Chart of the Day: What Do Strong Beat Rates Mean For Q3 Earnings?

Bespoke Stock Scores — 10/13/20

Bespoke’s Morning Lineup – 10/13/20 – Good First Impression

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

“Grow or die, that’s what I believed, no matter the situation.” – Phil Knight, Shoe Dog

With earnings season kicking off in earnest this morning, the above quote is probably the mantra of most CFOs of public companies. If you can’t show growth, kiss your stock price goodbye. Thankfully for the market this morning, the results we have seen so far as of this writing have been positive. With the exception of Fastenal (FAST), which reported inline EPS and AZZ, which missed revenue forecasts, every other company that has reported this morning has topped both EPS and revenue forecasts. Sure, it’s only eight companies, but it’s a good start.

Be sure to check out today’s Morning Lineup for a rundown of the latest stock-specific news of note, market performance in the US and Europe, major earnings releases, economic sentiment, trends related to the COVID-19 outbreak, and much more.

Outside of the US, emerging market equities have generally lagged the S&P 500, but in the recovery off the September lows, emerging market equities have the distinction of taking out their early September highs before the S&P 500. Not only that but just yesterday, the Emerging Market ETF (EEM) managed to also make a marginal new 52-week high as well. If it can build on those gains in the days ahead, the breakout will be confirmed.

Speaking of breakouts, EEM has essentially been range-bound for the better part of thirteen years. Since making an all-time high in 2007, EEM has seen multiple rallies to the low to mid-$50s area only to pull back. EEM closed yesterday at $46.23, so it’s nowhere near testing resistance at multi-year highs yet, but it’s something to keep on the radar. When and if it makes new highs in the months ahead, it will mark a notable long-term breakout more than a decade in the making.

Daily Sector Snapshot — 10/12/20

Big Banks Reporting This Week

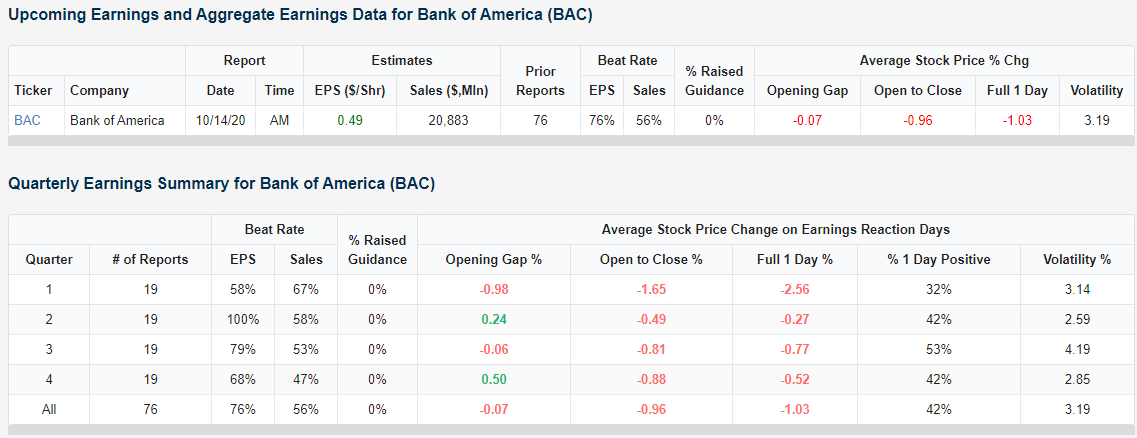

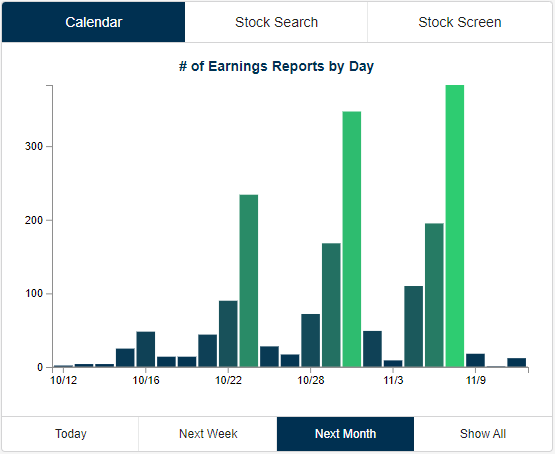

The third quarter earnings season begins this week with the first of the big banks set to report tomorrow morning. One feature of our Earnings Explorer tool is an interactive earnings calendar with detailed information on stocks set to report earnings in the days, weeks, and months ahead. Below is a snapshot of the calendar showing expected earnings reports through Wednesday morning. Notably, Citigroup (C) and JP Morgan (JPM) will report tomorrow morning, while Bank of America (BAC), Goldman Sachs (GS), and Wells Fargo (WFC) will report on Wednesday morning.

