B.I.G. Tips – Low Volume Gains

Chart of the Day: The Montana Curve

Opposite Day For Retail Triple Plays

There were two earnings Triple Plays in the past 24 hours, with both coming out of the retail industry. A triple play is when a company reports better than expected earnings and revenues and also raises guidance. On Tuesday after the close, Nordstrom (JWN) reported EPS 19 cents above estimates and revenues of $3.657 billion compared to estimates of $3.329 billion. In spite of those strong results, the stock is not only down but it has also erased all of the gains of the past week dropping 16.5% as of this writing in today’s session. The leaves the stock right around its lows from the end of last month which are also at a similar level to the consolidation that took place at the end of last year.

Meanwhile, another retailer, Dick’s Sporting Goods (DKS), is seeing the opposite reaction. The stock is up 15% today after reporting EPS of $5.08 ($2.82 expected) and sales that were $440 million above forecasts. While both companies reported triple plays, those inverse reactions are also resemblant of the longer-term trends in the stocks heading into the reports. Since the start of the year, JWN has been making a series of lower lows and lower highs while DKS has been in a steady uptrend.

As for where the reactions stand relative to each stock’s respective history, JWN is on pace for its worst one-day reaction to any quarter since at least 2001 surpassing the 15% drop from its report in November 2015.

The stock price reaction for DKS is not at a record, but it is historic in its own right. The move today is similar to that of last August when it surged 15.68% on earnings, although that quarter didn’t qualify as a triple play since the company didn’t raise guidance. As such, the stock is on pace for its sixth (or fifth if it closes more than 15.68% higher) largest earnings move on record.

Adding to the irony of today’s reactions, historically Q2 has actually been the strongest quarter for stock price reactions to earnings for Nordstrom. On average, the stock has historically risen 2.26% the day after reporting Q2 results with a positive return 68.4% of the time.

Turning to the retail sector more broadly, the SPDR S&P Retail ETF (XRT) is higher by 15 bps today as the ETF hovers at the high end of the past several month’s range. Given it is an equal-weight ETF, the inverse and volatile moves in JWN and DKS are essentially canceling one another out. Click here to view Bespoke’s premium membership options.

Bespoke’s Morning Lineup – 8/25/21 – Big Test for Small Caps

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I have always believed that it’s important to show a new look periodically. Predictability can lead to failure.” – T. Boone Pickens

You can’t get much flatter than where equity futures are at the given moment, but then again, you can’t get a more quiet time of year than a Wednesday in late August. In COVID related news, China has reportedly started to re-open its Ningbo port after a two-week shutdown, Japan is set to spend an additional 1.4 trillion yen on additional COVID vaccines with two-thirds of the directed towards the purchase of boosters, while JNJ announced that an early study shows a boost in the body’s immune response to a booster of its COVID vaccine.

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including the latest US and international COVID trends.

It’s been quite a wild ride for small caps over the last few days. After failing to retake its 50-day moving average (DMA) in early August, bulls gave up in the middle of the month, and the Russell 2000 experienced a quick sell-off that not only tested the lows from mid-July but also broke below the 200-DMA for the first time in nearly a year. The break of the 200-DMA didn’t last long, though. Last Friday, the Russell 2000 bounced 1.6%, and that was followed by a 1.9% follow-through on Monday and then another 1% rally on Tuesday.

In the span of just three trading days, the Russell 2000 went from testing the 10% threshold for a technical correction to the point now where it is actually in the upper half (barely) of the trading range it has been stuck in nearly all year. Despite that bounce, though, the Russell heads into today still just below its 50-DMA. With it already rallying 1% in each of the last three trading days, does it still have gas left in the tank to get back above that level? That will be the big short-term test.

Start a two-week trial to Bespoke Premium and read today’s full Morning Lineup.

Start a two-week trial to Bespoke Premium and read today’s full Morning Lineup.

