also one of the more attractive stocks among the S&P 500 industrials with the fourth-highest dividend yield, behind Eaton (ETN), 3M (MMM), and Nielsen (NLSN). At 3.37%, the stock yields nearly double the sector average and is also well above the ~1.9% yield of the S&P 500. The company has grown its dividend every year over the past decade and given a payout ratio of 63.5%, it looks to be capable of continuing to do so. Provided the stock holds above support between $110 and $115, the stock is an interesting option for income-oriented investors. Start a two-week free trial to Bespoke Institutional to access our Earnings Explorer, Trend Analyzer, and much more.

Global Equities: Everybody Wins!

The image below is a snapshot of 35 different country ETFs from our Trend Analyzer tool in the interactive section of our website. For each ETF, we start off by showing its YTD performance along with where each one closed the prior trading day with respect to its 50-day moving average. From there, we also show each ETF’s Trend rating (up, down, or sideways), along with a ‘Timing’ score that takes into account each ETF’s trend and where it’s trading with respect to its trading range to determine whether current levels provide a statistically attractive time to take a long position. Finally, we also show where each ETF is trading with respect to its trading range (red or green circle) and where it was trading one week earlier (end of tail).

Looking at the current snapshot, the majority of country ETFs are not only above their 50-day moving averages, but they are also overbought. In fact, just nine ETFs are not overbought and only one – Turkey (TUR) – is below its 50-DMA. What’s really amazing about the recent performance of the country ETFs, though, is that all 35 ETFs listed below have traded higher over the last week. So it has not only been a good week for US equities, but stocks around the world have also been in rally mode. Leading the way to the upside, Sweden (EWD), Poland (EPOL), Turkey (TUR), and Austria (EWO) are all up over 4%, while Israel (EIS), China (GXC), Vietnam (VNM), and Malaysia (EWM) have lagged with gains of less than 1%.

So why are equities rallying on a global scale? There are a number of factors behind the move, ranging from some improved tone in global data, positive earnings, and the evergreen headline of optimism related to trade. One key thing to keep in mind with regards to the performance of the ETFs below, though, is that the returns are expressed in US dollar terms. Because the dollar has declined over 1% over the last week, it therefore automatically provides a boost to performance figures. The weak dollar hasn’t accounted for all of the strength in the individual country ETFs over the last week, but it has accounted for a large share of the gains. Start a two-week free trial to Bespoke Premium to sample our most actionable investment research and receive access to all of our interactive tools. If you use this checkout link, you’ll receive a 10% discount on an annual membership if you stick with it past your trial period.

