Chart of the Day – Economic Indicator Diffusion Index Rebounds

Bespoke’s Morning Lineup – 9/27/21 – All Eyes on Washington

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The uncreative mind can spot wrong answers, but it takes a very creative mind to spot wrong questions.“ – Antony Jay

Equities were looking higher to start the week, but that’s not the case anymore as Dow futures are now flat, the S&P 500 is indicated lower by about 0.30% while the Nasdaq is looking at a decline of nearly 1%. Small caps, meanwhile, are indicated slightly higher for now.

Washington will be a key area of focus this week as lawmakers attempt to hammer out an infrastructure bill and an agreement to keep the government funded and raise the debt ceiling. Whatever the outcome of all these negotiations, one thing we can count on is that it will not be smooth.

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including the latest US and international COVID trends.

September and October are notoriously volatile times of the year, so it shouldn’t come as a surprise that the equity market’s historical short-term performance to close out September and start October has been weak. Over the last ten years, the S&P 500’s median performance in the week following the close on 9/27 has been a decline of 0.20% which ranks in the 24th percentile relative to all other one-week periods throughout the year. While short-term performance has been on the weak side, returns one and three months out have been considerably better. Over the last ten years, the S&P 500’s median one-month performance from the close on 9/27 has been a gain of 2.41% which ranks in the 84th percentile. Performance over the following three months has been even more impressive as the S&P 500 has seen a median gain of 6.82% ranking in the 99th percentile. You can’t get much better than that.

Start a two-week trial to Bespoke Premium and read today’s full Morning Lineup.

Bespoke Brunch Reads: 9/26/21

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, join Bespoke Premium with a 30-day free trial!

Sports & Crypto

Sports Fans Are Into Cryptocurrency, and Brands Are Capitalizing by Alex Silverman (Morning Consult)

A new survey of Americans suggests that sports fans are much more likely to be familiar with cryptocurrency and other digital assets than the population as a whole, suggesting a valuable vein of marketing potential. [Link]

Golfer Tiger Woods joins NFT craze, releases 10,000 digital images to be sold through company co-founded by Tom Brady by Tom VanHaaren (ESPN)

Tiger Woods will attempt to monetize his career accomplishments via Tom Brady’s company Autograph. The NFTs are available via the DraftKings marketplace. [Link]

Regulation

Treasury unleashes cryptocurrency sanctions to fight ransomware by Sam Sabin and Victoria Guida (Politico)

This week Treasury announced stepped-up enforcement against crypto exchanges and cryptocurrencies that are used in ransomware attacks. An initial round of sanctions targeted Russian crypto exchange Suex. [Link]

Justice Department Files Antitrust Suit Challenging American-JetBlue Alliance by Brent Kendall and Alison Sider (WSJ)

An agreement between American and JetBlue to limit head-to-head competition in hub airports throughout the Northeast is being investigated by the Department of Justice on anti-trust grounds. [Link; paywall]

COVID

Pregnant Women Who Get COVID Vaccine Pass Antibodies to Newborns (HealthDay News)

An NYU study showed that all 36 newborns tested at birth for COVID-19 antibodies from their vaccinated mothers had immune systems primed for the virus, a major endorsement of vaccination for pregnant women. [Link]

‘Post-Vax COVID’ Is a New Disease by Katherine J. Wu (The Atlantic)

Some diseases that we already vaccinate against continue to infect vaccinated people, but in a modified, much less dangerous form. COVID is likely to move the same direction over time, remaining a burden on vaccinated people but ultimately a much less deadly one. [Link]

Renewables Finance

EXCLUSIVE White House backs plan for renewable energy industry tax partnerships by Jarrett Renshaw and Laura Sanicola (Reuters)

Carbon-intensive energy infrastructure is often owned by master limited partnerships, which confer significant tax advantages. The Biden administration is reportedly considering the creation of a similar set of vehicles for renewables energy production and distribution. [Link]

Europe’s Big Climate Reveal Gets Stuck on Sovereign Bonds by Frances Schwartzkopff and John Ainger (Bloomberg)

The EU is requiring disclosure from asset managers on how much of their portfolios are invested in environmentally sustainable activities. But government bonds aren’t included in the disclosure requirements, leading to a strange grey area for the largest chunk of the European bond markets. [Link; soft paywall]

A huge new city is being built in the US desert – but is it just greenwashing? by Ed Cunningham (TimeOut)

A billionaire’s plan to create a city of 5 million in the arid western United States is either a stroke of genius or a vanity project run horrifically amuck. [Link]

Natural Disasters

The Long-Lost Tale of an 18th-Century Tsunami, as Told by Trees by Max G. Levy (Wired)

A 9.0 magnitude quake before the arrival of Captain Cook in the Pacific Northwest recked havoc on the region, leaving a massive impact on the growth of Douglas Firs which still stand today. [Link; soft paywall]

