10% of Population Filing Jobless Claims

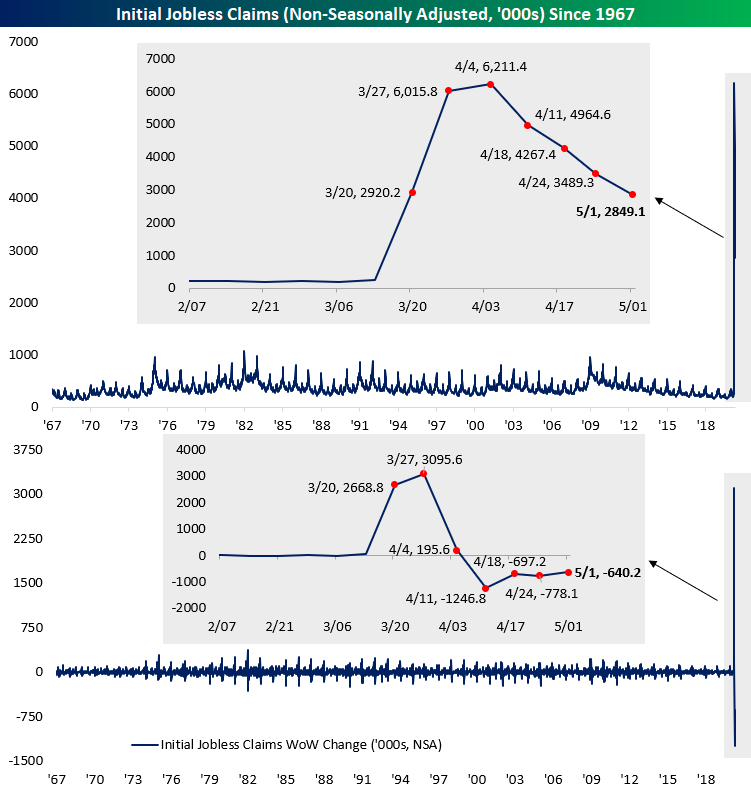

Initial jobless claims fell for a fifth consecutive week down from 3.839 million last week to 3.169 million this week. While that is still extremely high by historical standards, that is the lowest print since jobless claims starting printing more than a million in late March. In other words, a massive number of people are continuing to file for unemployment insurance, but the pace of increase has slowed down with the peak in the rearview for the time being.

On a non-seasonally adjusted basis, this week was only the fourth consecutive decline with claims now down to 2.849 million. As with the seasonally adjusted number, this week’s print was the smallest of the past several weeks since claims first began to print in the millions but is still very high compared to the rest of history.