Bespoke’s Morning Lineup – 10/22/19

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

Biogen (BIIB) Set to Gap up 40% on Earnings/Drug News

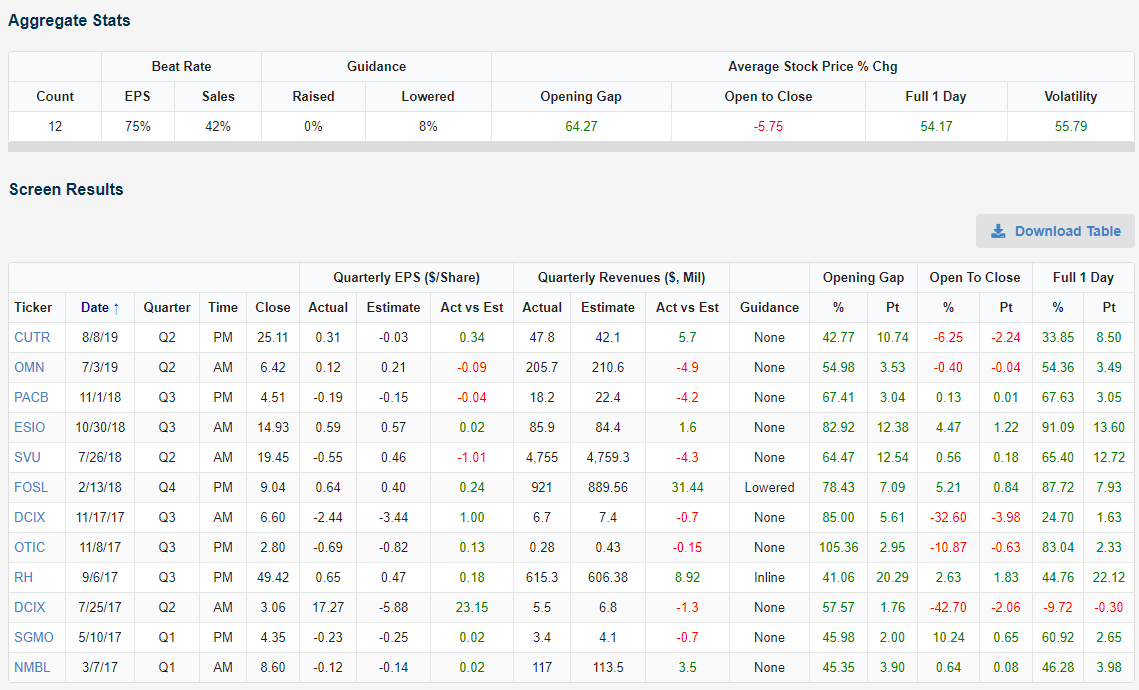

Biogen (BIIB) shares are currently set to gap higher by 41% this morning due to earnings and positive news for its Alzheimer’s drug. A 40%+ gap on earnings is extremely rare, but we can find historical occurrences very easily using our Earnings Explorer tool. Seeing how prior stocks performed following big gaps up or down on earnings is one of the many useful ways to use our Earnings Explorer. Below are the results from a quick screen we ran that found all stocks reporting earnings since the start of 2017 that opened higher by at least 40% on the day. As shown, there have only been 12 occurrences, and the average gap up at the open for these 12 names was +65.27%.

After their initial massive gap higher, these 12 stocks averaged a decline of 5.75% from the open to the close of trading, so it appears that traders look to book some profits. However, the average is actually skewed by DCIX, which shows up twice on the list with back-to-back gaps up of 50%+ back in 2017. In July 2017, DCIX opened higher by 57% only to trade down 42% from the open to the close for a full-day decline of 9%. In November 2017, DCIX opened up 85% only to fall 32% from the open to the close. On its November 2017 report, at least DCIX still managed to close higher by 25% for the full day.

All in all, 7 of the 12 stocks that have gapped up 40%+ on earnings since 2017 have continued higher from the open to the close. One thing for sure is that BIIB would be the highest priced stock to gap up 40%+ on earnings since at least 2001 when our database begins. No stock above $200/share has gapped up even 30%+ following an earnings report. The only $100+ stocks to gap up 30%+ since 2001 are Netflix (NFLX) and First Solar (FSLR). Netflix opened higher by 39% following its January 2013 report (when it had closed at $103/share the prior day) and it gained another 2% from the open to the close that day. FSLR closed at $167/share on 11/7/07 and then gapped up 32% the next morning following earnings. That day FSLR continued higher by 1.5% from the open to the close to finish the day up 34.3%. Biogen (BIIB) closed yesterday at $223.51 and is currently trading between $305-$320 in the pre-market. Start using our Earnings Explorer tool now with a Bespoke Institutional membership. Click here to join and get your first 14 days free.

The Closer – EMFX, Dollar Positioning, Building Reversals, Banks, Canada Votes – 10/21/19

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, we go over multiple FX currencies including KRW, the Taiwanese dollar, Chinese yuan, and Chilean peso. We also look at how speculators are positioned on the US dollar and reasons to expect further dollar weakness. We then review banks’ breakout before turning to a primer on the Canadian election.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

B.I.G. Tips – Death by Amazon – 10/21/19

Our “Death By Amazon” index was created many years ago to provide investors with a list of retailers we view as vulnerable to competition from e-commerce. In 2016, we also created our “Amazon Survivors” index which is made up of companies that look more capable of dealing with the threat from online shopping. To see how the two indices have been performing lately and view the full list of stocks that make up the indices, please read our newest report on the subject available to Bespoke Premium and Bespoke Institutional members.

To unlock our “Death By Amazon” and “Amazon Survivors” indices, login or start a two-week free trial to either Bespoke Premium or Bespoke Institutional.

Can Cadence (CDNS) Keep Its Streak?

Cadence Design (CDNS), an electronic design supplier and engineering services firm, reports earnings after the close tonight. The company is expected to report EPS of $0.51 and sales of $576.3 million compared to EPS of $0.49 and revenues of $532.5 million one year ago. Over the past couple of years, CDNS has been notable in the stock’s price reaction on earnings days has been consistently positive. Headed into tonight’s report, the stock is on a streak of six consecutive quarters with a positive full-day reaction. That is the longest such streak for CDNS since a six quarter long streak that came to an end in January of 2013. The company has also frequently reported earnings triple plays (EPS and sales beat in addition to raised guidance) in the past couple of years with half of the last ten quarters experiencing a triple play.

