Bespoke Baskets Update — January 2022

Daily Sector Snapshot — 1/19/22

S&P 500 Sector Weightings Report – Q1 2022

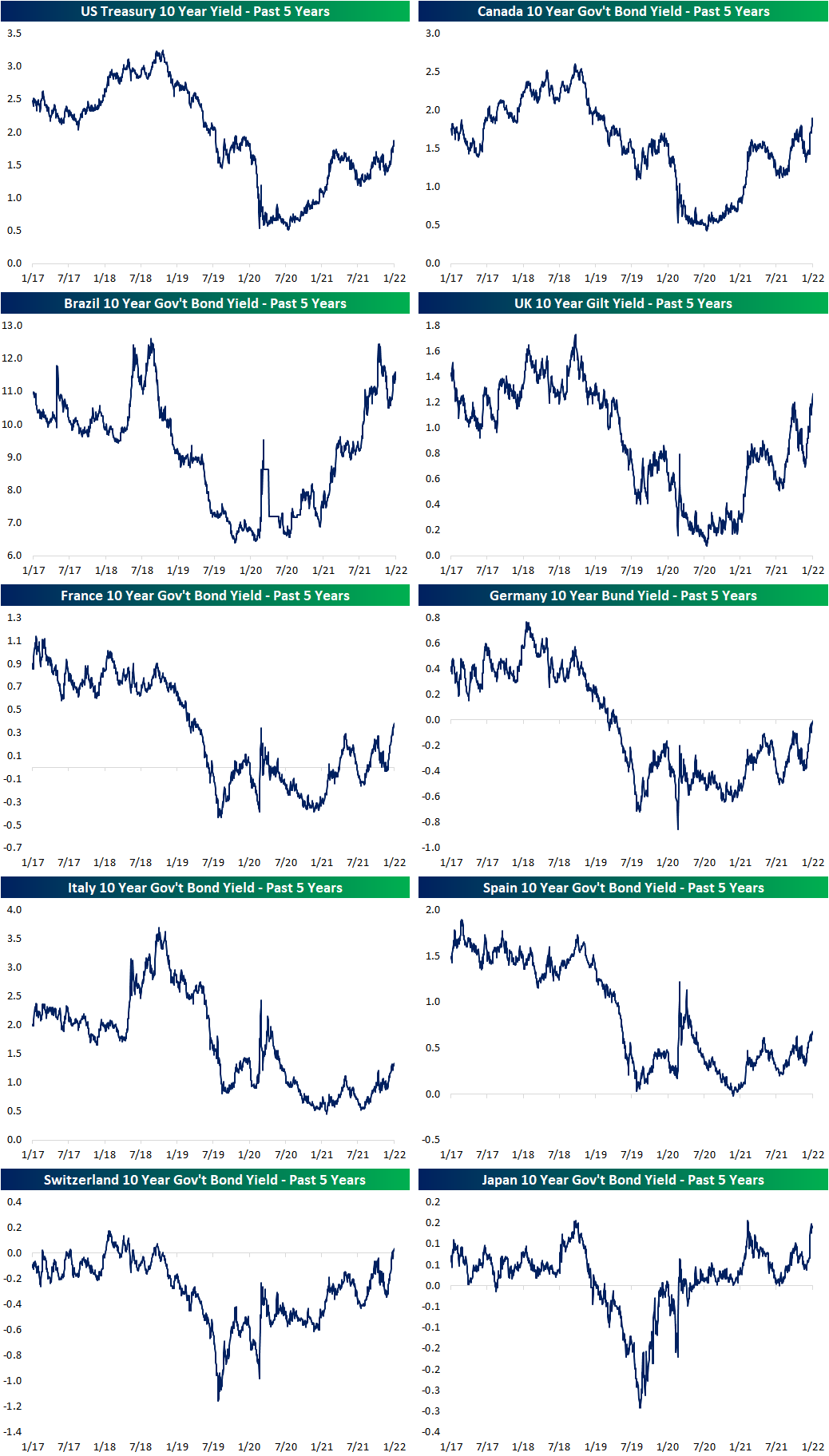

Sovereigns Soar

All around the world, government bond yields are on the rise and hitting some significant levels. In many cases, the rapid increase in yields over the past month has resulted in multi-month, if not multi-year, highs. For Spain and Italy, today’s level of yields are the highest since May and June 2020, respectively. The 10 year US Treasury yield has reached the highest level since January 2020 as Canada, France, the UK, and Germany meanwhile have the highest yields since the spring of 2019. In the case of Germany, the bund yield even moved back into positive territory for the first time since 2019. As the 10-year yield on Swiss bonds has reached the highest level since the fall of 2018, it too has moved back into positive territory in recent weeks. While it has also seen a big rise in yields, Brazilian bond yields remain further off of prior highs.