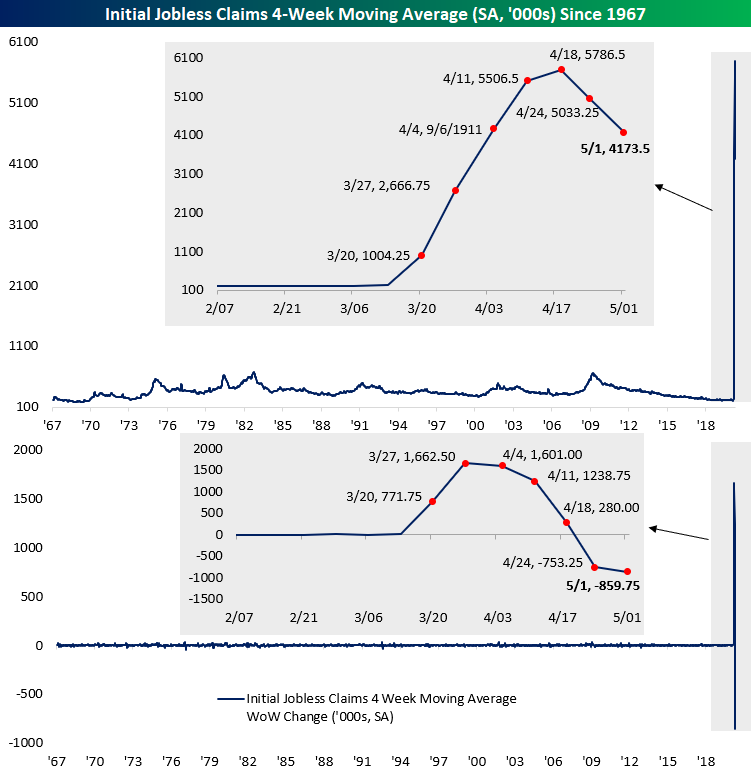

The four-week moving average has also seemed to have peaked for the time being as it fell for a second straight week. The moving average is now down to 4.174 million compared to over 5 million last week. While it could be expected given the massive volatility of the indicator over the past couple of months, that 859.75K decline from last week is the largest single week decline on record (second chart below).

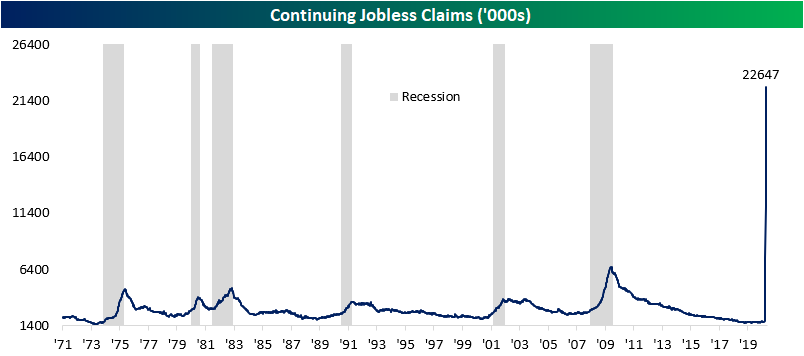

Since the March 20th print (the first one in the millions) to today, a total of 33.483 million initial jobless claims have been filed. That is more than 10% of the US population and over 20% of the labor force!. As such, continuing jobless claims (lagged by a week) came in at another record of 22.647 million this week. Start a two-week free trial to Bespoke Institutional to access our interactive economic indicators monitor and much more.

Chart of the Day: Investor Sentiment Slammed

Bespoke’s Morning Lineup – 5/7/20 – Let’s Try This Again

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

Yesterday was a positive open for the US equity market, but all of those gains melted throughout the trading day and the day was capped with a sharp drop into the close. Today, futures are once again indicating a higher open. In fact, just before the release of weekly claims, futures were right at their highs of the session. After a higher than expected print of 3.169 million relative to expectations of 3.0 million, though, we’ve given up some of those gains, but we’re still firmly in positive territory. Looking on the bright side, at least claims have dropped for five straight weeks now. We’ll see what happens at 4 PM.

Be sure to check out today’s Morning Lineup for a rundown of the latest stock-specific news of note, Chinese export data, and the latest stats and trends on the COVID outbreak.

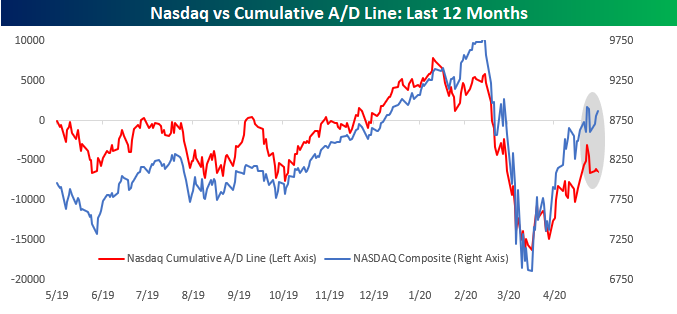

In yesterday’s email, we took a look at breadth in the S&P 500, but we all know that the Nasdaq has been the real star of the show. This morning, we wanted to provide a quick look at breadth in the Nasdaq. All we’ve heard recently is that the ‘big five’ of Microsoft, Apple, Amazon, Alphabet, and Facebook have been driving the market, especially the Nasdaq. The reality isn’t quite the case. While it’s true that back in February, the Nasdaq’s cumulative A/D line made a lower high just as the Nasdaq peaked, ever since then, breadth has been tracking price pretty closely. Through the end of April, for example, both price and breadth were at post 3/23 highs.