Daily Sector Snapshot — 8/24/21

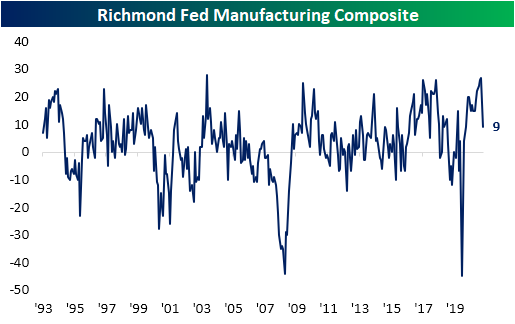

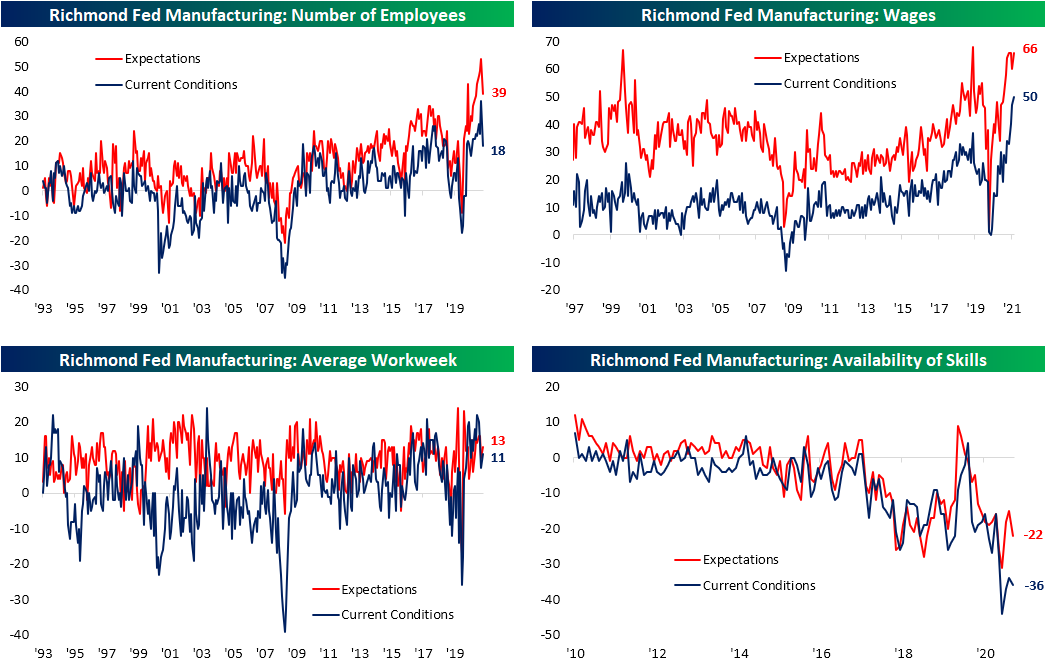

Richmond Adds to Regional Manufacturing Pain

Last week’s releases of the Philly and New York Fed manufacturing surveys showed broad slowdowns in activity, and today’s release of the Richmond Fed’s reading only reaffirmed those findings. The headline number went from a near-record high of 27 in July down 18 points to 9 in August. That is the lowest reading since last July. While that still indicates the region’s manufacturing economy is continuing to grow at a historically healthy clip, the massive decline month over month points to a historic slowdown. In fact, the 18 point decline was the third largest one-month drop on record behind 22 and 49 point declines in February and April of last year, respectively.

Given the headline number dropped by such a large degree, many of the sub-indices of the report similarly saw declines that rank in the bottom few percentiles of each one’s respective history of month over month changes. Just like the composite reading, if there is a silver lining to be had, most indices are again coming off of near-record levels meaning those large declines only leave them in the middle of their historical ranges at worst as is the case for New Orders and Shipments. Additionally, current readings mostly remain positive indicating that there is still growth across components, but at a more modest pace. The only negative indices are Local Business Conditions, the two indices covering inventories, and Availability of Skills. While some good can be reasoned with negative readings in inventories and availability of skills—for instance, those negative readings can mean firms will need to increase production with strong demand and there is a tight labor market—the drop in local business conditions is more concerning and likely a result of rising COVID cases.

As previously noted, the indices for New Orders and Shipments remain at solid levels consistent with growth in spite of the massive declines month over month. As such, Order Backlogs remain fairly elevated in the 88th percentile. While the growth of backlogs slowed dramatically alongside new orders, supply chains continue to look abnormal. Even though the index for Vendor Lead Times has fallen four points from the record high set back in May, the current reading remains well above any historical precedent.

