B.I.G Tips – Sentiment on the Rise

Solar and Steel Shining, Biotech Bounces, and Miners Moving

Looking across the ETFs in the US Groups screen of our Trend Analyzer, by far the best performer over the past week has been the Solar ETF (TAN). In just five days, TAN has managed to rally 11% roughly cutting in half what had been a 20% YTD decline through last week. Even after that rally though, after stellar returns last year, TAN is still the worst performer of this group of ETFs in 2021. Given it had traded in oversold territory for most of the past two months, TAN’s recent rally has not even been enough to bring the ETF back above its 50-DMA. TAN is not alone in being an ETF to see rotation in the past week after YTD weakness though. For example, biotech ETFs like the S&P Biotech ETF (XBI) and Nasdaq Biotechnology ETF (IBB) have both been strong over the last week after underperforming YTD,

Not all YTD losers have seen outsized gains in recent trading though. Both gold miner ETFs – GDX and GDXJ – are down YTD but have only seen marginal gains over the last week.

The Steel ETF (SLX) has also gone on an impressive run in the last week as the fourth best performing ETF in the screen. That has helped make it one of the strongest YTD performers putting it into extreme overbought territory as it trades 13% above its 50-DMA.

Some of these recent moves have resulted in some interesting developments in the various charts of these same ETFs which we show in the snapshot of our Chart Scanner below. Circling back to the gold miners, GDX has been in rally mode over the past couple of months resulting in it moving back above its 50-DMA and breaking its downtrend in the process. That does not mean GDX is totally out of the woods. So far the ETF has come up short of its 200-DMA which will be an interesting area of resistance to watch going forward. Similarly, after erasing some of the huge run in 2020, TAN (bottom left) managed to find support around $81 at multiple points in the past several weeks with the most recent test of this level being exactly a week ago. The huge 11% rally in the days since has brought it back up to its 50-DMA which it so far has failed to move back above. Conversely, IBB had been stuck between both its 50 and 200-DMAs since late February, but the recent bounce off of its 200-DMA preceded a breakthrough of its 50-day to the upside that has taken place over the past few days.

As for the other ETFs in our US Groups screen, there are multiple ones like the North American Tech-Multimedia Networking ETF (IGN), Semiconductors (SMH), and Regional Banking ETF (KRE) that have been rallying off of their 50-DMAs and moving back up towards 52-week highs. In the case of IGN, that has resulted in what appears to be an upside break of the past few months’ wedge pattern. There are also other breakouts to new 52-week highs like for the US Financial Services ETF (IYG) and the S&P Metals and Mining ETF (XME). Click here to view Bespoke’s premium membership options for our best research available.

Bespoke’s Morning Lineup – 4/27/21 – Earnings Remain Strong

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

“When Henry Ford made cheap, reliable cars people said, ‘Nah, what’s wrong with a horse?’ That was a huge bet he made, and it worked.” – Elon Musk

The pace of earnings reports has picked up steam considerably, but the pace of earnings beats has remained strong so far. This morning, nearly 80% of companies reporting have topped EPS forecasts and more than 70% have topped revenue forecasts. All in all, a strong showing. We’re also even seeing a number of positive price reactions to the companies reporting with UPS being a notable winner in early trading.

Read today’s Morning Lineup for a recap of all the major market news and events including the biggest overnight events, some key earnings reports, economic data from around the world, as well as the latest US and international COVID trends including our vaccination trackers, and much more.

The S&P 500 hit an all-time high yesterday, and overall breadth has remained positive. One example we wanted to highlight this morning is the fact that of the 62 industries within the S&P 500, 49 (79%) are within 5% of a 52-week high, and 21 (34%) are within 1% of a high. That leaves just 13 industries (21%), which are highlighted in the chart below, down more than 5% from their respective 52-week highs. Leading the way to the downside, Energy Equipment is down nearly 17% after its blistering rally late last year and early this year while the Autos group is down just over 14%. Another notable industry in the group is Technology Hardware, which is basically a proxy for Apple (AAPL). That’s the only industry from the Technology sector in the group that is down over 5%, but we did find it interesting that two other industries with the word ‘technology’ in them are also included- Biotechnology (-5.02%) and Health Care Technology (-10.2%).

