The Bespoke Report – A Good Month in Four Days

If you were expecting a bit of a pullback to start December after November’s big gains, it didn’t come this week. While November’s performance for the US and global equities was the equivalent of a good year, December’s MTD returns already would be considered a great month! Major US equity indices are all up 2% already, and the small-cap Russell 2000 is up close to 4%. Every sector with the exception of Utilities is also up on the month, but Energy is by far the biggest winner with a gain of over 10%. Even after that gain, though, it is still down nearly 30% on the year. In international markets, we’ve also seen big gains with countries like Brazil, Mexico, Spain, Russia, and the UK all up over 5%. Lastly, as one might expect given the big gains in equities, bonds are all lower on the month with the most weakness at the long end of the curve.

This week’s Bespoke Report is a bit shorter than normal as we have also started to publish various sections of our annual Bespoke Report Market Outlook. To view this week’s Bespoke Report as well as our Annual Outlook report as it’s published, take advantage of our 2021 Annual Outlook Special.

This week’s Bespoke Report newsletter is now available for members.

To read the report and access everything else Bespoke’s research platform has to offer, start a two-week free trial to one of our three membership levels. You won’t be disappointed!

2021 Outlook – Credit

Our 2021 Bespoke Report market outlook is the most important piece of research that Bespoke publishes each year. We’ve been publishing our annual outlook piece since the formation of Bespoke in 2007, and it gets better every year! In this year’s edition, we’ll be covering every important topic you can think of that will impact financial markets in 2021.

The 2021 Bespoke Report contains sections like Economic Cycles, The Fed, Sector Technicals and Weightings, Stock Market Sentiment, Stock Market Seasonality, Housing, Commodities, and more. We’ll also be publishing a list of our favorite stocks and asset classes for 2021 and beyond.

We’ll be releasing individual sections of the report to subscribers until the full publication is completed by year-end. Today we have published the “Housing” section of the 2021 Bespoke Report, focusing on the wild ride taken by credit markets over the course of 2020 and the outlook for 2021. We review the long-term history of corporate debt yields and spreads to benchmark interest rates, as well as looking at what the current backdrop implies for equity markets. We finish with a preview of what might become the biggest focus for credit markets in 2021.

To view this section immediately and all other sections, become a member with our 2021 Annual Outlook Special!

2021 Outlook – Housing

Our 2021 Bespoke Report market outlook is the most important piece of research that Bespoke publishes each year. We’ve been publishing our annual outlook piece since the formation of Bespoke in 2007, and it gets better every year! In this year’s edition, we’ll be covering every important topic you can think of that will impact financial markets in 2021.

The 2021 Bespoke Report contains sections like Economic Cycles, The Fed, Sector Technicals and Weightings, Stock Market Sentiment, Stock Market Seasonality, Housing, Commodities, and more. We’ll also be publishing a list of our favorite stocks and asset classes for 2021 and beyond.

We’ll be releasing individual sections of the report to subscribers until the full publication is completed by year-end. Today we have published the “Housing” section of the 2021 Bespoke Report, focusing on the recent data and outlook for housing markets and homebuilders. We review affordability, construction data, activity in the existing and new home markets, data and drivers for homebuilder stocks, and finally a review of the impact COVID has had on mortgage delinquencies.

To view this section immediately and all other sections, become a member with our 2021 Annual Outlook Special!

2021 Outlook – Washington

Our 2021 Bespoke Report market outlook is the most important piece of research that Bespoke publishes each year. We’ve been publishing our annual outlook piece since the formation of Bespoke in 2007, and it gets better every year! In this year’s edition, we’ll be covering every important topic you can think of that will impact financial markets in 2021.

The 2021 Bespoke Report contains sections like Economic Cycles, The Fed, Sector Technicals and Weightings, Stock Market Sentiment, Stock Market Seasonality, Housing, Commodities, and more. We’ll also be publishing a list of our favorite stocks and asset classes for 2021 and beyond.

We’ll be releasing individual sections of the report to subscribers until the full publication is completed by year-end. Today we have published the “Washington” section of the 2021 Bespoke Report, which recaps market scenarios under different political compositions in DC as well as some important comparisons between this election and 2016’s.

To view this section immediately and all other sections, become a member with our 2021 Annual Outlook Special!

2021 Outlook – Valuation

Our 2021 Bespoke Report market outlook is the most important piece of research that Bespoke publishes each year. We’ve been publishing our annual outlook piece since the formation of Bespoke in 2007, and it gets better every year! In this year’s edition, we’ll be covering every important topic you can think of that will impact financial markets in 2021.

The 2021 Bespoke Report contains sections like Economic Cycles, The Fed, Sector Technicals and Weightings, Stock Market Sentiment, Stock Market Seasonality, Housing, Commodities, and more. We’ll also be publishing a list of our favorite stocks and asset classes for 2021 and beyond.

We’ll be releasing individual sections of the report to subscribers until the full publication is completed by year-end. Today we have published the “Valuation” section of the 2021 Bespoke Report, which compares current valuations for major indices and sectors to their historical levels at various points in bull and bear markets. We also analyze the earnings yield, price to book ratios, and dividend yields for the S&P 500 relative to history.