You can dig deeper into individual stocks with our Earnings Explorer tool to see their historical earnings reports and how investors reacted. Below we show aggregate earnings snapshots for both Citigroup (C) and JP Morgan (JPM), which report tomorrow ahead of the open.

Notably, the Q3 earnings release for Citigroup has seen the stock average a one-day gain of 0.87% in reaction to the news. That’s a better share price response than any other quarter. Following its historical Q4 earnings releases, for example, Citi shares have been very weak with an average one-day decline of 2.39%.

While Q3 earnings have been okay for Citigroup in terms of share price reaction, it has been the worst quarter of the year for JP Morgan (JPM) historically. Over the last 19 years, JPM has averaged a one-day decline of 0.73% on its Q3 earnings reaction day with positive returns just 26% of the time.

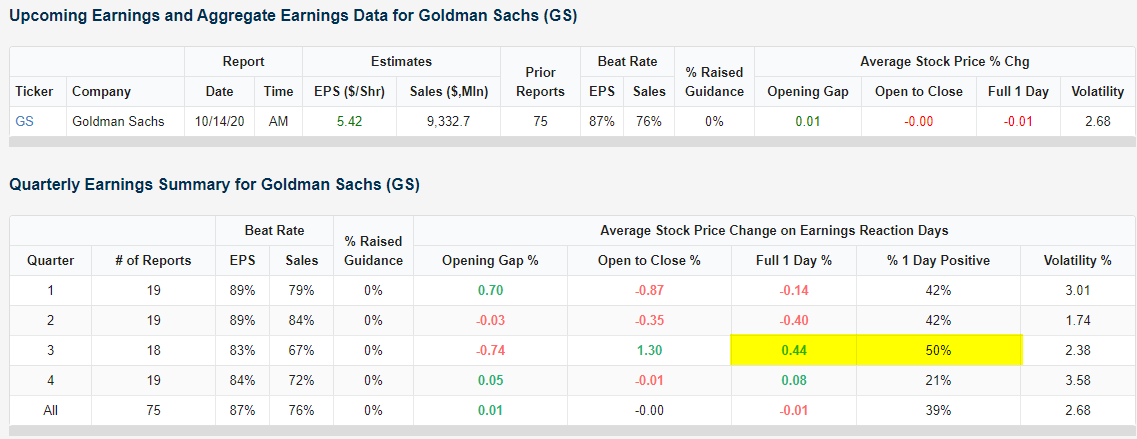

Bank of America (BAC) has the worst numbers of the five big banks reporting this week when it comes to share price reactions to earnings. As shown below, the stock has averaged a decline of 1.03% on its 76 earnings reaction days since 2001 with positive returns just 42% of the time. Goldman Sachs (GS) has also struggled on earnings historically with its share price rising in reaction to the news just 39% of the time. Goldman’s Q3 report, however, has been a bit more bullish with the stock averaging a one-day gain of 0.44% in reaction to past third quarter earnings releases. Finally, Wells Fargo (WFC) is also set to release Q3 earnings on Wednesday, and the stock has only gained in reaction to past Q3 releases 32% of the time. Try out our Earnings Explorer tool for free with a two-week trial to Bespoke Institutional.

Chart of the Day: AAPL Performance After iPhone Reveals

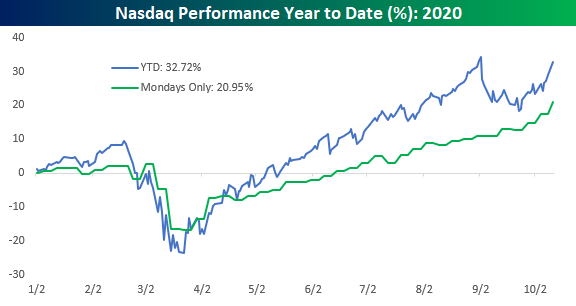

“Meet the Nasdaq”

Tim Russert used to sign off from each week’s episode of Meet the Press with the tagline, “If it’s Sunday, it’s Meet the Press.” Borrowing from that phrase, the Nasdaq’s tagline might as well be “If it’s Monday, it’s Meet the Nasdaq.” With a gain of over 3% today, the Nasdaq is doing what it always does on Mondays – rally! The chart below shows the year-to-date performance of the Nasdaq so far in 2020 as well as its performance if you only owned the index on Mondays. Year to date, the Nasdaq is up an impressive 32.7%, putting it on pace for the first back-to-back annual gain of over 30% since 1998 and 1999. Even crazier, though, is the fact that the Nasdaq is up over 20% year-to-date on Mondays alone! The weekday that most people love to hate has been responsible for more than 60% of this year’s Nasdaq gain.

