Bespoke’s Morning Lineup – 1/31/22 – Only One More Day

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Success is not final; failure is not fatal: It is the courage to continue that counts.” – Winston Churchill

US equity futures are trading down towards their lows of the morning after trading higher most of the night. A key concern for the market continues to be – you guessed it – the Fed, and comments from Atlanta Fed President Raphael Bostic suggesting the possibility of a 50 basis points (bps) hike has some investors on edge. A read of his comments, though, shows that he only said ‘every option is in the table for every meeting’, and then went on to say that his views will follow incoming data rather than committing to some pre-set plan. With more than six weeks between now and the March meeting, there’s probably going to be a lot more headlines like this as investors look to decipher and dissect every comment from every Fed official for signs of where they’re leaning.

The economic calendar is on the light side today with Chicago PMI and Dallas Fed the only reports on the calendar. The Chicago report is forecast to show slower growth than December while the Dallas read on manufacturing activity is expected to come in right around December’s levels. Earnings data is also on the light side today, but that won’t last as the rest of the week will be one of the busiest of the earnings season.

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including the latest US and international COVID trends.

After the month we’ve had, there isn’t much positive to say about the equity market so far in 2022. One silver lining could be seasonality. The gauges below taken from today’s Morning Lineup show that the upcoming one and three-month periods for the S&P 500 are among the best one and three-month periods of the year. Over the last ten years, the S&P 500’s median performance from the close on 1/31 out through the next month has been a gain of 3.94% while the forward three-month return has been a gain of 5.68%. Those median performance numbers are good enough to rank in the 98th and 85th percentile, respectively, relative to all other one and three months periods of the year. Seasonal trends are only one part of the puzzle when it comes to market returns and they can easily be outweighed by other factors, but at least the market has the calendar working in its favor.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Bespoke Brunch Reads: 1/30/22

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, join Bespoke Premium with a 30-day free trial!

Biology

Frogs Regrow Missing Limbs in Lab Study, Advancing Key Effort of Regenerative Medicine by Aylin Woodward (WSJ)

A new drug cocktail is a small step forward, but a step nonetheless in the quest to regrow human limbs lost to disease or accidents. [Link; paywall]

Why we are living in an era of unnatural selection by David Farrier (BBC)

Evolution is an inexorable force framed by the environment living things inhabit. Humans have radically altered that environment and the results are as interesting as they are hard to believe. [Link]

Why The Animal Critic Gives The Panda An F (NPR)

Pandas are lazy, refuse to reproduce, and their primary source of food is one they are not able to properly digest. That compares to the noble octopus, which is highly intelligent and have strong memories. [Link]

Renewables

Bumper year-end for Chinese offshore wind as feed-in tariff expires by Nadia Weekes (WindPower Monthly)

As subsidies for wind power farms were set to end, ten different 300MW+ Chinese wind farms entered service in December, with a combined capacity off 3.5GW; China is targeting 1.2TW of total wind and solar capacity by 2030. [Link]

McKinsey calculates the staggering capital spending required to reach net-zero by 2050 by Emma Newburger (CNBC)

The cost of transitioning to net-zero GHG emissions by 2050 would need $3.5trn per year in capital spending, equivalent to 7% of household spending in 2020. [Link]

Tesla

Elon Musk offers college student $5,000 to delete Twitter bot tracking his private jet over ‘security concerns’ – but the IT major refuses and asks for internship instead by Keith Griffith (Daily Mail)

A teenager collated data from a range of public sources to create a Twitter bot that keeps the world appraised as to what Elon Musk’s private jet is up to, leading to a very amusing offer and counter-offer. [Link]

Tesla Now Runs the Most Productive Auto Factory in America by Tom Randall and Demetrios Pogkas (Bloomberg)

While the entire auto industry has suffered from the semis shortage, Tesla’s Fremont, CA factory is churning out more finished cars than any of the more than 70 national auto manufacturing facilities. [Link; soft paywall]

Growth

ARKK’s Claims of an Anti-Innovation Market Ring Hollow by Robby Greengold, CFA (MorningStar)

An investigation of ARK Invest’s claims that weak performance has been due to a market-wide attack on innovation-related stocks more generally. [Link; registration required]

Startup Funding Triples to a Record $15 Billion in Latin America by Ezraa Fieser (Bloomberg)

2021 was a benchmark year for tech startups in Latin America as investors poured more than $15bn in to the region’s new companies, more than three times the prior record. [Link; soft paywall]

We Might Be in a Simulation. How Much Should That Worry Us? by Farhad Manjoo (NYT)

If we start to see the virtual world as just as “real” as the non-virtual one, what does that say about how “real” the non-virtual world is? [Link; soft paywall]

Fugitive Crystal Cruises’ luxury ship on the lam expected to stay in Bahamas’ safe haven by Jay Weaver, David J. Neal, and Anna Jean Kaiser (Miami Herald)

A cruise ship that is owned by a bankrupt company has become a federal fugitive, with an arrest warrant issued and US Marshalls in pursuit across the Caribbean. [Link]

Mobility

The cultural dynamics of declining residential mobility by Nicolas Buttrick and Shigehiro Oishi (NIH)

Declines in mobility are linked to significant changes in culture that create feelings of cultural stagnation and even concrete material costs to people who used to be able to move but now are stuck in place. [Link]

Gambling

Parlay Cards Prove to be Worst Bet Gamblers Make in Las Vegas Casinos in 2021 by Darren Rovell (Action Network)

Casinos keep 32% of the money that punters bet on parlays, which are a uniquely terrible wager in terms of the take for bettors looking for a long shot. [Link]

Read Bespoke’s most actionable market research by joining Bespoke Premium today! Get started here.

