Daily Sector Snapshot — 12/4/20

Bespoke’s Morning Lineup – 12/4/20 – Positive Tone into Jobs Report

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

“I buy when other people are selling.” – J. Paul Getty

It’s safe to assume then that Mr. Getty hasn’t been buying much lately. Futures are higher again this morning putting the S&P 500 on pace for its fourth positive week in the last five, but in order to get there, we’ll have to get through the November jobs report. There have been some concerns about the health of the jobs market lately, but secondary indicators we track have been holding up relatively well.

Be sure to check out today’s Morning Lineup for updates on the latest market news and events, a discussion of the latest OPEC talks, factory orders in Germany, an update on the latest national and international COVID trends, and much more.

We’ve illustrated the positive breadth in the market in a number of different ways lately, but here’s another. For the last few days now, all 24 of the S&P 500’s Industry Groups have been trading above their 200-DMA. Looking back at the last five years, that doesn’t happen all that often. The last time there was such a high reading was at the start of the year on January 2nd. While the year may be on pace to finish right where it started in terms of breadth, it was far from a straight line as this reading went from 100% down to 0% and back to 100%. You can’t get any wider of a range than that!

Bespoke’s Weekly Sector Snapshot — 12/3/20

Bearing Down Into The Holidays

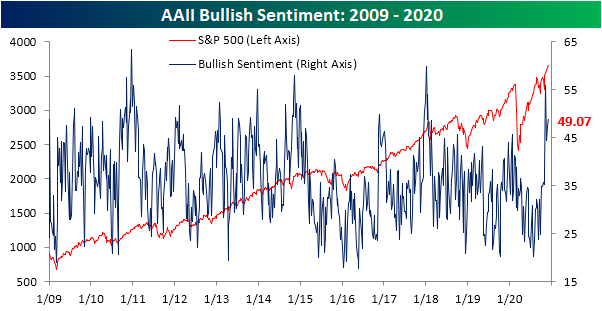

The S&P 500 has pressed to more all-time highs, and as a result, sentiment has turned even more bullish. In this week’s AAII sentiment survey, nearly half of the respondents (49.07%) reported a bullish. That is up for a second week in a row and remains at some of the highest levels of the past few years, though, it is more moderate than the reading from the first week after the election when over 55% reported as bullish.

While bullish sentiment is still off its recent highs, bearish sentiment has continued to press to new lows. 22.66% of respondents reported as bearish this week. That is down from 27.47% last week and is the lowest reading for bearish sentiment since the final couple of weeks of last year and the first week of 2020.

Given this, the bull-bear spread remains widely in favor of bulls, but off of its highs from a few weeks ago. Just like bullish sentiment, it is still at some of the highest levels of the past few years. Outside of the early November high, the bull-bear spread is at the highest level since February 2018.

Neutral sentiment is perhaps the most normal of the sentiment categories. While bullish and bearish sentiment readings are several percentage points away from their historical averages, at 28.25% neutral sentiment is only 3.19 percentage points below its historical average. Click here to view Bespoke’s premium membership options for our best research available.

Equity Newsletter Exuberance

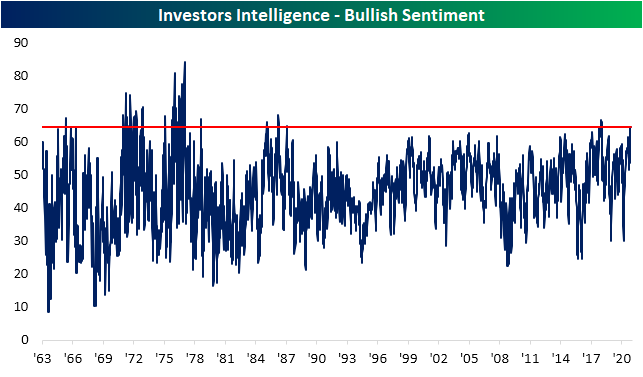

As we discussed in an earlier post, sentiment, as proxied by AAII’s weekly survey, has been overwhelmingly bullish. Other sentiment surveys are echoing the exuberance among investors. The Investors Intelligence survey of equity newsletter writers likewise saw bullish sentiment rise again this week from what were already strong levels. 64.7% of respondents reported as bullish this week. That is in the top 3% of all readings in the history of the survey. The last time this reading on bullish sentiment was this elevated was in January of 2018. Prior to that, you would need to go all the way back to February of 1987 to find a time that a higher share of respondents reported as bullish.

