Taking Flight

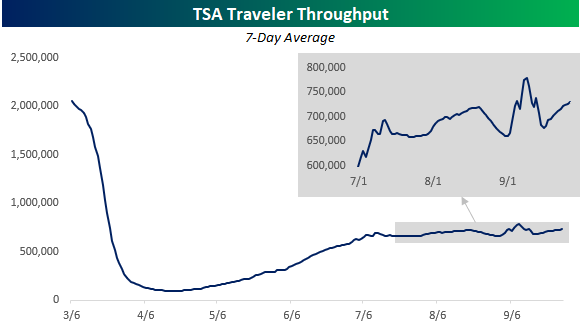

After some volatility in the pace of air traffic where passenger throughput surged early in the month and then quickly came back down to earth in the middle of the month, the number of Americans traveling through US airport security checkpoints has been back on the rise in recent days as the 7-day average through Sunday stood at 730,491, which is less than 50K from the peak level in early September.

While air-traffic trends are improving, relative to last year, total traffic is still down by more than two-thirds (-68.43%). In the chart below, we show the y/y change in TSA passenger throughput (blue line, left axis) to the performance of the Airline ETF (JETS). While the two haven’t tracked each other step for step, there has certainly been a link between the two. While the surge in JETS in late May/early June got ahead of itself and subsequently reversed much of those gains, as y/y traffic trends stabilized in the down 60%-70% y/y range, JETS has also stabilized in the high teens. In order for JETS to get back up to its highs from June, traffic trends will need to start seeing a material acceleration. Click here to view Bespoke’s premium membership options for our best research available.

Bespoke’s Morning Lineup – 9/28/20 – Stimulated Markets

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

“Do more of what works and less of what doesn’t.” – Steve Clark

Will we or won’t we? Investor hopes over a potential new round of stimulus/relief out of Washington have been on the rise this morning after House Speaker Pelosi has indicated that she still thinks a deal with the White House is possible and that both she and Treasury Secretary Mnuchin have agreed to restart informal talks. With Pelosi and Democrats still at $2.3 trillion and the White House and Republicans refusing to go above $1.5 trillion, there’s still a wide gap, but at least they’re talking.

Be sure to check out today’s Morning Lineup for a rundown of the latest stock-specific news of note, market performance in the US and Europe, trends related to the COVID-19 outbreak, and much more.

In last week’s trading, the Nasdaq 100 was the only one of the major US index ETFs to finish the week in the green, but a number of other indices came close with the S&P 100, Russell 1000, and S&P 500 all finishing down less than 1%. With today’s rally at the open, all of these indices will erase last week’s losses right at the open and could even make a run at reclaiming their 50-day moving averages. Mid and small caps, on the other hand, will all need a bit of an added boost to erase last week’s losses, though. What is encouraging about the setup heading into the week, is that the timing scores on all of the ETFs shown currently rank as ‘Good’.

Bespoke Brunch Reads: 9/27/20

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, join Bespoke Premium with a 30-day free trial!

COVID

J&J offers PhI/IIa data showing its single-dose vaccine can stir up sufficient immune response by Amber Tong (Endpoints News)

The outlook for vaccine coverage got a shot in the arm this week as Johnson & Johnson’s early stage data revealed that a single dose gave 98% of participants neutralizing antibodies 29 days after administering just one dose of vaccine. [Link; soft paywall]

How Italy Snatched Health From the Jaws of Death by Elisabeth Braw (Foreign Policy)

After a horrifying first wave, Italians have avoided seeing a resurgence in COVID infections, unlike many of their European neighbors. [Link]

SARS-CoV-2 Transmission Dynamics Should Inform Policy by Muge Cevik, Julia Marcus, Caroline Buckee, and Tara Smith (SSRN)

A detailed review of possible mitigation strategies based on the results of contract-tracing studies. Lower income and high-occupant households are key to the strategy. [Link]

