Bespoke Stock Scores — 6/8/21

Brazil Boils

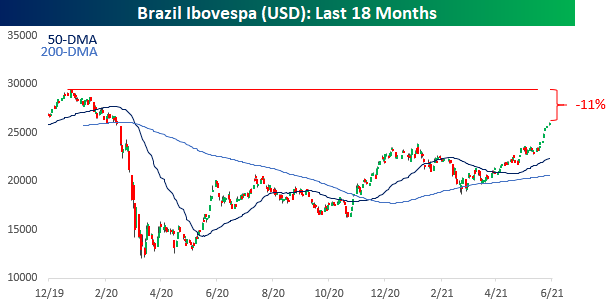

It’s been a hot time for stocks in Brazil over the last several days. The country’s benchmark Ibovespa index broke out above its highs from early this year completing a cup and handle formation and hasn’t looked back since. Yesterday was the index’s eighth straight day of gains during which the index has rallied more than 6%. This morning, the country is in the spotlight again as Berkshire Hathaway (BRK.b) has agreed to buy a $500 million stake in Nu Pagamentos SA, valuing the company at $30 billion. You may have never heard of Nu Pagamentos, but it is a privately held company that does business under the name Nubank, which is the largest fintech company in Latin America.

With the recent weakness in the dollar, the rally in Brazilian equities has been even stronger for US-based investors. During the same eight-day winning streak, the Ibovespa is up over 12% is USD. As shown in the chart below, though, while dollar weakness has flattered returns for Brazilian equities from a US-based investor’s perspective in the short-term, it’s been the opposite pattern over the longer term. While the Ibovespa is well above its early 2020 highs in local currency terms, on a dollar-adjusted basis, it’s still down 11%. Click here to view Bespoke’s premium membership options.

B.I.G. Tips – Charts We’re Watching

Bespoke’s Morning Lineup – 6/8/21 – Six or Twelve

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

“You can only do so many things great, and you should cast aside everything else.” – Tim Cook

Depending on whether you look at closing or intraday levels, the S&P 500 closed out yesterday within six or twelve points of a record high. This morning, equity futures are up relative to Monday’s close, and the way things are going now, that closing high from a month and a day ago will be topped at the open.

The economic calendar is light today. NFIB Small Business Optimism for May was released earlier, and while economists were expecting a modest bounce from April’s level, the actual reading showed a modest decline (99.6 vs 101.0 consensus estimate and 99.8 in April). A key theme from this month’s report was the fact that almost half of all small businesses said they have been unable to fill open positions. As an example, 93% of small business owners hiring or trying to hire reported that they received few or no qualified applications. We’re also likely to see a reinforcement of this trend later this morning when the JOLTS survey shows another likely record number of job openings despite the fact that job creation has been less impressive than forecasts.

Read today’s Morning Lineup for a recap of all the major market news and events including a discussion of the Biogen Alzheimer’s treatment, a recap of activity and economic data overnight, and the latest US and international COVID trends including our vaccination trackers, and much more.

Yesterday marked the beginning of the annual Worldwide Developers Conference (WWDC) from Apple (AAPL). While the company has been holding this event for over 30 years, its popularity really exploded following the launch of the iPhone in 2007. The conference first sold out in 2008 after Steve Jobs announced in October 2007 that Apple would open the iPhone up for developers to write software. The WWDC has historically been a noteworthy event for people involved in the development of Apple products, but it hasn’t historically been a great period for the stock.

The table below shows the performance of AAPL stock leading up to and during every prior WWDC in the iPhone era and since the conference first sold out in 2008. This year marks only the fourth time in the last 14 years where AAPL’s stock was down YTD heading into the conference. During the conference, though, performance has been on the weak side averaging a decline of 1.43% (median: -1.15%) with positive returns only four out of 13 times.