Meanwhile, just 16.7% of the respondents reported as bearish. While not at the same sort of extreme as bullish sentiment (in the bottom 13% of all readings), that is the lowest reading since early September.

In addition to gauging bearish sentiment, the report also measures the percentage of respondents that are “looking for a correction”. This reading ticked slightly higher this week rising from 18.2% up to 18.6%. While slightly higher, that is still in the bottom 20% of all readings across the history of the survey. More recently, though, this was more of an extreme low. Last week’s reading of 18.2% was the lowest reading since December of 2006. Click here to view Bespoke’s premium membership options for our best research available.

Services Slowing

Just like the reading on manufacturing earlier this week, the ISM’s Non-Manufacturing survey showed overall growth in November, albeit at a slower rate. The headline reading for the services index beat expectations (55.9 vs 55.8 expected) but still came in below last month’s level of 56.6. That is a sixth consecutive month of expansionary readings (readings above 50 indicate growth/below 50 indicate contraction) although the reading for November was the lowest of those six months. The same applies to the composite of the manufacturing and services which fell from 56.9 to 56.1.

Looking across each of the individual indices of the report also resembled the manufacturing report. While most components continue to be consistent with further growth, November did see some slowing across a range of indicators.

The improvements in business activity have considerably moderated over the past few months. After a near-record high reading back in July, this index has fallen every month except for in September. At 58, the index is around levels similar to just before the pandemic began earlier this year. A slowdown in orders likely plays a role in this as the index for New Orders similarly sits in the middle of its historical range following a 1.6 point decline to 57.2 in November. While that is still indicative of new orders growth, it would be the slowest growth since August.

Export order growth slowed in November as that index fell to a barely expansionary reading of 50.4. While orders from outside the US were a bit weak, the index for imports rose to 55 which is the strongest level since January of this year (55.1). One important thing to note with these indices, though, is less than half of survey respondents report that they do not use or track imports/exports (only 29% for exports and 37% for imports). In other words, these readings only apply to a smaller sample of responding firms.

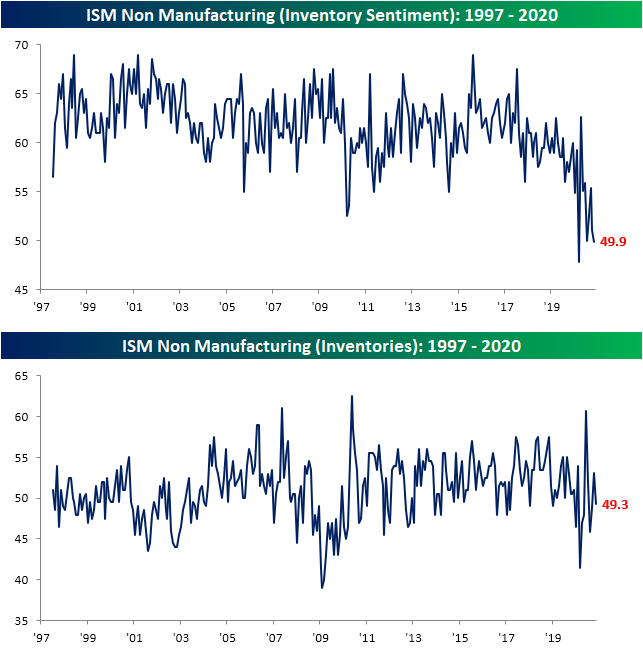

The continued growth in new orders has resulted in smaller inventories. For only the second time in the index’s history (the other instance being March of this year), the index for Inventory Sentiment came in below 50. That indicates a larger share of companies are reporting that inventories are too low rather than too high. As a result, the index for Inventories showed a contractionary reading of 49.3. That is not any sort of extreme reading but again points to declining inventories.