A Notorious COVID Troll Actually Works for Dr. Fauci’s Agency by Lachlan Markay (Daily Beast)

One of the National Institute of Allergy and Infectious Diseases’ PR team has been waging an online disinformation campaign designed to undermine NIAID communications related to COVID. [Link]

“Security”

Ring’s latest security camera is a drone that flies around inside your house by Dan Seifert (The Verge)

Home surveillance company Ring is rolling out an aerial drone designed to be used inside the home, allowing users to remotely activate and patrol when they’re away. [Link]

Texas Deployed SWAT, Bomb Robot, Small Army of Cops To Arrest A Woman And Her Dog by Seth Harp (The Intercept)

Police shut down an entire bridge because they thought a woman’s car decorations meant she was carrying a bomb. [Link]

Schools

Temperature Isn’t a Good Litmus Test for Coronavirus, Doctors Say by Sumathi Reddy (WSJ)

Schools and a variety of other institutions have been using temperature as a proxy for COVID infection, but the loose proxy for infections might be much less useful than widely hoped. [Link; paywall]

New York’s Online Class Sizes Could Reach Nearly 70 Students by Lee Hawkins (WSJ)

With NYC’s in-person reopening of classrooms pushed back, online learning programs may be overwhelmed by students who had planned for in-person learning. [Link; paywall]

Forgone Growth

Citi Pledges to Become Antiracist, Review Internal Policies by Jennifer Surane (Bloomberg)

A new Citigroup report estimates that economic discrimination against Black Americans has cost the US economy $16trn over the last 20 years via lost wages, less education, and less access to loans for business or homeownership. [Link; soft paywall]

Americans Want Homes, but There Have Rarely Been Fewer for Sale by Nicole Friedman (WSJ)

Thanks to both longer-term structural patterns including demographics and the shorter-term drive of lower interest rates and the COVID pandemic, there aren’t many houses available to buy these days. [Link; paywall]

Conservation

Botswana says toxins in water killed hundreds of elephants by Brian Benza (Reuters)

Bacterial blooms in drinking water that produce toxins that are toxic to animals are responsible for the deaths of hundreds of elephants, a devastating side-effect of climate change for an already stressed population. [Link]

Airbus has revealed three zero-emission plane designs that could become reality in just 15 years — take a look at the hydrogen-powered aircraft of the future by David Slotnick (Business Insider)

Hydrogen powered planes are being touted by Airbus as a potential climate solution, with three concept models in the works and potentially ready within 15 years. [Link]

Sustainability Timeline: Walmart’s Journey to a Better Future (Walmart)

This week Wal-Mart committed to zero emissions by 2040 and reserving 50 million acres of land and 1 million square miles of ocean by 2030. [Link]

Read Bespoke’s most actionable market research by joining Bespoke Premium today! Get started here.

Have a great weekend!

Daily Sector Snapshot — 9/25/20

The Bespoke Report — Equity Market Pros and Cons: Q4 2020

This week’s Bespoke Report is an updated version of our “Pros and Cons” edition as we get set for the fourth quarter of 2020.

With this report, you’re able to get a complete picture of the bull and bear case for US stocks right now. It’s heavy on graphics and light on text, but we let the charts and tables do the talking!

On page two of the report, you’ll see a full list of the pros and cons that we lay out. Each bullet point is not meant to be weighted equally, but the fact that there are more cons than pros indicates that the market is entering Q4 facing plenty of headwinds instead of having the wind at its back.

To read this report and access everything else Bespoke’s research platform has to offer, start a two-week free trial to Bespoke Premium. Enter “THINKBIG” at checkout to receive a 10% discount once the trial ends. You won’t be disappointed!