To view this section immediately and all other sections, become a member with our 2021 Annual Outlook Special!

Daily Sector Snapshot — 12/4/20

Bespoke’s Morning Lineup – 12/4/20 – Positive Tone into Jobs Report

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

“I buy when other people are selling.” – J. Paul Getty

It’s safe to assume then that Mr. Getty hasn’t been buying much lately. Futures are higher again this morning putting the S&P 500 on pace for its fourth positive week in the last five, but in order to get there, we’ll have to get through the November jobs report. There have been some concerns about the health of the jobs market lately, but secondary indicators we track have been holding up relatively well.

Be sure to check out today’s Morning Lineup for updates on the latest market news and events, a discussion of the latest OPEC talks, factory orders in Germany, an update on the latest national and international COVID trends, and much more.

We’ve illustrated the positive breadth in the market in a number of different ways lately, but here’s another. For the last few days now, all 24 of the S&P 500’s Industry Groups have been trading above their 200-DMA. Looking back at the last five years, that doesn’t happen all that often. The last time there was such a high reading was at the start of the year on January 2nd. While the year may be on pace to finish right where it started in terms of breadth, it was far from a straight line as this reading went from 100% down to 0% and back to 100%. You can’t get any wider of a range than that!

Bespoke’s Weekly Sector Snapshot — 12/3/20

Bearing Down Into The Holidays

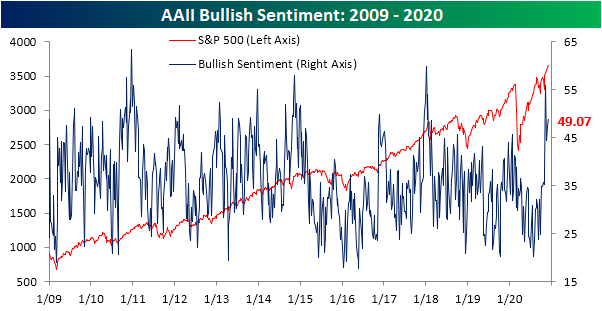

The S&P 500 has pressed to more all-time highs, and as a result, sentiment has turned even more bullish. In this week’s AAII sentiment survey, nearly half of the respondents (49.07%) reported a bullish. That is up for a second week in a row and remains at some of the highest levels of the past few years, though, it is more moderate than the reading from the first week after the election when over 55% reported as bullish.

While bullish sentiment is still off its recent highs, bearish sentiment has continued to press to new lows. 22.66% of respondents reported as bearish this week. That is down from 27.47% last week and is the lowest reading for bearish sentiment since the final couple of weeks of last year and the first week of 2020.

Given this, the bull-bear spread remains widely in favor of bulls, but off of its highs from a few weeks ago. Just like bullish sentiment, it is still at some of the highest levels of the past few years. Outside of the early November high, the bull-bear spread is at the highest level since February 2018.

Neutral sentiment is perhaps the most normal of the sentiment categories. While bullish and bearish sentiment readings are several percentage points away from their historical averages, at 28.25% neutral sentiment is only 3.19 percentage points below its historical average. Click here to view Bespoke’s premium membership options for our best research available.

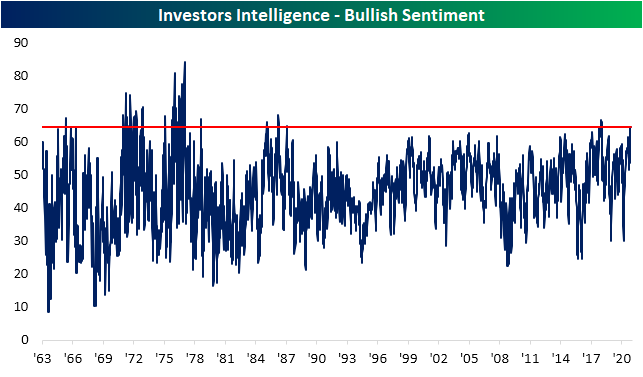

Equity Newsletter Exuberance

As we discussed in an earlier post, sentiment, as proxied by AAII’s weekly survey, has been overwhelmingly bullish. Other sentiment surveys are echoing the exuberance among investors. The Investors Intelligence survey of equity newsletter writers likewise saw bullish sentiment rise again this week from what were already strong levels. 64.7% of respondents reported as bullish this week. That is in the top 3% of all readings in the history of the survey. The last time this reading on bullish sentiment was this elevated was in January of 2018. Prior to that, you would need to go all the way back to February of 1987 to find a time that a higher share of respondents reported as bullish.

Meanwhile, just 16.7% of the respondents reported as bearish. While not at the same sort of extreme as bullish sentiment (in the bottom 13% of all readings), that is the lowest reading since early September.

In addition to gauging bearish sentiment, the report also measures the percentage of respondents that are “looking for a correction”. This reading ticked slightly higher this week rising from 18.2% up to 18.6%. While slightly higher, that is still in the bottom 20% of all readings across the history of the survey. More recently, though, this was more of an extreme low. Last week’s reading of 18.2% was the lowest reading since December of 2006. Click here to view Bespoke’s premium membership options for our best research available.