While breadth has tracked price pretty closely since the March lows, in recent days there has been a modest divergence between the two. As shown in the shaded region, while the Nasdaq’s price level remains right near its recent highs, the cumulative A/D line has been weaker. At this point, the divergence is small enough that it could be erased in a matter of days, but if this May pattern persists, then it will be a more definite sign of waning participation in the bounce. Today should be a good test for the Nasdaq as we’ve seen a number of smaller stocks in the index trading higher in reaction to earnings.

Daily Sector Snapshot — 5/6/20

Chart of the Day: Google Search Trends Round 2

Bespoke’s Consumer Pulse Report — May 2020

Bespoke’s Consumer Pulse Report is an analysis of a huge consumer survey that we run each month. Our goal with this survey is to track trends across the economic and financial landscape in the US. Using the results from our proprietary monthly survey, we dissect and analyze all of the data and publish the Consumer Pulse Report, which we sell access to on a subscription basis. Sign up for a 30-day free trial to our Bespoke Consumer Pulse subscription service. With a trial, you’ll get coverage of consumer electronics, social media, streaming media, retail, autos, and much more. The report also has numerous proprietary US economic data points that are extremely timely and useful for investors.

We’ve just released our most recent monthly report to Pulse subscribers, and it’s definitely worth the read if you’re curious about the health of the consumer in the current market environment. Start a 30-day free trial for a full breakdown of all of our proprietary Pulse economic indicators.

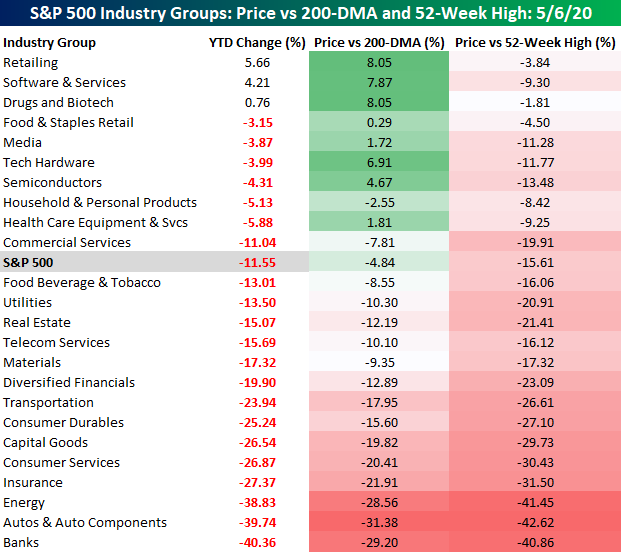

No Love for the Banks

While the S&P 500 has started to run out of momentum in recent days, there are still a handful of S&P 500 industry groups that are hanging onto gains on a YTD basis. Leading the way higher, the Retailing Industry Group is up over 5% YTD. That performance is a bit misleading, though, as the majority of retailers are under enormous pressure. Here’s a bananas stat for you. Of the 25 stocks in the Retailing industry group, Amazon.com (AMZN) accounts for 59.4% of the group’s entire market cap. While AMZN is up 25% YTD, the average performance of the stocks in the group on an unweighted basis is a decline of over 18% and the only other stock in the group that is up YTD is Home Depot (+4%). Given the divergent paths of AMZN and everyone else, it has seen its share of total market cap increase by ten percentage points just since the start of the year. The increasing dominance of AMZN over the rest of the retail sector can ultimately become problematic for both. The continuation of the shutdown and AMZN’s dominance only make it more likely that pressure on traditional retailers will increase, but as more retailers shut their doors, the empty stores and out of work employees that follow will undoubtedly lead to increased political pressure on AMZN.