Economic Research

Why Do We Think That Inflation Expectations Matter for Inflation? (And Should We?) by Jeremy B. Rudd (Federal Reserve Finance and Economics Discussion Series)

A scathing review of the widespread presumption that inflation expectations are a key source of future inflation, raising the possibility of significant policy errors. [Link; 27 page PDF]

E-Commerce

FedEx, UPS Rate Rises Are Making Online Shopping More Expensive by Paul Ziobro (WSJ)

Large shipping companies are raising prices in coming weeks with FedEx announcing a 6% cost hike; UPS and FedEx typically raise prices at about 5% per year. [Link; paywall]

Read Bespoke’s most actionable market research by joining Bespoke Premium today! Get started here.

Have a great weekend!

The Bespoke Report Newsletter – 9/24/21 – Turning Points In Markets, The Economy, And Policy

This week’s Bespoke Report newsletter is now available for members.

Whether you look at the earnings outlook, macroeconomic data, or the policy backdrop, we’ve reached a turning point in the trends that have defined the recovery from the COVID recession. We discuss all in detail in the latest edition of The Bespoke Report along with analysis of inflation and the ten year yield, cryptocurrencies, an update on our Death By Amazon and Amazon Survivors indices, events in China this week, housing market data this week, analysis of the Federal Reserves Q2 Flow of Funds report, and more.

To read this week’s full Bespoke Report newsletter and access everything else Bespoke’s research platform has to offer, start a two-week trial to one of our three membership levels.

Daily Sector Snapshot — 9/24/21

Bespoke’s Morning Lineup – 9/24/21 – A Rally Sandwich

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Indecision may or may not be my problem.” – Jimmy Buffett

After a couple of good days where it appeared as though the market was putting some of the September headwinds behind it, it looks as though equities will close out the week on a down note causing a rally sandwich on a loaf of weakness. If the S&P 500 closes at current levels indicated by the futures market, we’ll finish down for the week and back below the 50-DMA. The Russell 2000, however, is still on pace for a positive week provided current levels hold. Thursday’s rally back above the 50-DMA for the S&P 500 was a moral victory for technicians, but if it doesn’t hold today, it will mark the second straight week that the index closed below its 50-DMA.

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including the latest US and international COVID trends.

As for where the major averages stand heading into today, the Russell 2000’s sideways consolidation range remains intact and barring further weakness during the trading session, its 50-day moving average should continue to hold. The Nasdaq 100 and S&P 500 are another story, though, as both of these indices are on pace to open below those levels today. Technicians consider failed attempts to retake the 50-DMA to be a sign of underlying weakness, so that will be a trend to watch going forward.

Start a two-week trial to Bespoke Premium and read today’s full Morning Lineup.

Bespoke’s Weekly Sector Snapshot — 9/23/21

The Bespoke 50 Top Growth Stocks – 9/23/21

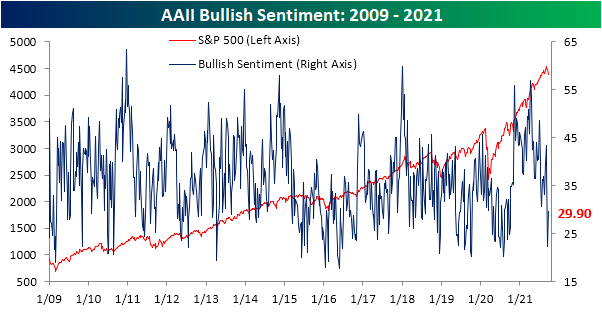

Individual Investor Sentiment Bounces Back

Last week saw a massive decline in optimism according to the AAII‘s weekly investor sentiment survey. In fact, bullish sentiment saw its largest one-week decline in over two years. Even though the S&P 500 has technically declined more in the week leading up to this week’s survey than last week’s, sentiment actually improved with the percentage of respondents reporting as bullish rising from 22.4% to 29.9%. That was the biggest one-week increase since the first week of July, but the percentage of bullish respondents is still well below the past year’s range.

Even though there was a big pickup in bullish sentiment, bearish sentiment was only little changed. This reading only fell 0.1 percentage points to 39.3%. That remains at a level above anything observed since last fall.

That means that mostly all of the gains to bullish sentiment this week borrowed heavily from the neutral camp. Neutral sentiment fell sharply this week shedding 7.4 percentage points. That was the biggest one-week decline since a 7.5 percentage point drop in the first week of August.

We’d also note that while last week saw a big shift in sentiment among individual investors, this week, newsletter writers followed suit as bullish sentiment among that group fell below 50% to 47.1% for the lowest reading since May. Bearish sentiment meanwhile rose to 22.3% which is the highest reading since October 7th of last year. Click here to view Bespoke’s premium membership options.