Daily Sector Snapshot — 6/7/21

Orcale (ORCL) Surges Above Price Targets

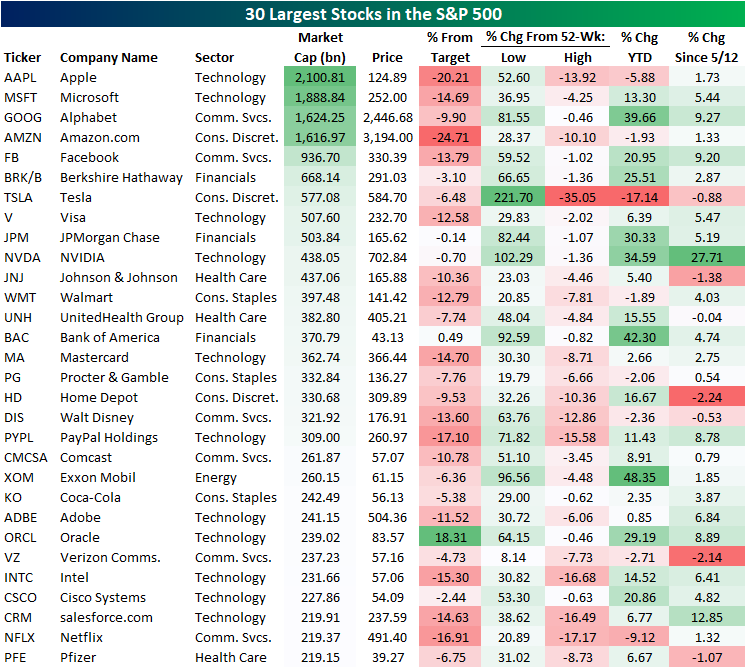

Thus far in 2021, most of the 30 largest S&P 500 stocks are in the green on a year-to-date basis with a few notable exceptions. The largest company with a $2.1 trillion market cap, Apple (AAPL), has fallen 5.88% year-to-date and is down nearly 14% from its 52-week high. Of the 30 largest stocks, the only two other stocks that are down by more year-to-date and are also further below their 52-week highs are Netflix (NFLX) and Tesla (TSLA). TSLA has been particularly hard hit with a 17% loss so far in 2021 which brings it down 35% from its high. Conversely, Alphabet (GOOG), JPMorgan Chase (JPM), NVIDIA (NVDA), Bank of America (BAC), and Oracle (ORCL) are some of the stocks that are closest to new highs (around 1% away) and are up around 30% or better YTD. Unsurprisingly for an Energy sector stock, the best performer this year has been Exxon Mobil (XOM) which is closing in on a 50% gain YTD.

After setting new record highs right around a month ago, the S&P 500 pulled back to its 50-DMA which it found support at on May 12th. The subsequent rally since then has seen the index make a run back up to those record highs which it has been hovering around in recent days. Since its May 12th low, by far the two best-performing stocks in the 30 largest stocks have been NVIDIA (NVDA) which has gained 27.71%, and salesforce.com (CRM) which has risen a smaller, but still impressive, 12.85%; both companies reported triple plays in late May which partially played a role in that strength. While far from a leader, AAPL is also up in that time as is the rest of the trillion-dollar market cap club.