In the table below we summarize the performance of the Nasdaq by weekday so far in 2020. Monday’s average daily gain of 0.57% with gains more than 75% of the time is both the best average daily return and the most consistent to the upside. Tuesdays and Wednesdays haven’t been particularly bad for the Nasdaq either. Both days have seen an average one-day gain of 0.30% or more, and Wednesday has been positive three-quarters of the time. While the first three trading days of the week have been strong, Thursday and Friday have been days to forget. Although both days have also experienced positive returns more than half of the time, the average one-day change for both is negative resulting in declines on a cumulative. Thursday has been the weakest with a cumulative decline of 11.53% while Friday’s cumulative decline has been more modest at just 3.46%. TGIM. Click here to view Bespoke’s premium membership options for our best research available.

Economic Data and Earnings In Earnest

Although a very busy news week made up for it, last week was uneventful on both the earnings and economic data front. In terms of earnings, only eight companies reported, and for economic data, as shown below, there weren’t even a dozen releases.

This week is another story. On the economic data front, there are more than two dozen releases crammed into Tuesday through Friday (there are no scheduled releases for today due to the Columbus Day holiday). Small business optimism will be the first release of the week early Tuesday morning. CPI will be out later in the day with PPI following up on Wednesday morning. Tuesday will also see manufacturing readings from the Philly and New York Fed, and we’ll get the usual Thursday weekly releases like jobless claims and Bloomberg Consumer Comfort. Friday closes out the week with retail sales, industrial production, University of Michigan sentiment, and TIC flows all on the docket.

Not only is economic data ramping up but so too are earnings. Whereas last week only saw 8 earnings reports, this week there are over ten times that number as earnings season kicks off with some of the big banks like Citi (C) and JPMorgan Chase (JPM) reporting. As shown in the snapshot from our Earnings Explorer below, the following three weeks will only see the number of companies reporting accelerate with peak earnings season in the first week of November. Click here to view Bespoke’s premium membership options for our best research available.

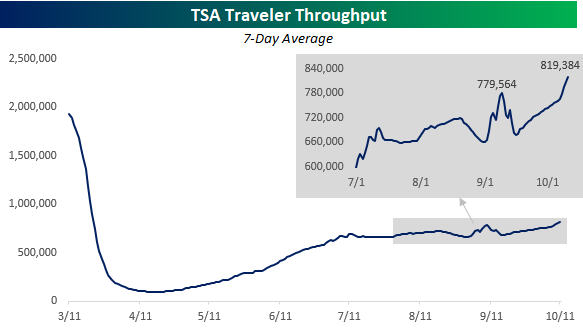

Air Passenger Traffic Achieves Upward Lift

With COVID case counts on the rise throughout the country, you would think that Americans would be a bit more concerned about getting on airplanes. Rather than hunker down, though, Americans have been increasingly spreading their wings. The latest passenger throughout numbers released by TSA showed that on Sunday 984,234 passengers went through security checkpoints at US airports. That was the highest single-day reading since March 16th. This weekend’s air passenger traffic also helped to push the 7-day average of traffic to new post-COVID highs. After rising and then falling back down after the Labor Day holiday, air passenger traffic has ‘surged’ in recent days to push the current 7-day average up to 819,384 passengers per day.

Air travel has been on the rise, but the term surge may be too strong. When we compare air passenger traffic levels to where they were a year ago, we’re still down over 65% on a 7-day average basis. Even yesterday’s strong passenger numbers were still down over 61% from their same levels last year. In other words, there’s still a lot of room for improvement! The chart below compares the y/y change in passenger throughput to the performance of the Airline ETF (JETS) since the start of the pandemic. Not surprisingly, there has been a pretty strong correlation between the two as increases in passenger traffic have been accompanied by rallies in the airlines and vice versa. Click here to view Bespoke’s premium membership options for our best research available.

Bespoke’s Morning Lineup – 10/12/20 – “Soft” Open

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

“Do more of what works and less of what doesn’t.” – Steve Clark

Due to the Columbus Day holiday, it’s a quiet start to the week in terms of data related to earnings and the economy, but equities are poised for a very strong start anyways as tech stocks lead the rest of the market higher. More specifically, it’s the software sector that’s driving the rally this morning, and one catalyst for the gains is the $3.2 billion takeover of Segment by software darling Twilio (TWLO). While stocks of the acquiring company usually take a hit when a merger is announced, this morning TWLO is trading more than 5% higher to record highs, and that comes after already tripling this year!

Be sure to check out today’s Morning Lineup for a rundown of the latest stock-specific news of note, market performance in the US and Europe, manufacturing in Japan, trends related to the COVID-19 outbreak, and much more.

On the topic of software, just last week the group looked to be starting to break out of a consolidation phase after underperforming the broader market since early September. Today’s rally should further the move out of congestion, but the group still enters the week trading down close to 5% from its prior high.

Bespoke

Bespoke