Singles Miss Out on Housing Strength

Data on residential housing this morning surprised to the upside at the headline level in terms of both Building Permits and Housing Starts. Despite the better than expected results, the internals of the report weren’t great as all of the strength was in multi-family units. In fact, single-family Building Permits were only up 0.6% m/m and were down -0.1% y/y compared to a m/m gain of 15.8% and a y/y gain of 44.3% in multi-family permits. Similarly, single-family Housing Starts actually declined 2.8% m/m and only increased 5.2% y/y compared to multi-family units which rose 20.6% m/m and 52.7% y/y. An increase in multi-family units isn’t necessarily considered a bad thing, but single-family units tend to have more of an economic impact.

Overall, Housing Starts are still trending higher. On a 12-month moving average basis, Housing Starts have been surging in recent months and just came in at the highest level since May 2007. Housing data tends to roll over well in advance of recessions, so as long as Starts keep trending higher, it’s a sign of economic strength.

Looking more closely at single-family Building Permits and Housing Starts, the 12-month moving average of this metric has actually been starting to flatten out in recent months. Housing has been a pillar of the economy in the post-pandemic rebound, so this will bear watching going forward.

It’s always interesting to see how closely homebuilder stocks tend to track trends in Housing Starts, which we show below. Similar to the stall out in starts, we’ve also seen the iShares Home Construction ETF (ITB) start to stall out over the last few months. Click here to view Bespoke’s premium membership options.

Bespoke Stock Scores — 9/21/21

Dreamforce Kicks Off

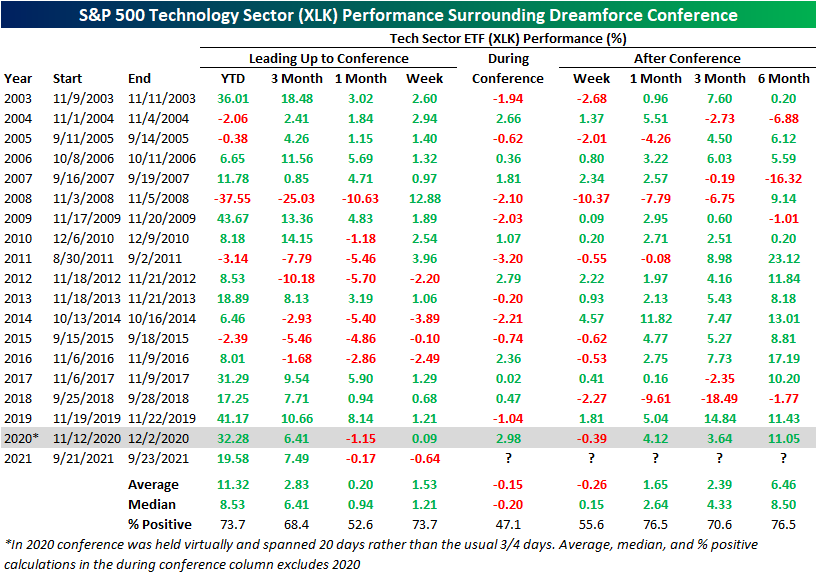

Salesforce.com (CRM) kicks off its annual Dreamforce conference today. This is the 19th year of the event in which the company showcases its products and hosts various presentations by industry leaders. Like many conferences, in-person attendance is limited again this year with the event streamed online over the next few days. Unlike last year, the conference is back to its usual length of only a few days compared to the 2020 event that went on for nearly a month. The Dreamforce conference typically occurs in the fall but has happened as early as the end of August and as late as early December.

As for how Dreamforce impacts the stock, below we show how CRM’s performance leading up to, during, and after each year’s conference. The stock pretty consistently trades higher around the Dreamforce conference. If you exclude last year when the conference lasted for a much longer period of time, and the Slack takeover acted as a negative catalyst, CRM tends to move higher during the conference. The only notable period of weakness is the week after the conference ends. That period has averaged a 0.93% decline with positive performance less than half the time. Longer-term performance, though, has been more consistent to the upside. Note that because of the extended length of Dreamforce in 2020, performance figures at the bottom of both tables do not take 2020 performance figures into account.

Salesforce.com is a giant in the Tech sector ranking as the eighth largest stock in the S&P 500 Technology sector. As such, the stock’s performance does hold some weight on the broader market. Below we replicate the table above but with the performance of the S&P 500 Tech Sector ETF (XLK). As with CRM, XLK has typically rallied leading up to the conference, but it tends to underperform CRM during the conference falling 20 bps on a median basis during the few days the event takes place versus CRM’s median gain of 0.51%. Following the conference, like CRM, XLK’s short-term performance over the next week is mixed to negative, but one, three, and six months later the stock has traded higher more than two-thirds of the time.Click here to view Bespoke’s premium membership options.