Daily Sector Snapshot — 4/26/21

Tesla (TSLA) Earnings On Deck

Tesla’s (TSLA) much anticipated first-quarter results will be out after the closing bell this afternoon. The company is expected to report EPS of $0.73 and sales of $9.887 billion which would represent 65% YoY growth from last year. While that would be impressive growth versus a year ago, when it comes to stock price reaction in tomorrow’s session, Q1 earnings are usually somewhat underwhelming. As shown in the snapshot of our Earnings Explorer below, Q1 earnings have seen a positive reaction the least often of any quarter for TSLA with the stock finishing the day after earnings in the green only 30% of the time and down in each of the last five Q1 reports. Additionally, the average full-day gain of 0.25% is the second smallest move higher of any quarter next to the 0.1% average gain in Q4. Although the full-day average performance has not necessarily been the worst, Q1 has averaged the worst returns from open to close with a decline of 1.93%.

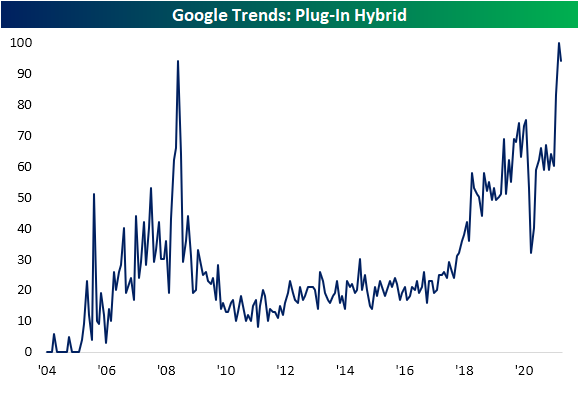

Regardless of the results, the overall trends for the EV market have been pretty positive recently based on Google Trends data. So far in 2021, searches under the Autos and Vehicle categories for “Plug-In Hybrid” have surged to record highs. Even after pulling back in April, current levels of searches are stronger than almost any point in the past. The same goes for searches of charging stations. Given people who already own an EV would be searching for charging stations, this would perhaps be a better read-through for the number of people who own and are using their EVs. Even at a time of year that searches for the term are seasonally weak, the current levels of search interest are at a historically strong level meaning EVs are more popular on the road. Click here to view Bespoke’s premium membership options for our best research available.

Another Day, Another Strong Manufacturing Survey

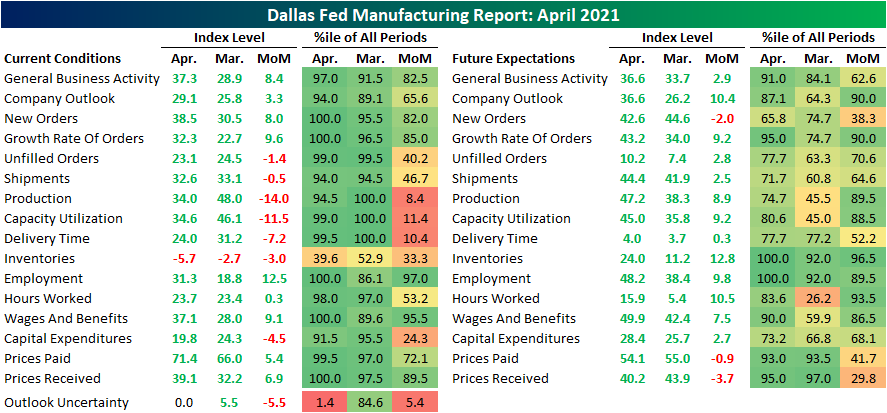

Monday’s monthly report from the Dallas Fed showed yet another strong reading on the manufacturing sector. The headline index tracking the region’s General Business Activity came in at the highest level in just under three years, rising 8.4 points to 37.3. Not only was that a multiyear high, but this month’s reading is also in the top 3% of all months since the start of the survey in 2004. Expectations also are optimistic with the index rising to the strongest level since September 2018. The indices for Company Outlook similarly rose to levels not seen since 2018.

Given businesses are reporting as more optimistic, uncertainty continues to fall. In fact, the Outlook Uncertainty Index fell to zero this month which indicates that uncertainty among the region’s manufacturers is no longer on the rise. While there is not nearly as extensive of a history of this index as the rest of the survey (only dating back to 2018), this was the first non-positive reading since May 2018.

With strong readings in broader measures of activity, the majority of indices in the report remain in the top percentiles of readings. The only exception is Inventories which is in the bottom 40% of readings after falling 3 points this month. On the other hand, there were several indices like those for New Orders and Employment which were at the highest levels on record. Those strong readings do come with a caveat though. Breadth in this month’s report was a bit mixed with just over a half-dozen indices falling month over month. Despite these indices all staying in the top decile of readings after those declines, we would note that the drops in the indices for Production, Capacity Utilization, and Delivery Times were historically large for a single month.

