Chart of the Day: Long Standing Dividend Aristocrats

Get Ready for a Reversal of This Trend

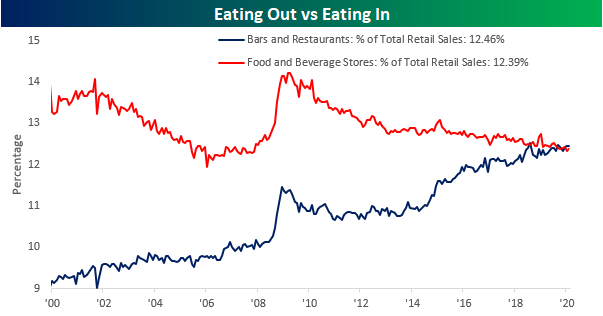

One of the trends we have been highlighting in the monthly retail sales report over the years has been the growing trend of eating out versus eating in. For years we have seen the Bars and Restaurants category of retail sales consistently gaining share at the expense of the Food and Beverage Stores category. Just last month, Bars and Restaurants saw their share of total sales rise to 12.46%, which was just below the record high of 12.47% from October 2018. That total share of sales was also 0.07% greater than the share of Food and Beverage Stores (12.39%) which is also right near record highs.

The run was fun while it lasted. With restaurants all over the country being forced to shut due to fears of the Covid-19 virus, even if American consumers wanted to go out to eat, the only way they can is by ordering takeout. With everybody stuck at home, more Americans will undoubtedly be eating at home in the coming months, and that is going to cause the share of total sales for Bars and Restaurants to come crashing down. The only question is whether other sectors besides Food & Beverage Stores will pick up the slack or if the pie will only get smaller as consumers reign in spending.

The trend of dining out is likely to take a hit in the coming months, but one trend that will only accelerate is ‘clicks’ over ‘bricks’. After overtaking the category of General Merchandise in September 2018, Nonstore retailers have been picking up share at a steady pace ever since. Through February, the current spread in share of 1.3 percentage points is not far from the record seen last September. Again, though, with physical stores all over the country simply closing for an indefinite period in recent days, online is going to become the only option for consumers whether they can leave their homes or not. Start a two-week free trial to Bespoke Institutional to access our interactive economic indicators monitor and much more.

Homebuilders Not Worried Yet

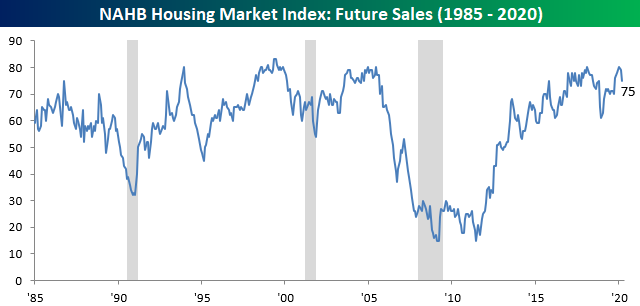

This morning the NAHB released results from their monthly survey of homebuilders. The index showed some weakening in sentiment as it fell to 72 in March from 74 in February. As with many other recent indicators released, that is a fairly modest decline given the current environment and likely would not have captured the full extent of equity market declines and shutdowns to enforce social distancing. Granted, those effects are also not entirely absent either seeing as the NAHB noted half of the responses to the survey came after March 4th.

The headline index fell on lower readings pretty much across the board. Each of the sub-indices with the exception of the Midwest fell in March. Additionally, perhaps the biggest negative shift this month was for future outlook with that index falling 4 points. By comparison, the index for present sales only fell by 2 points. In other words, homebuilders seem to have experienced some slowdown in activity and are anticipating for it to get worse.

Again the index for the Midwest in March was a bit of an outlier. It was the only region to rise in March, but that is after it was a bit weaker than other regions recently. In fact, the rise to 67 also still leaves the index for the Midwest 6 points off of the December high of 73. Overall, as with the headline index, across different regions, sentiment has shifted lower although this is likely just the tip of the iceberg.