As previously mentioned, the broad move in yields in the past month has been rapid. In the charts below, we show the one-month change in the 10-year yields for these countries’ bonds going back over the past five years. In most cases, the current run has been the sharpest increase since around the time of the COVID crash. For each country shown, those one-month changes also rank in the top few percent of all monthly changes over the past two decades. In fact, for Canadian bonds and UK Gilts, the moves rank in the top 1% of all monthly moves over the past twenty years. In today’s Fixed Income Weekly, we take a closer look at the moves in yields for a range of countries, and the implications for foreign exchange. Click here to view Bespoke’s premium membership options.

B.I.G. Tips – Small Cap Death Cross

Bespoke’s Morning Lineup – 1/19/22 – Strong Housing Data

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“A good first impression can work wonders.” – J.K. Rowling

Futures are attempting a bounce after yesterday’s wallop, and positive reactions to earnings from Bank of America (BAC) and Morgan Stanley are contributing to the positive tone. The only economic reports for the morning were Housing Starts and Building Permits, and both came in significantly higher than expected and at their second-highest levels since the financial crisis. The only readings that were strong for each series were in Q1 of 2021.

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including the latest US and international COVID trends.

First impressions are always important, but they’re not always accurate, and that’s the hope of bulls following the first days of earnings season. Banks kicked off the Q4 earnings season late last week, and two of the largest to report were Goldman Sachs (GS) and JP Morgan Chase (JPM). The stocks of both banks had abysmal reactions to their reports.

Following Friday’s report from JPM, the stock declined 6.15% which ranks as the worst earnings reaction day performance for the stock in at least 20 years beating out the 6.06% decline the stock experienced in January 2009 during the thick of the financial crisis. The reaction in GS to its earnings report on Tuesday wasn’t much better with the stock falling just under 7%. That was large enough to rank as the second-worst earnings day reaction for the stock behind only the 11.56% decline in April 2009 just as markets were coming out of the financial crisis.

As disheartening as a bad first impression can be, one potential bright side is that it can have the effect of resetting the bar low, and in early trading, both Bank of America (BAC) and Morgan Stanley (MS) are trading up close to 3% in reaction to their reports. Whether those gains can hold through the opening and closing bell, though, is another story.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Chart of the Day – Mid-Term Election Years

Bespoke Stock Scores — 1/18/22

Daily Sector Snapshot — 1/18/22

Energy Exploding (Relatively Speaking)

To help get a gauge on which sectors are out- or underperforming the broader market, in the charts below, we show the relative strength lines of each of the eleven sectors versus the S&P 500 over the past year from our Sector Snapshot. Market trends in the prior days and weeks have resulted in some notable moves across these relative strength lines.

With Consumer Discretionary one of the weaker sectors of late as high growth areas have gotten hit hardest, its relative strength line has broken below its most recent low. While Consumer Discretionary has broken down on a relative basis, Communication Services, which has seen a massive string of underperformance since the summer, has seen a modest reversal higher, although the steep downtrend of the relative strength line is still in place.

The Tech sector has also seen a breakdown in its relative strength line recently with a collapse in the past month. Conversely, Real Estate has held onto its uptrend with its relative strength line bouncing over the past couple of days.

Consumer Staples, Financials, and Industrials, meanwhile, have been in downtrends over most of the past year. The recent strength of Staples and Industrials have broken those downtrends materially while Financials have failed to break out in the past several days after a big leg higher in the preceding weeks. Utilities similarly has failed to move out of its downtrend. At that same time, Energy has essentially made a vertical move higher after what was generally a sideways move in the past year.

The last couple of years has certainly seen a strong run for the Energy sector, but taking a longer-term look at performance relative to the broader market it is hard to tell. In the chart below, we show the relative strength line of the Energy sector versus the S&P 500 starting on 7/1/08, when the ratio of the sector to the S&P 500 hit its all-time high. As shown, there has been secular underperformance from Energy stocks since the Global Financial Crisis which hit its most extreme level during the COVID crash. Since the lows in the spring of 2020, the Energy sector has rebounded, and the relative strength line is at some of the highest levels in the past couple of years, but there is still a long way to go in order to break the longer-term downtrend. Stay on top of market trends by becoming a Bespoke subscriber today. Click here to view Bespoke’s premium membership options.