Taking a more granular look at these indices, demand continues to grow at a historically strong clip. Both indices for New Orders and the Growth Rate of Orders rose to record highs. In spite of the acceleration in demand, the index for Unfilled Orders was actually slightly lower falling 1.4 points. That indicates that with surging new orders, backlogs continued to grow in April but actually at a slower pace than March. Even after that deceleration, though, Unfilled Orders sit well above the vast majority of historical readings. Shipments similarly pulled back ever so slightly in April indicating the region’s businesses are trying to match that demand.

The bigger declines came out of the indices for Production and Capacity Utilization. Again, these indices still sit at strong levels well above past years’ readings but did markedly decelerate in April. Comments highlighted in the release help to give some anecdotal evidence as to the reasons why production has hit the brakes. A few common themes throughout the comments include the impact of winter storms, rising prices (especially for inputs and freight), a lack of labor, and supply chain strain.

Other areas of the report back up those claims. Regarding prices, Prices Paid rose for the ninth month in a row topping 70 for the first and only time since October 2004. Meanwhile. those price increases are being passed along as the index for Prices Received rose to a record high.

Employment was another area that was frequently flagged as a concern among reporting businesses. Many comments noted the difficulty in hiring even with generous pay offers. Even though there seems to be trouble finding enough workers, workers are coming back at a historic rate. The index for Employment (both current conditions and expectations) marked the highest level to date as did Wages & Benefits. Additionally, the month-over-month rises in the indices stand in the top few percent of all months in the history of the survey. In other words, businesses are and want to continue to take on more employees and are raising pay to do so. On top of raising headcounts, Capital Expenditures also continue to grow although there was some deceleration in April. Click here to view Bespoke’s premium membership options for our best research available.

Chart of the Day – Gravity-Defying Equities

Bespoke’s Morning Lineup – 4/26/21 – Earnings Deluge

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

“Focus and simplicity…once you get there, you can move mountains.” – Steve Jobs

The S&P 500 closed just 0.33% from an all-time high on Friday, and futures are mixed heading into the new trading week. S&P 500 futures are flat, Dow futures are higher, and the Nasdaq is indicated lower.

Whether the week finishes at new highs or not will likely depend on earnings as this week will be the biggest week for earnings of the earnings season, including reports from the largest companies in the S&P 500. To kick off the week, we have seen ten reports cross the wires so far, and not a single one of them missed EPS forecasts. Whether these reports translate into positive returns in each of the company’s stocks, however, is hardly a foregone conclusion the way things have been playing out lately.

The pace of reports will pick up considerably after the close with more than 30 reports, including Tesla (TSLA) and NXP Semi (NXPI).

Read today’s Morning Lineup for a recap of all the major market news and events including the biggest overnight events, some key earnings reports, economic data from around the world, as well as the latest US and international COVID trends including our vaccination trackers, and much more.

Maybe it’s because of the earnings reports that we typically see at this time of year, but historically the period spanning the last few days of April and the first days of May haven’t been particularly friendly for bulls. The snapshot below from our Seasonality Tool shows that over the last ten years the S&P 500’s median performance from the close on 4/26 out through the next week has been a decline of -0.09%. That ranks in just the 30th percentile relative to all other one-week periods throughout the year. Looking out over the next month, the median return has been a gain of 0.56% which, while positive, still ranks in just the 34th percentile relative to other one-month periods. While the short-term returns have been on the weak side, longer-term, the S&P 500’s median return over the upcoming three months has been a gain of 3.71% which actually ranks in the 73rd percentile.

Bespoke Brunch Reads: 4/25/21

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, join Bespoke Premium with a 30-day free trial!

Conservation

The destructive green fantasy of the bitcoin fanatics by Jamie Powell & Jemima Kelly (FT)

When you’re not assuming an outcome and backfilling whatever it takes to get to there, Bitcoin is very simply a massive, energy intensive polluter fueled by dirty coal power. [Link; paywall]

The Chip Shortage Is Bad. Taiwan’s Drought Threatens to Make It Worse. by Stephanie Yang (WSJ)

With explosive demand driving a massive chip shortage around the world, Taiwan Semi is facing a huge problem: no water, a critical input for semiconductor manufacturing. [Link; paywall]

YOLO

Robinhood, Three Friends and the Fortune That Got Away by Rachel Louise Ensign (WSJ)

Tracking the progress of three amateur investors through the pandemic and the hundreds of trades that were part of a massive boom in retail trading last year. [Link; paywall]

Welcome to the YOLO Economy by Kevin Roose (NYT)

With vaccinations available, equity markets ripping, and crypto booming, early middle-age Millennials are flipping over the carefully arranged tables of their lives to seize the day. [Link]