“Low Energy” Energy

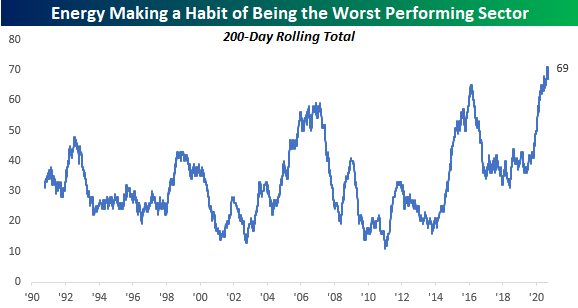

US stocks are looking to close out the week on a positive note with the S&P 500 up over 1%. One sector that hasn’t been participating in the rally, however, is Energy. While it just moved back into positive territory for the day, the sector remains at the back of the pack in terms of sector performance. If these levels hold for the remainder of the trading day, it will be the 69th time in the last 200 trading days that Energy has been the worst-performing sector. That works out to more than once every three trading days. Talk about a sector that’s in liquidation mode!

The chart below shows the rolling 200-day total number of days that Energy has been the worst-performing sector in the S&P 500. While the current level of 69 is extremely high, earlier this month the rolling 200-day total was even higher at 71. Over this same period of time, no other sector has even seen close to as many days of ranking at the bottom as Energy. The next closest is Utilities as it has been at the bottom of the pack in terms of performance on 36 of the last 200 trading days. It hasn’t just been the last 200 trading days that have been rough for the Energy sector. Over the last five years, the sector has been the worst-performing sector on just over 23% of all trading days. Is this what it felt like for the horse and buggy companies in the early 1900s or the ice-harvesting companies after the invention of electric refrigeration? Click here to view Bespoke’s premium membership options for our best research available.

Bespoke’s Morning Lineup – 9/25/20 – Tug of War Continues

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

“Short term volatility is greatest at turning points and diminishes as a trend becomes established.” – George Soros

It’s been a relatively volatile night in the markets as futures vacillate between modest and steeper losses. Currently, they are closer to the side of modest weakness, but that’s subject to change depending on the market’s latest whims. European markets are seeing even sharper declines as we close out another lousy September week for markets. Investor concerns about the election and an expansion of the COVID outbreak continue to keep a lid on any market upside. Despite the rising concerns over COVID, the cruise lines are a notable bright spot this morning as Barclays upgraded the group.

Be sure to check out today’s Morning Lineup for a rundown of the latest stock-specific news of note, market performance in the US and Europe, trends related to the COVID-19 outbreak, and much more.

September has certainly been a rough month for stocks, and the charts below show just how consistent the selling has been. The chart on the left shows a composite chart of the S&P 500’s performance this month, and the one on the right provides an hourly breakdown of performance. To sum things up, when the market has been open, investors have been selling. Besides some ever so modest gains in the opening half-hour, the rest of the day consists of investors hitting bids and unloading stocks. While the 10-11 hour has seen the steepest losses, every other hour of the day from 11 AM on has also seen losses on an average basis. Looking on the bright side, after today there are only three trading days left in the month.

Bespoke’s Weekly Sector Snapshot — 9/24/20

The Bespoke 50 Top Growth Stocks — 9/24/20

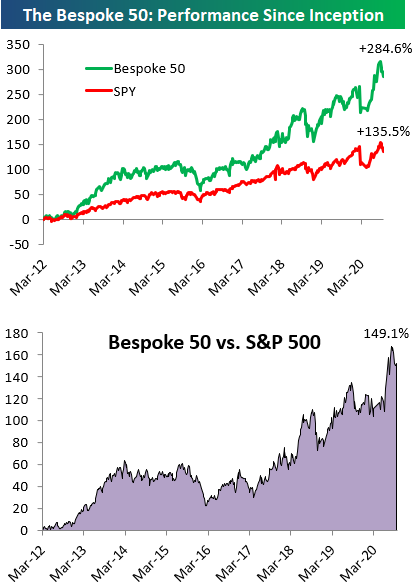

Every Thursday, Bespoke publishes its “Bespoke 50” list of top growth stocks in the Russell 3,000. Our “Bespoke 50” portfolio is made up of the 50 stocks that fit a proprietary growth screen that we created a number of years ago. Since inception in early 2012, the “Bespoke 50” has beaten the S&P 500 by 149.1 percentage points, which hit a new high this week. Through today, the “Bespoke 50” is up 284.6% since inception versus the S&P 500’s gain of 135.5%. Always remember, though, that past performance is no guarantee of future returns. To view our “Bespoke 50” list of top growth stocks, please start a two-week free trial to either Bespoke Premium or Bespoke Institutional.