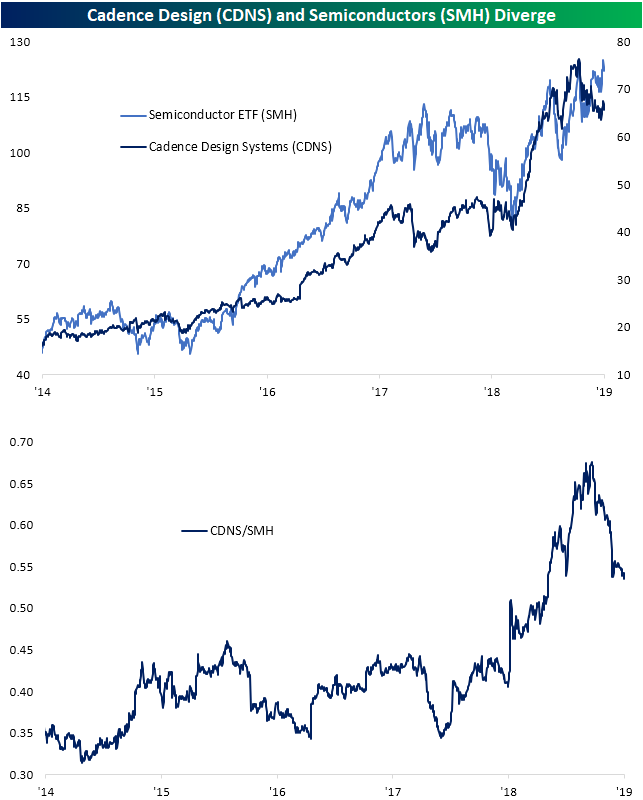

Given the company’s business is tied with that of semiconductors (SMH), while not wholely a semiconductor company itself, CDNS has generally followed the trends of the industry over the past few years. But there has been a few divergences in the past year. Whereas the two had been in steady uptrends earlier in the cycle, then trending sideways together for most of 2018, the Q4 2018 sell-off hit SMH much harder. Since the sell-off, both have rocketed higher in 2019; CDNS even more so than SMH. More recently though, since shortly after CDNS’s last earnings report in July, it has underperformed as shown in the relative strength chart in the second chart below. As CDNS sits in a downtrend, SMH has managed to reach new highs. While the two have not necessarily perfectly tracked each other, the move higher in the semis would have suggested CDNS to move higher.

Headed into this quarter’s earnings, the chart of CDNS has actually begun to reverse this downtrend. After finding support around prior lows at ~$63, the stock broke out of its downtrend but failed to hold above its 50-DMA. If the past six quarters’ trend of positive reactions to earnings continues—in addition to the broader support of related semiconductor stocks—it could be the catalyst needed for the stock to continue to break its downtrend. Start a two-week free trial to Bespoke Institutional to access our Earnings Explorer and much more.

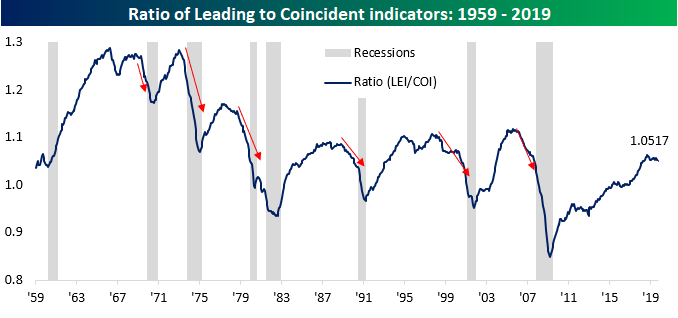

Leading Indicators Decline

We didn’t mention it Friday, but among the multitude of weaker than expected economic indicators last week, the index of Leading Economic Indicators for September was one of them. While the consensus forecast was for the index to remain unchanged from August’s level, it actually declined 0.1%. At times in the past, we have highlighted how sharp downturns in the ratio between Leading and Coincident indicators have often preceded recessions.

In the current cycle, it has now been twelve months since the ratio peaked last September, and while that raises the risk of a recession, we would note that the current downturn in this ratio has been much more gradual than the steep downturns that we saw leading up to prior recessions. Additionally, in both the 1960s and 1990s, we saw instances where the ratio saw much steeper declines without a recession.

The recent downturn in the ratio between Leading and Coincident Indicators isn’t even the first time during this cycle that we have seen the ratio lose momentum and show similar declines. From mid-2011 through late 2013, the ratio went 27 months without hitting a new cycle high, and then again from the second half of 2015 through the end of 2016, there was an 18-month stretch without a new high. In the current period, it has only been 12 months without a new high.

While the current lull in the Leading vs Coincident Indicator ratio hasn’t been long yet, it is still declining. Therefore, it’s nowhere near close to snapping the streak of months without a high. Just looking at the last two periods, for example, from the time the ratio bottomed, it took nine months in 2013 and 11 months in 2016 before the ratio fully rebounded and hit a new high for the cycle. In other words, if the ratio doesn’t start rebounding soon, this period will go down as the longest period of economic slack/consolidation of the expansion. Join Bespoke Premium now to get Bespoke’s most actionable stock market research. Click here to get your first 14 days free.