It’s not NBA Top Shot, Beeple or a tweet, but IBM is about to turn patents into NFTs by Eric Rosenbaum (CNBC)

IBM and intellectual property specialist IPwe are collaborating on an effort to tokenize patents via the company’s blockchain platform, though it’s not entirely clear how tokenization would increase pattern liquidity. [Link]

Credit

A $1 Trillion Liquidity Surge Is Morphing Into a Leverage Boom by Paul Seligson (Bloomberg)

Pandemic borrowing that helped companies fortify their cash position during the pandemic is being redeployed to M&A, stock buybacks, and dividend hikes. [Link; soft paywall]

Vaccines

High Efficacy of a Low Dose Candidate Malaria Vaccine, R21 in 1 Adjuvant Matrix-M™, with Seasonal Administration to Children in Burkina Faso by Mehreen S. Datoo et al (SSRN)

A new malaria vaccine produced in partnership with Novavax has been shown to be 55.8% effective, a major step towards a widely available vaccine for a disease that kills roughly 1mm people per year around the world. [Link]

Vaccines Won’t Protect Millions of Patients With Weakened Immune Systems by Apoorva Mandavilli (NYT)

While vaccines are highly effective for those with functioning immune systems, millions of people won’t be protected by them due to other conditions; for them, monoclonal antibodies may be the only option. [Link; soft paywall]

Sports

New Jersey border towns surpass Las Vegas as sports gambling hotspot by Chris Sheridan (Basketball News)

Legalized sports betting venues in Fort Lee, New Jersey are regularly pulling in more betting action than the entire state of Nevada as bettors flock in from the Empire State. [Link]

Where Do QBs Come From (ESPN)

Louisiana and New York are by far the standouts when it comes to producing quarterbacks, and while Texas may be a football powerhouse by any other definition it ranks far and away the worst of any state when it comes to players under center. [Link]

Clout

Hip-Hop Loves Cash App, and That Might Be Why Jack Dorsey Bought Tidal by Grant Rindner (GQ)

Venmo was first in the free payment app space, but CashApp has been the big winner thanks to wild popularity in the South that was spread and amplified by the affection of hip hop. [Link]

Instagram star cat dies from injuries after boy trips on leash by Craig McCarthy & Jackie Salo (NYP)

A cat with more than 33,000 on Instagram was killed this week after a boy tripped on the feline’s leash, sparking a major brawl which also included the owners’ pet dog and bird. [Link]

Scarcity

Why are Hawaii visitors cruising around in U-Hauls? Blame the pandemic. by Chelsea Davis (Hawaii News Now)

Rental cars are so scarce in Hawaii that tourists are renting U-Hauls to get around the island during visits from the mainland. [Link]

South Florida restaurant buys robots to fight staffing issues by Michael Hollan (NYP)

A crab shack in South Florida has purchased three robots to take over some front-of-house tasks that typically would be performed by human staff. [Link]

Tragedy

The Fort Bragg Murders by Seth Harp (Rolling Stone)

Fort Bragg in Fayetteville, North Carolina has hosted a rash of deaths ranging from suicides to homicides, with more than 40 troops stationed at the base dying in 2020 alone. [Link]

Read Bespoke’s most actionable market research by joining Bespoke Premium today! Get started here.

Have a great weekend!

The Bespoke Report Weekly Newsletter– 4/23/21

This week’s Bespoke Report newsletter is now available for members.

At 1 PM ET on Thursday, the S&P 500 was trading up nicely on the day and then suddenly dropped on news headlines that President Biden’s upcoming infrastructure/tax hike proposal would include an increase in the capital gains tax on high earners from ~20% up to ~40%. It was curious that the market fell at all on this headline given that this type of tax hike was something Biden ran on during his campaign, but nevertheless, major US indices continued to fall for the remainder of the trading day to finish down roughly 1% on the day.

The worries — at least as far as the market is concerned — didn’t last long. 26 hours later at the close on Friday, the S&P 500 tracking SPY ETF closed exactly 1 cent below the level it was trading at as of 1 PM ET on Thursday!

Overall, US index ETFs were slightly lower on the week but remain up 3-6% in April and 8-20% YTD. Most sectors finished the week lower, although Health Care, Industrials, and Materials managed to post gains. China (ASHR) had a strong week, up 4.4%.

As usual, this week’s Bespoke Report covers the major forces that are driving equity markets right now. To read the report and access everything else Bespoke’s research platform has to offer, start a two-week free trial to one of our three membership levels. You won’t be disappointed!