Given lead times are long and backlogs are still elevated, inventories are also historically low. That is the case for both raw and finished goods. Each of these indices remains negative in the bottom 1% of all readings, but they did see sizable bounces in August. In other words, the region’s firms continue to report that they are drawing upon inventories at a historic rate while vendor lead times are likely not allowing those inventories to be replenished at a more desirable rate.

Prices paid finally got some relief, albeit it was not much. Prices paid rose at a 11.05% annualized pace versus a record high of 11.16% in July. Conversely, Prices Received continue to make parabolic moves rising 9.25% annualized.

Not only are prices paid and received near/at record highs, but wages also set the record bar even high. While wages are rising, actual hiring saw a substantial pullback from a record high as more firms reported a lack of workers with necessary skills. Click here to view Bespoke’s premium membership options.

Nasdaq Crosses Another 1,000 Point Threshold

It won’t be official until the close, but with the Nasdaq crossing 15,000 for the first time today, it’s on pace to cross its third 1,000 point threshold this year and the sixth since the pandemic began in early 2020. The table below lists each 1,000 point threshold that the Nasdaq has crossed over time along with the first day that it crossed that threshold, the number of days since the prior cross, what percentage that 1,000 point consists of relative to the prior threshold, and then how many upside and downside crosses the Nasdaq has had around that level on a closing basis.

Of all the 1,000 point thresholds the Nasdaq has crossed over time, the only one that it never traded back below after crossing it was 6,000 back in April 2017. Besides 1,000, that was also the 1,000 point threshold that took the longest to cross above. After first crossing 5,000 back in March 2000, it took 6,256 days for the Nasdaq to top 6,000. Since then, though, the Nasdaq has been making quick work of 1,000 point thresholds. With the exception of the 486-day gap between 8K and 9K, every other 1,000-point threshold since 6,000 has taken less than a year to cross. Even in the midst of a global pandemic, it took the Nasdaq less than six months to get from 9,000 to 10,000.

The long-term chart of the Nasdaq below includes red dots to show each time the Nasdaq first crossed a 1,000 point threshold along with the number of days for each one.

Looking at the chart above may give you a feeling of lightheadedness given the seemingly parabolic nature of the last few years. An important thing to keep in mind, though, is that as a percentage of the index’s price level, every 1,000 point threshold represents a smaller move in percentage terms. While the move from 9K to 10K represented a move of over 11%, the move from 14K to 15K represents only a little more than 7%. Looking at this chart on a log scale where each label on the y-axis represents a doubling of the index shows how modest the recent 1,000 point thresholds have been relative to earlier ones. Think about it this way, in the less than two years between when the Nasdaq first crossed 2K to when it crossed 5K for the first time (four different 1,000 point thresholds), it rallied 150%. Over the last four years, though, the Nasdaq has crossed 10 different 1,000-point thresholds, but the gain has also only been 150%. Click here to view Bespoke’s premium membership options.

Chart of the Day: Crude Oil Breaks a Losing Streak With Authority

Bespoke’s Morning Lineup – 8/24/21 – Drifting Lower

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“They always say time changes things, but you actually have to change them yourself.“ – Andy Warhol

US equities are still indicated to open higher today, but futures are off their overnight highs. Following a strong session in Asia, European markets opened higher but have been trending lower since the open. The only economic reports on the calendar today are the Richmond Fed and New Home Sales which will both be released at 10 AM.

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including the latest US and international COVID trends.

The S&P 500 came close but finished just shy of closing at a record high yesterday. The Nasdaq, meanwhile, managed to close at its 28th record high of the year. At the current pace so far this year, the Nasdaq would finish the year with 43 record closing highs. So, where would that rank relative to history? Dating back to 1971, there have actually been nine other years where the Nasdaq finished the year with 43 or more record closing highs. The most recent was last year when there were 55 and before that, you only have to go back to 2017 when there were a record 72. That’s one every three to four days!

Start a two-week trial to Bespoke Premium and read today’s full Morning Lineup.

Start a two-week trial to Bespoke Premium and read today’s full Morning Lineup.