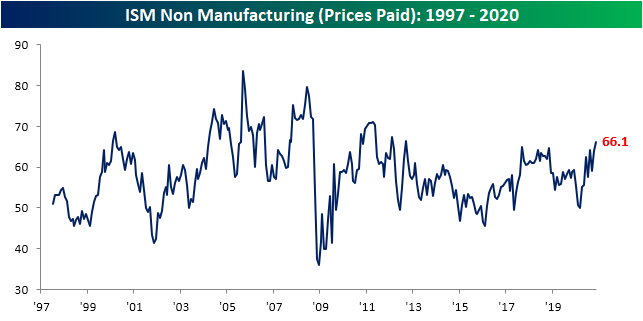

Stronger demand has filtered through to lower inventories which has, in turn, resulted in higher prices. The index for prices paid rose to 66.1 from 63.9 in October. That points to prices growing at their fastest pace since February of 2013.

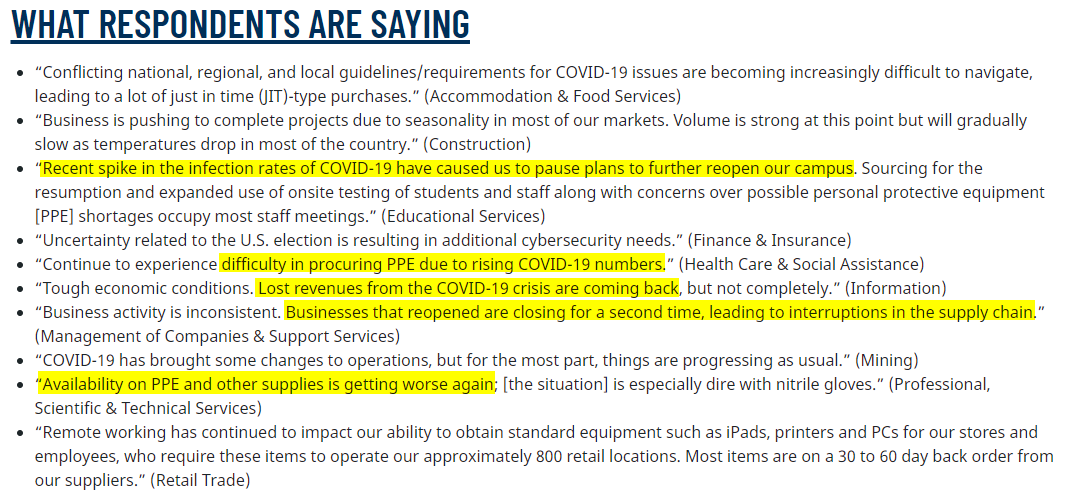

Staying on the topic of prices, with housing flying high, prices for construction contractors and construction supplies like lumber, PVC, and steel have all been on the rise as they remain in short supply. Outside of construction contractors, labor, in general, was cited as in short supply. That is consistent with some commentary concerning employment in Monday’s manufacturing release. But unlike Monday’s report in which the employment component fell to a contractionary reading, the services employment index showed a third straight expansionary reading at 51.5. Additionally, as COVID has made a resurgence in the past few months, PPE and other related products continue to be cited as some of the commodities seeing price increases. For PPE this month saw a 10th month in a row that these products were in short supply with higher prices.

The commentary section reaffirms the COVID ressurgence impact. Quotes from various industries stated how higher infection rates have had negative impacts. Click here to view Bespoke’s premium membership options for our best research available.

Chart of the Day: EM En Fuego

Claims Back to the Lows

After two weeks of upticks, initial jobless claims saw some good news this week ahead of the Nonfarm Payrolls number on Friday. Claims experienced a sizeable decline falling 75K from last week’s upwardly revised reading of 787K. A decline had been expected with forecasts calling for a drop to 775K. Instead, the decline was much larger as claims came in at 712K. That is just 1K above the pandemic low from the first week of November. Although it is still a historically high reading, claims have continued to get closer to moving below the pre-pandemic record high of 695K from October of 1982.

The picture was even better for unadjusted claims. Although the current time of the year has historically marked a seasonal upswing in claims, the 48th week of the year has typically marked a decline week over week. Given the seasonal tailwind for the current week of the year, claims fell to a new low for the pandemic. Unadjusted claims came in at 713.8K, 122.5K below last week’s reading of 836.3. That was the largest weekly decline in the unadjusted number since the last major leg lower in the first week of August when claims fell by nearly 150K.

