Dollar Down, Internationals Up

While risk assets are continuing their recent move higher today, the US dollar (as proxied by Bloomberg’s dollar index) is also reversing higher as it looks to end a four-day losing streak. As shown in the chart below, last week saw the dollar drop 1.93%; its worst stretch of five days since June 1st. While today’s rally is reversing some of those losses, last week’s move resulted in a break below support from the consolidation that had been occurring since mid-summer when the dollar fell below late 2019 lows. Although it is off the lows today, the dollar is currently around some of its lowest levels of the past two and a half years.

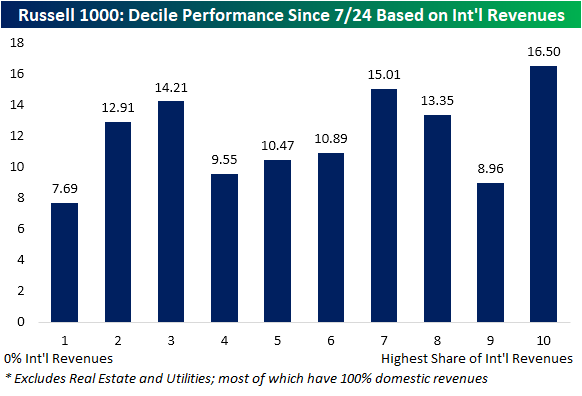

Assuming the dollar fails to move back above that prior support level, a weaker dollar means more attractive prices for US goods for foreigners, and as a result, that could bode well for companies with more international revenue exposure. Recently, that theory has held up fairly well. Using data from our International Revenues Database, in the chart below we created a decile analysis for performance since 7/24 (when the dollar first closed below December 2019 lows) of Russell 1000 stocks based on each stock’s percentage share of revenues that come from abroad. This excludes stocks in the Real Estate and Utilities sectors which generally have nearly all revenues coming from the US. As shown, since the dollar has been pressing to new multi-year lows, the group of stocks that has been the best performers have been those with the highest share of international revenues with an average gain of 16.5% since 7/24. Conversely, the 1st decile comprised of only the stocks with zero international revenues have underperformed with only a 7.69% gain. While not a perfect relationship given some outperformance of the second and third deciles and weakness of the ninth decile, at least at the extremes, more internationally exposed companies have been the top performers since the dollar’s leg lower earlier this year. Click here to view Bespoke’s premium membership options for our best research available.

Chart of the Day: Surges to Record Highs

Bespoke’s Morning Lineup – 11/9/20 – Happy Days on the Horizon?

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

“The fear, not the disease, threatened to break the society apart.” – John M. Barry, The Great Influenza: The Story of the Deadliest Pandemic in History

Futures were already looking to continue their big rally from last week earlier this morning, but the news that Pfizer’s COVID vaccine showed 90%+ effectiveness against infection has the S&P 500 indicated to open up over 4%! Not everything is rallying on the news, though. While the Nasdaq is also indicated to open up on the day, the biggest beneficiaries of the COVID economy are being sold en masse as investors rotate into the re-opening trades. Just as fear of the pandemic sank markets back in March, hopes for a vaccine are having the reverse effect.

Be sure to check out today’s Morning Lineup for a rundown of the latest stock-specific news of note, discussion of vaccine news, trends related to the COVID-19 outbreak, and much more.

What a wild morning for the market. There’s still a lot of time left in the day, but the S&P 500 is up over 4% in the pre-market while the Nasdaq is barely higher. If this performance gap continues throughout the trading day, it will be the widest margin of outperformance for the S&P 500 relative to the Nasdaq in nearly 20 years (1/2/01). Going back to 1990, there have only been nine other days where the S&P 500 outperformed the Nasdaq in a single day, and they all occurred between March 2000 and January 2001.

The Bespoke Report — Election Week 2020

Daily Sector Snapshot — 11/6/20

Bespoke Consumer Pulse Report — November 2020

Bespoke’s Consumer Pulse Report is an analysis of a huge consumer survey that we run each month. Our goal with this survey is to track trends across the economic and financial landscape in the US. Using the results from our proprietary monthly survey, we dissect and analyze all of the data and publish the Consumer Pulse Report, which we sell access to on a subscription basis. Sign up for a 30-day free trial to our Bespoke Consumer Pulse subscription service. With a trial, you’ll get coverage of consumer electronics, social media, streaming media, retail, autos, and much more. The report also has numerous proprietary US economic data points that are extremely timely and useful for investors.

We’ve just released our most recent monthly report to Pulse subscribers, and it’s definitely worth the read if you’re curious about the health of the consumer in the current market environment. Start a 30-day free trial for a full breakdown of all of our proprietary Pulse economic indicators.