In terms of winners on a YTD basis, behind AMZN Retailing, the only two other groups in the black are Software & Services (4.21%) and Drugs and Biotech (0.76%). These three industry groups are also the furthest above their 200-DMA with Tech Hardware and Semis rounding out the top five.

On the downside, there’s no shortage. While just about everyone knows that the Energy sector has been one of the worst-performing groups in the market, you may be surprised to learn that it is not the worst-performing industry group on a YTD basis. In fact, both Autos (-39.74%) and Banks (-40.36%) are both down more than Energy (-38.83%) at this point. While bank balance sheets were a lot healthier heading into this crisis than they were in the last one, investors haven’t been convinced that they will be able to get through the COVID pandemic without taking a major hit. Learn more about Bespoke’s premium insights at our membership options page.

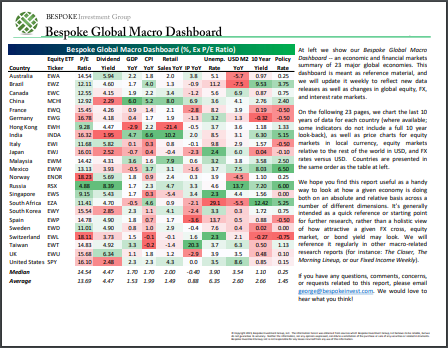

Bespoke’s Global Macro Dashboard — 5/6/20

Bespoke’s Global Macro Dashboard is a high-level summary of 22 major economies from around the world. For each country, we provide charts of local equity market prices, relative performance versus global equities, price to earnings ratios, dividend yields, economic growth, unemployment, retail sales and industrial production growth, inflation, money supply, spot FX performance versus the dollar, policy rate, and ten year local government bond yield interest rates. The report is intended as a tool for both reference and idea generation. It’s clients’ first stop for basic background info on how a given economy is performing, and what issues are driving the narrative for that economy. The dashboard helps you get up to speed on and keep track of the basics for the most important economies around the world, informing starting points for further research and risk management. It’s published weekly every Wednesday at the Bespoke Institutional membership level.

You can access our Global Macro Dashboard by starting a 14-day free trial to Bespoke Institutional now!

Bespoke’s Morning Lineup – 5/6/20 – ADPain

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

Futures are off their earlier highs but still indicating a higher open. The big datapoint of the morning was the April ADP Private Payrolls report which came in at 20.236 million- by far the highest ever reading (by a factor of more than 20). While it’s little to no consolation, the print was actually slightly better than expected. Maybe the most impressive aspect of the release was that consensus estimates (20.550 million) were so close to the actual print.

Be sure to check out today’s Morning Lineup for a rundown of the latest stock-specific news of note, April PMI data, German Factory Orders, and the latest stats and trends on the COVID outbreak

We’re always paying close attention to market breadth for any signs of potential strength or weakness in the underlying market. The chart below shows the S&P 500’s cumulative A/D line and price over the last year. Comparing the two shows that breadth coming off the March lows has tracked price pretty closely. Just about every higher high and higher low in the market has been confirmed by the S&P 500’s cumulative A/D line, so that doesn’t suggest anything untoward occurring underneath the surface.

While overall breadth is positive, there has been an interesting and modestly negative divergence in breadth on big market days versus big down days. Since the 2/19 high for the S&P 500, there have been a total of 42 trading days where the S&P 500 was up or down 1% or more. On the 20 days where the S&P 500 was up over 1%, the median breadth reading was +370. On the 22 days where the S&P 500 was down over 1%, though, the median breadth reading was considerably more one-sided at negative 439. In other words, on days where the market is down big, investors are taking more of a sell everything approach, whereas on days when the market is up big, they are being more discriminating in their buys.