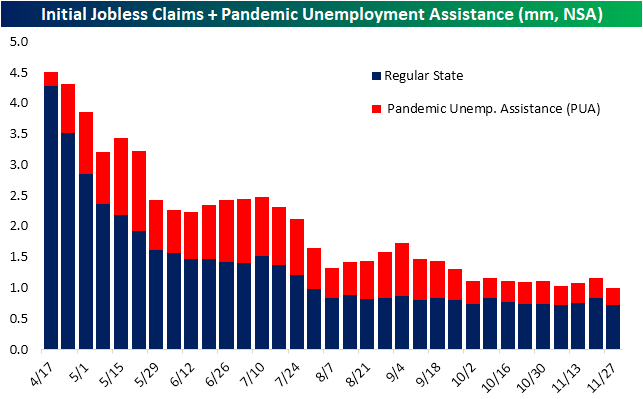

As we note every week, while the decline in regular state initial claims is a welcome sign no matter what, it does not show the entire picture. In the chart below, we show initial claims and claims through the Pandemic Unemployment Assistance program (PUA). This week, total claims between regular state and PUA also reached a new low for the pandemic coming in just above 1 million this week and below the previous low of 1.021 million from the first week of November. That was a result of not only the drop in regular state claims, but PUA claims also falling 30K to a new low.

While lagged an additional week to initial jobless claims, adjusted continuing claims likewise painted a pretty optimistic picture as well. Continuing claims fell 569K this week, down to 5.52 million, exceeding expectations for a decline to 5.8 million. That is the first reading below 6 million since March 20th, and it is also now well below what had been the pre-pandemic record high of 6.635 million from the global financial crisis.

Including the data for all programs of the weekly report adds yet another week of lag, but it does give a more complete picture. For the week of November 13th, total continuing claims fell to 20.2 million from 20.56 million the previous week. That is slightly below the level from the last week of October, which brings total claims to the lowest level since April. Taking a look across the programs, the overall decline was driven by drops in regular state claims and an even larger decline in PUA claims.

Given the length of time that many claims have been in place though, counts for programs that extended insurance once expiration is reached (which varies in length from state to state) like the Extended Benefits program and Pandemic Emergency Unemployment Compensation (PEUC) program have continued to rise. With regards to the Extended Benefits program, claims have now risen for 22 straight weeks through November 13th, albeit the most recent week’s 59.7K rise was the smallest week over week increase since August 21st. Similarly, PEUC claims have continued to rise with the most recent week adding another 79.7K. That leaves the total number of claims between these two programs at over 5.25 million for the first time of the pandemic. That means that despite some light at the end of the tunnel of the COVID front given positive vaccine news, with the pandemic continuing to drag on, nearly a quarter (26%) of all people receiving jobless benefits have been unemployed for an extended period of time. Click here to view Bespoke’s premium membership options for our best research available.

Bespoke’s Morning Lineup – 12/3/20 – Less Terrible Claims

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

“Confidence is not ‘I will profit on this trade.’ Confidence is ‘I will be fine if I don’t profit from this trade.’” – Yvan Byeajee

It’s a busy day for economic data, and it’s starting off on the right foot with both initial and continuing jobless claims coming in better than expected, albeit at still terrible levels. As bad as the numbers are, though, it’s encouraging that claims are moving in the right direction. With claims behind us, the next report of focus is the ISM Services report at 10 AM Eastern. Expectations for this report are also low as activity levels have started to decline in recent weeks as case counts rise.

Be sure to check out today’s Morning Lineup for updates on the latest market news and events, Markit PMI data for the services sector, an update on the latest national and international COVID trends, and much more.

The latest COVID wave has clearly been the most severe in terms of the number of confirmed cases, geographic reach, hospitalizations, and soon to be deaths. The chart below compares the 7-day average number of US confirmed COVID cases (red line) versus the relative strength of our basket of “Stocks for the COVID Economy” that we first published in early March versus the S&P 500 (blue line).

In the early stages of this wave, right before and up to the announcement of the vaccine from Pfizer (PFE) on 11/9, COVID stocks underperformed the S&P 500 rather sharply, but since 11/9, COVID stocks have once again started to outperform the S&P 500. They still remain well off their highs on a relative basis, but the initial reaction to vaccine news appears to have been overdone.