Bespoke’s Morning Lineup – 11/6/20 – Time For a Break

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

“Happiness does not come from a job. It comes from knowing what you truly value, and behaving in a way that’s consistent with those beliefs.” ― Mike Rowe

There wasn’t much dirty about today’s jobs report. Non Farm, Private, and Manufacturing payrolls all topped expectations while the unemployment rate fell to 6.9% compared to forecasts for a level of 7.6%, Even the underemployment rate was less than expected at 12.1% compared to forecasts that were closer to 13%. All in all, a very good report relative to expectations, and that has been reflected in the futures market where rates are higher and equities are rebounding.

Be sure to check out today’s Morning Lineup for a rundown of the latest stock-specific news of note, election analysis, trends related to the COVID-19 outbreak, and much more.

You would think that after the week we’ve had in the market that the market and every sector would be trading at overbought levels, but as shown from page two of our Morning Lineup below, that isn’t quite the case. Three S&P 500 sectors currently remain in neutral territory, while Energy is closer to oversold than overbought! Also surprising is the fact that Technology is still one of the three sectors that aren’t overbought. Normally, after a rally like we’ve seen in the last week, Technology would be leading the charge, but that hasn’t quite been the case this week.

Gold in All Forms Glitters

What a day for gold today – both physically and in its ‘digital’ form. Gold prices are trading up 3% today as just about every asset class is up in price as the value of the dollar declines. After pulling back more than 11% from its August highs, the price of gold has broken its downtrend from that high.

Bitcoin is often referred to as ‘gold’ in a digital form, and it was certainly in rally mode today. With a one-day gain of over 7%, bitcoin is back above $15,000. Today’s move is actually only the largest upside move since 10/21, but it would be the first close above $15,000 since January 2018 and only the 18th time in the digital currency’s history that it closed above that level. Up until recently. there was an uptrend line where bitcoin rallies would run out of steam, but in the last two days, it has found some added fuel to push higher.

One bitcoin will currently buy a holder 7.7 ounces of gold which is the highest ratio since August 2019. The last time bitcoin was at 15,000, though, gold was much cheaper as a bitcoin would buy you more than 12 ounces of gold. Additionally, back in June 2019, the ratio between the two was just under 9. From the peak in late 2017, the ratio of bitcoin to gold made a series of lower highs, but back in July it finally broke above that downtrend range and has been off to the races ever since. Three years ago, the bitcoin mania that would grip markets in the last few weeks of 2017 was just starting to take off and conversations at Thanksgiving tables all over the country included a cousin, aunt, uncle, or even grandmother who was either bragging about getting rich or knew a person who was getting rich buying crypto. With bitcoin prices surging again this year heading into the holiday, we could be in for a repeat of those conversations again this year only instead of around the dinner table, it sounds like many of these conversations will be taking place over Zoom. Click here to view Bespoke’s premium membership options for our best research available.

Bespoke’s Weekly Sector Snapshot — 11/5/20

One Sentiment Survey Soars While Another Sinks

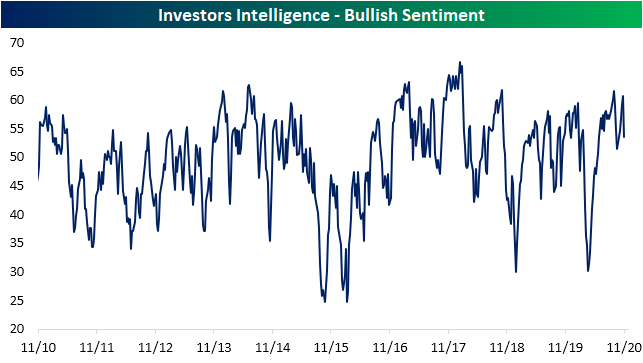

In an earlier post, we discussed how bullish sentiment in the AAII survey has been on the rise, but looking at another weekly sentiment survey from Investors Intelligence, the opposite is true. The percentage of respondents reporting as bullish fell sharply this week, 7 percentage points, down to 53.6%. While a majority are still optimistic and that reading is in the middle of its range, that was the largest weekly decline since a 7.4 percentage point decline to 41.7% in the first week of March.

Meanwhile, the percentage of newsletter writers that are “looking for a correction” rose sharply to 25.8% this week following last week’s over 5% decline for the S&P 500.

The Investors Intelligence survey has a long history dating back to 1963, and in all weeks in that time, only 5% (174 weeks) have seen bullish sentiment fall 5 percentage points or more while the percentage of respondents looking for a correction has risen at least 5 percentage points in the same week. In the chart below, we show the average performance of the S&P 500 following these past occurrences when there has not been another in the prior 3 months. The S&P 500 has frequently been higher over the following weeks and months, but there is a slight underperformance relative to all periods since 1963 when the survey begins. Click here to view Bespoke’s premium membership options for our best research available.