B.I.G. Tips – No Signs Of Credit Pain In Bank CDS

Chart of the Day – Over-what?

Bespoke’s Morning Lineup – 9/21/21 – Attempting a Turnaround

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“You can’t predict, [but] you can prepare.” – Howard Marks

Markets are attempting to stage a turnaround Tuesday this morning with equity futures firmly in the green and Europe also trading firmly higher. Just release economic data has provided a boost as both Building Permits and Housing Starts for the month of August came in significantly better than expected, although the strength was attributable to multi-family rather than single-family units.

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including the latest US and international COVID trends.

After a rough options expiration week, this week didn’t start any better as the S&P 500 fell 1.7% yesterday. So how common is it for the S&P 500 to trade down more than 1% on the Monday following options expiration? Since the start of 2010, there have been eighteen other occurrences, and yesterday was the second time this year and the seventh time since the COVID outbreak in 2020; so they are occurring with a bit more frequency lately. That being said, a year before COVID it happened three months in a row spanning November 2018 through January 2019. Also, like 2020, there were five occurrences in 2011.

Start a two-week trial to Bespoke Premium and read today’s full Morning Lineup.

Daily Sector Snapshot — 9/20/21

Homebuilder Sentiment Surprise

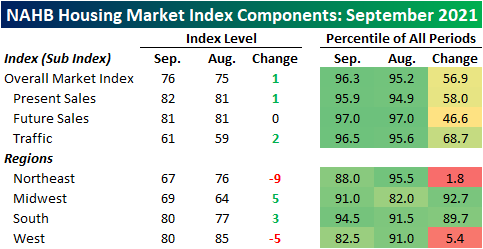

The NAHB released its September reading on homebuilder sentiment this morning. Rather than another decline down to 74 that was expected, the headline reading surprised to the upside coming in slightly higher at 76. We are now approaching the one-year anniversary since homebuilder sentiment peaked at its record high of 90 from last November. While little progress has been made in working back up to that high, the current reading remains at one of the strongest levels on record.

Both Present Sales and Traffic drove the headline index higher this month with the latter seeing the larger move higher of the two. Future sales, on the other hand, went unchanged for the second month in a row. Just like the overall market index, each of these components has pulled back from last November’s highs but remain at historically strong levels.

There was a more significant movement based on geography. Starting with the bad news, the Northeast and West experienced particularly large declines of 9 and 5 points, respectively. After that decline, sentiment in the Northeast is at the weakest reading since June of last year and the month-over-month decline ranks in the bottom 2% of all monthly moves. The drop in sentiment in the West similarly was one of the largest declines on record.

Meanwhile, the Midwest and South had much stronger showings this month. Not only were the indices for both of these regions in the top decile of all periods, but they also showed significant improvement in September. The 5 point uptick in the Midwest index ranks in the top decile of all moves while the 3 point increase in the South narrowly missed a 90th percentile move. Click here to view Bespoke’s premium membership options.

Chart of the Day: Down Mondays

Bespoke’s Morning Lineup – 9/20/21 – When it Rains, it Pours

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Failing to raise the debt limit would produce widespread economic catastrophe.” – Janet Yellen

Good Morning Subscriber,

After months of heat, it only seems fitting that problems are boiling to the surface just as Summer winds to a close this week. Between FOMC tapering, slower economic data, the upcoming debt limit, and China’s Evergrande, the problems are starting to mount. Futures opened lower last night, and originally the damage didn’t look like it was going to be too bad, but by 11 o’clock eastern time, things started to deteriorate.

The continuing collapse of Evergrande is obviously the main concern of investors around the world this morning. The fact that most of those Asian markets are closed for holidays today also makes it harder to discern what the overall impact is going to be and that only creates more uncertainty in other markets around the world that are open for trading today.

S&P 500 futures are near their lows of the morning and indicated to open down by over 1.5%, the 10-year yield is down nearly six basis points to 1.30% (it was actually lower than that last Wednesday), and the VIX is back above 25 and at its highest level since May.

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including the latest US and international COVID trends.

The numbers below are going to look worse in a couple of hours after the US market’s open, but the table below breaks down where sectors stand after last week and heading into this morning’s decline. Last week, both Materials and Utilities were easily the worst performers with declines of 3% or more. As a result of those losses, the Materials sector moved into oversold territory, while Utilities isn’t far behind. Industrials were down by only about half that much, but that was enough to put it into ‘Extreme’ oversold levels. Along with those three sectors, the only others that were below their 50-day moving averages (DMA) as of Friday were Consumer Staples and Communication Services. While only five sectors were below their 50-DMA as of Friday, there’s a good chance that by the end of the day today, either all or all but one of them (Consumer Discretionary) will be below their 50-DMAs. Change has a way of coming quickly in the market.

Start a two-week trial to Bespoke Premium and read today’s full Morning Lineup.