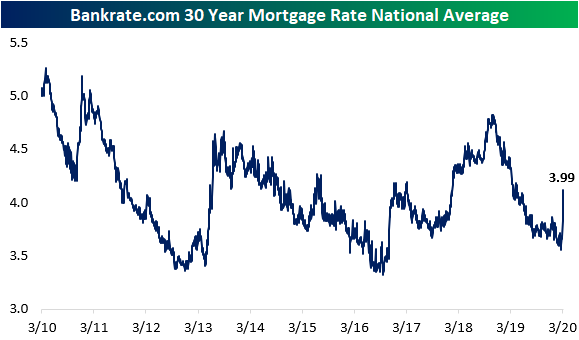

One factor at play that that may be balancing itself out is mortgage rates. The national average for a 30 year fixed rate mortgage was sitting at the low end of the past few years’ range earlier this month. In the past week, though, mortgage rates have moved sharply higher and are now at similar levels to where they were last year. In other words, while low rates may have temporarily bolstered homebuilder confidence earlier this month, given the move in the past week, those effects have likely eased. Turning to next month’s survey, there is likely to be a large downward shift lower in homebuilder sentiment, especially if rates continue to drift higher. Start a two-week free trial to Bespoke Institutional to access our interactive economic indicators monitor and much more.

GDP Forecasts Relative to History

Yesterday, Goldman Sachs’ lead economist cut the bank’s GDP forecasts for the first half down to 0.0% in Q1 and a decline of 5.0% for the second quarter. Based on how things are moving and in the direction they are going, 5% may sound like an optimistic scenario. While all sorts of numbers have been thrown around regarding just about everything lately, we wanted to help put in perspective just how severe a quarterly decline in GDP of 5% really is.

The chart below shows US quarterly GDP going back to 1950. First of all, negative quarters for GDP have been uncommon for the US economy over time. In the 291 quarters since 1950, the US economy has only contracted in 41 (14%) of those quarters. 5% declines, however, are incredibly rare. SInce 1950, there have only been six prior quarters where GDP declined by 5% or more with the most recent being back in December 2008.

Obviously, the circumstances surrounding each contraction in GDP is different, but prior quarters where there was such a large shock to the system were typically not ‘one and done’ events. In fact, all six of the prior quarterly contractions of 5% or more were either immediately preceded or followed by another quarter of negative growth averaging a decline of over 2%. Start a two-week free trial to Bespoke Institutional to access our full suite of research and interactive tools.

B.I.G. Tips – Ten Year Price Charts

Bespoke’s Morning Lineup – 3/17/20 – Market Could Use a Little Luck

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

When the only thing you have left to fall back on is a little luck, things are bad out there. Futures were limit up at one point overnight, but those gains have faded as we near the close. Conditions in the credit markets aren’t faring as well, though. Despite all of the central bank actions over the last several days, credit spreads continue to widen.

Retail Sales were just released and came in much weaker than expected (-0.5% vs +0.2%), so despite all that shopping at Costco and stores like that as consumers stocked up on supplies, the overall total was weak.

Read today’s Bespoke Morning Lineup for a discussion of overnight moves in the credit markets, the latest stimulus plans coming out of Washington, and the trading in Asia and Europe.

Normally, when the equity market reaches extreme overbought or oversold levels it doesn’t stay that way for long. That hasn’t been the case recently, though, as the S&P 500 has been consistently at extreme oversold levels for a number of days now. There’s only so much time that the market or investors can stand these types of oversold readings.

The Closer – Washington Wakes Up – 3/16/20

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, we review the historic session as DC makes plans to provide stimulus to the American public. We then show what the drop in GDP could look like as a result of Covid-19. Next, we the massive move in the S&P 500 and dollar as well as the normalization in Treasury markets. We finish with a look at just how bad breadth has been in the past couple of weeks.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

Daily Sector Snapshot — 3/16/20

B.I.G. Tips – Historic Volatility

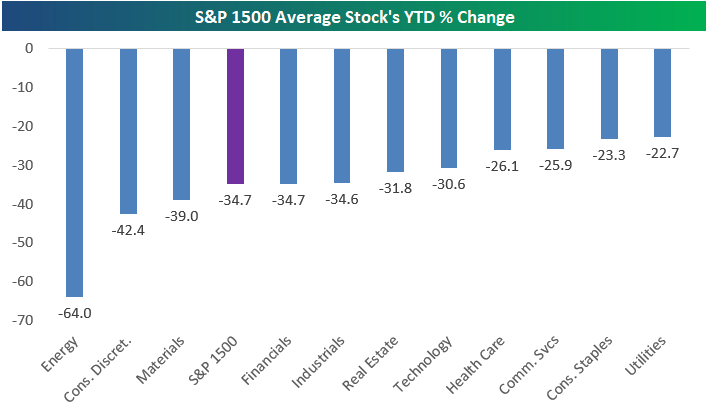

S&P 1500 Sector Declines

The average S&P 1500 stock is now down more than 25% month-to-date, 35% year-to-date, and 44.5% from its 52-week high. Below is a look at the carnage across S&P 1500 sectors. Start a two-week free trial to Bespoke Institutional to access our full suite of research and interactive tools.