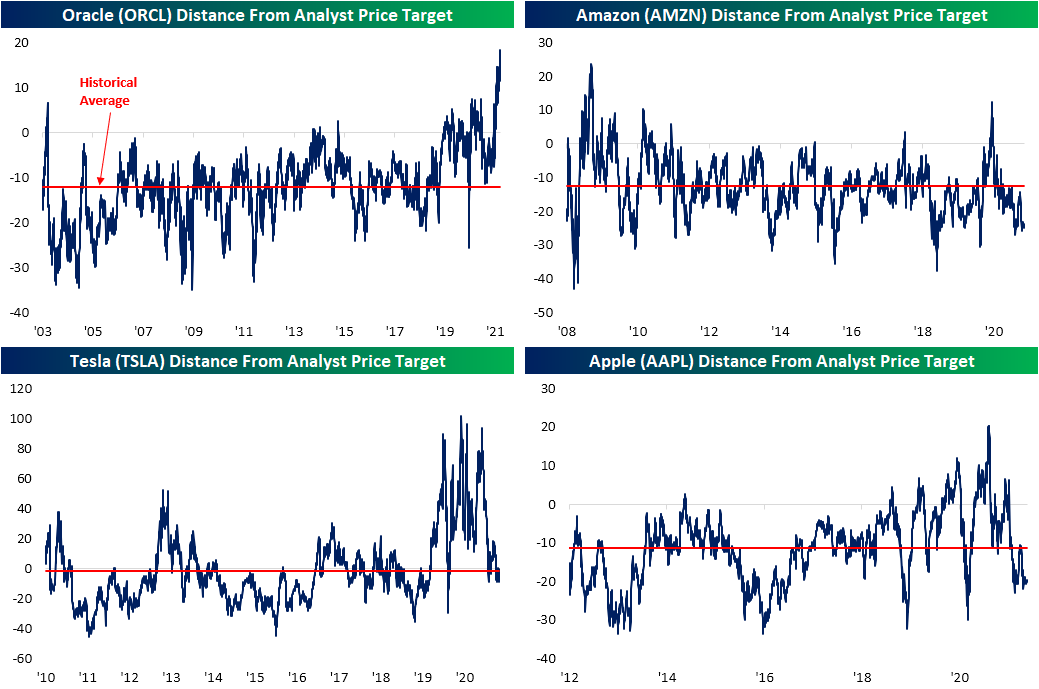

Another interesting thing to note of the stocks in the table above is their distances from their analyst price targets. There are a handful like JPMorgan Chase (JPM), NVIDIA (NVDA), and Bank of America (BAC) that are currently within 1% of their consensus price targets. After their strong runs this year, though, the median distance from a target for the full list is approximately 10% below. BAC is actually slightly above its target, and not many others can say that. In fact, the only other name of the largest stocks currently trading above its analyst price target is Oracle (ORCL), and it’s doing so in a big way. As shown above, ORCL is currently over 18% above its target. Going back through the history of the data for the stock, no other period since 2003 has seen ORCL trade as elevated above its target as it does now. For ORCL to get back below its average price target, either its share price would need to fall or analysts would need to significantly increase their price targets.

Looking at the other end of the spectrum, Amazon (AMZN) and Apple (AAPL) are the two names furthest below their price targets. For each of these stocks, trading that far below the analyst price target has been relatively uncommon over the past several years. For these two stocks to get back to where they normally sit relative to analyst price targets, either the stocks need to rise or analysts need to lower their price targets. For these two mega-cap behemoths, we think the latter is more likely.

While it does not stand out from the list of the other largest stocks as it only trades 6.5% below its target, TSLA is also notable. Over the past two years, the stock has continuously left its targets in the dust on average sitting 26% above. In July of last year, TSLA’s price even doubled the target price. But with the stock’s weakness this year, its distance from its price target is much closer in line with the historical average. Click here to view Bespoke’s premium membership options.

May 2021 Headlines

Chart of the Day – Energy Leads But Still Lags

Bespoke’s Morning Lineup – 6/7/21 – Drifting into Positive Territory

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

“We contend that for a nation to try to tax itself into prosperity is like a man standing in a bucket and trying to lift himself up by the handle.” – Winston Churchill

Futures started off with a negative bias this morning but have been drifting higher all morning and are now modestly positive for both the S&P 500 and Dow, while the Nasdaq is just barely lower. Treasury yields are higher, but the 10-year yield is still well below 1.6%, and even bitcoin is following the lead of equities and moving further into positive territory. It was a mixed weekend for the crypto-currency as China appears to be cracking down on the space while El Salvador said it will recognize bitcoin as legal tender.

Read today’s Morning Lineup for a recap of all the major market news and events including a discussion of the Global Minimum Tax, a recap of activity in Asia and Europe, and the latest US and international COVID trends including our vaccination trackers, and much more.

With the S&P 500 inching closer to new highs last week, the majority of sectors also traded higher. With crude oil continuing to rally towards 52-week highs, the Energy sector surged nearly 7% taking its YTD gain to nearly 50%. Behind Energy, four other sectors were up over 1%, and there are now four sectors that are already up over 20% YTD. Talk about a strong year!