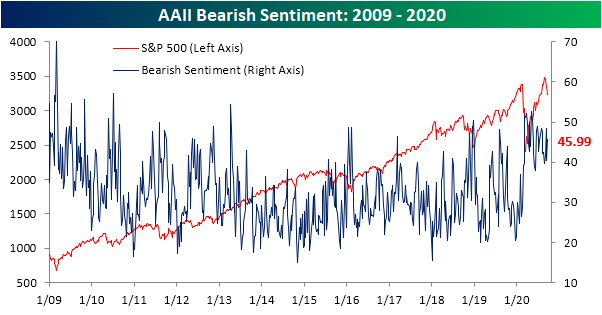

Bullish Sentiment Slipping and Sliding

Last week, when the S&P 500 was appearing to hold up at support at its 50-DMA, bullish sentiment managed to significantly rise to 32.02%. But in the week since then, the S&P 500 has taken another leg lower, falling below its 50-DMA and is now 9% from the September 2nd high. Today the index even briefly met the technical definition of a correction (10% decline from a high) on an intraday basis. Given this, bullish sentiment, as seen in the American Association of Individual Investors‘ weekly survey, has likewise taken a sizeable turn lower. Just 24.89% of responding investors this week reported as bullish. While lthis is a low reading, this week’s reading is actually slightly higher than two weeks ago (23.71%) following the initial drop from the highs.

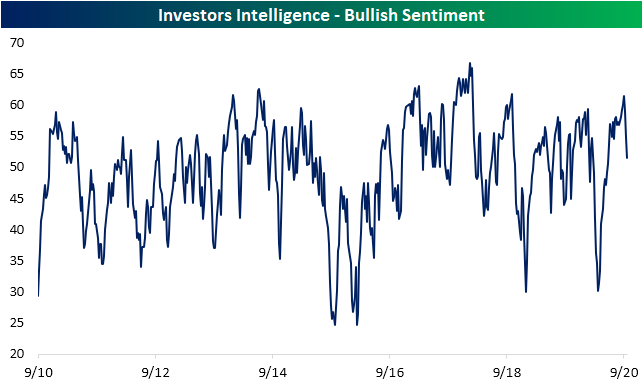

While the AAII survey has consistently held a bearish bias over the past few months despite the market rally, the Investors Intelligence survey of equity newsletter writers has been more optimistic. That is until the past few weeks. 51.5% of respondents to this survey are now reporting as bullish which is the lowest reading since the last week of May. Back at the September 2nd high, this survey showed 61.5% of respondents as bullish; the most since October of 2018. The 10 percentage point drop in that time was the largest decline in three weeks since March.

As a result of the losses in bullish sentiment, bearish sentiment in the AAII survey rose from 40.39% to 45.99%. Just as with bullish sentiment, there was a higher reading of 48.45% two weeks ago in the wake of the initial drop off the highs, but this week’s move returns bearish sentiment to levels seen throughout the spring and first half of summer.

With the inverse moves in bullish and bearish sentiment, the bull-bear spread widened to the low end of the past several month’s range at -21.1. The record streak of negative bull-bear spread readings has also continued to grow, now extending to 31 weeks.

Neutral sentiment was also higher this week rising to 29.11%, bringing the reading up to the same level as July 23rd. Click here to view Bespoke’s premium membership options for our best research available.