On the downside, only two sectors were down last week (Consumer Discretionary and Health Care). Consumer Discretionary is the only sector trading more than 1% below its 50-day moving average and one of just two sectors (Utilities being the other) that finished the week below that level.

Bespoke Brunch Reads: 6/6/21

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, join Bespoke Premium with a 30-day free trial!

New Research

Why Do Borrowers Default on Mortgages? A New Method For Causal Attribution by Peter Ganong & Pascal J. Noel (NBER Working Papers)

What drives default on mortgages? The authors estimate that roughly 97% of all mortgage defaults take place because of an adverse shock which leaves borrowers unable to cover their monthly payment, not because they are strategically walking away from an LTV over 100. [Link; soft paywall]

How Teach for America Affects Beliefs about Education by Kathrine M. Conn, Virginia S. Lovison, and Cecilia Hyunjung Mo (Education Next)

TFA volunteers acquire a greater appreciation for societal inequality in educational under-attainment, reduces support for charter schools and vouchers, and raises optimism that an excellent education in the US is possible for all children. [Link]

Labor Markets

The Divergent Signals about Labor Market Slack by Troy Gilchrist & Bart Hobijn (FRBSF Economic Letter)

Using a broader snapshot of the labor market shows that on balance the U3 unemployment rate is roughly representative of where things currently stand…with the important caveat that dispersion across indicators is much higher than historically has been the case. [Link]

Restaurants, Supermarkets Can’t Find Enough Workers to Open New Locations by Jaewon Kang & Heather Haddon (WSJ)

Grocers and restaurants that rely on large pools of low-prerequisite labor are struggling to find enough workers to staff new locations. [Link; paywall]

Price Tags

Why dirt from Mars could be the most expensive substance known to mankind (Science Insider/Twitter)

Three different joint space missions are hoping to bring back a couple of pounds of soil from Mars at a price tag of more than $9bn, making it easily the most expensive way to grow tomatoes ever devised (note: that’s not what scientists will use it for). [Link]

Building a Home in the U.S. Has Never Been More Expensive by Marcy Nicholson, Dave Merrill, & Cedric Sam (Bloomberg)

A fascinating walk-through of how much prices have risen for key inputs to home construction. Lumber features prominently but many other costs have also soared. [Link; soft paywall]

Disease

Covid-19 Prevention Measures Are Keeping Childhood Diseases Like Chickenpox at Bay by Peter Landers & Miho Inada (WSJ)

While COVID and related responses have had lots of negative impacts on children, there are some positives: more handwashing, masks, and other non-pharmaceutical interventions have led to a collapse in case counts for diseases like flu, chicken pox, strep throat, and rotavirus. [Link; paywall]

Moderna to take mRNA flu and HIV vaccines into Phase 1 trials this year by Rachel Arthur (BioPharma)

The company behind one of the two mRNA vaccines that were first to market in the fight against COVID is starting Phase 1 trials for flu and HIV this year, with another vaccine against cytomegalovirus (which causes mononucleosis). [Link]

Matters of State

Shrinking California by Will Wilkinson (Substack)

In 2020 California’s population shrank by over 180,000 people, with an interesting array of implications for both that state’s politics and states where former residents of the Bear Flag Republic are heading to. [Link]

West Virginia Gov. Jim Justice Is Personally Liable for $700 Million in Greensill Loans by Julie Steinberg & Duncan Mavin (WSJ)

Companies owned by West Virginia’s two-term governor are on the hook for hundreds of millions in loans backed by coal receivables, and the financial liability may roll all the way up to the governor’s mansion. [Link; paywall]

Cheating

Inside The ‘World’s Largest’ Video Game Cheating Empire by Lorenzo Franceschi-Bicchierai (Vice)

A group that found exploits to Tencent’s Playerunkown Battlegrounds Mobile and sold them for millions ended up attracting the attention of Chinese police. [Link]

Read Bespoke’s most actionable market research by joining Bespoke Premium today! Get started here.

Have a great weekend!