Have a great weekend!

The Bespoke Report — Equity Market Pros and Cons — Q1 2022

This week’s Bespoke Report is an updated version of our “Pros and Cons” edition for Q1 2022.

With this report, you’re able to get a complete picture of the bull and bear case for US stocks right now. It’s heavy on graphics and light on text, but we let the charts and tables do the talking!

On page two of the report, you’ll see a full list of the pros and cons that we lay out. We then provide slides for each “pro” or “con” that we’ve highlighted.

To read this report and access everything else Bespoke’s research platform has to offer, start a two-week trial to Bespoke Premium.

Heard on Conference Calls: Q4 Earnings Season

Below are some of the most interesting quotes pulled from our Conference Call Recaps since the start of the Q4 earnings season:

Supply Chain/Inflation

- According to Apple CEO Tim Cook, the logistics environment “is very elevated in terms of the cost of moving things around. I would hope that at least a portion of that is transitory, but…the world has changed.”

- In regards to supply chain issues, Intel CEO Pat Gelsinger added, “As we predicted, these ecosystem constraints are expected to persist through 2022 and into 2023, with incremental improvements over this period.”

- Tesla CEO Elon Musk stated, “In 2022, [the] supply chain will continue to be the fundamental limiter of output across all factories. So, the chip shortage, while better than last year, is still an issue.”

- Although Johnson & Johnson reported solid results, multiple segments were negatively impacted by “raw material availability” and “supply chain constraints,” according to CFO Joseph Wolk.

- 3M CEO Mike Roman commented, “we’re going to see a volatile environment in the first half of 2022. Things should get better in the second half, but I would not expect a big snap back on stability of supply in 1Q of 2022.”

- Procter & Gamble CEO Jon Moeller pointed out that “Higher commodity and freight cost impacts combined were a 460 basis points hit to gross margins.”

- Moeller continued, “Transportation and labor markets remain tight, availability of materials remain stretched in some categories and in some markets, inflationary pressures are broad-based with little sign of near-term relief.”

COVID related

- The Netflix management team blamed “COVID overhang and macro-economic hardships in several parts of the world like LATAM” as a factor hindering growth.

- Intuitive Surgical reported that “COVID-19 has had, and will likely continue to have, an adverse impact on the company’s procedure volumes.”

- United Health CFO John Rex commented, “In the most recent weeks inpatient hospitalization levels for our members are similar to the January 2021 levels, even with national COVID case rates about 4x higher.”

Technological Development

- In terms of the metaverse, Microsoft CEO Satya Nadella commented, “And as the digital and physical worlds come together, we are seeing real enterprise metaverse usage, from smart factories to smart buildings to smart cities.”

- Nadella continued, “As every company becomes a digital company, they will need a distributed computing fabric to build, manage, secure and deploy applications anywhere.”

- American Express aims to stay at the “leading edge of technology and digital payment solutions to make American Express an essential part of our customers digital lives,” as per CEO Stephen Squeri.

- In November, Netflix unveiled its mobile gaming experience globally, which allows members to “discover and launch games from within the Netflix mobile app.”

- Tesla CEO Elon Musk believes that “over time, we think Full Self-Driving will become the most important source of profitability for Tesla”.

Broader Economy

- American Express is forecasting “higher than long-term aspirational levels of revenue growth” through 2023 due to elevated levels of consumer spending, according to the investor presentation.

- Union Pacific EVP Kenny Rocker stated that the company “will face continued challenges in our energy-related market.”

- In regards to the energy market, Baker Hughes CEO Lorenzo Simonelli added, “As we look ahead to 2022, we expect the pace of global economic growth to remain strong although slightly moderate compared to 2021. We believe the broader macro recovery should translate into rising energy demand for 2022 and relatively tight supplies for oil and natural gas.”

- Simonelli continued, “growth rates are likely to moderate from 2021 levels as central banks are expected to begin tightening monetary policy in order to reduce COVID-related stimulus plans and quell growing inflationary pressures.”

- Automatic Data Processing CFO Don McGuire commented, “a gradual ongoing recovery in labor force participation will support job growth in the first half of the year.”

- Boeing CEO David Calhoun referenced the international markets, stating, “Recovery continues broadening in Europe and South America [but] further lockdowns have stagnated recovery in China.”

In summary, management teams anticipate operating in a continued inflationary environment, but the supply chain constraints are expected to ease in the back half of 2022. Since COVID emerged, there has been an increased focus on digitization, which certain companies are attempting to capitalize on. In regards to the energy market, supply is expected to remain tight while demand strengthens, thus implying a higher price point for related commodities.

To stay up to date with Corporate America’s rhetoric, become an Institutional Subscriber today to get full access to our Conference Call Recaps. Click here to view a sample of the conference call recaps that you would be receiving on a daily basis during earnings season.

B.I.G. Tips – What Does Bearish Sentiment Imply for the S&P 500?

Bespoke’s Morning Lineup – 1/28/22 – No Support

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I’m only rich because I know when I’m wrong.” – George Soros

Markets are flipping the script this morning as the pattern of futures overnight and into this morning has been the complete opposite of the pattern Wednesday night into Thursday morning. Whereas futures traded lower most of the night Wednesday and rallied into the open, overnight futures were positive but started to aggressively sell-off after Europe opened. Geopolitical events are a major issue weighing on sentiment as President Biden reportedly told Ukrainian President Zelensky that a Russian invasion was ‘virtually certain’ even as Zelensky has asked Biden to tone down the rhetoric and ‘ calm down the messaging’.

It may be Friday, but there are some important economic data on the calendar. The Employment Cost Index, Personal Income, and Personal Spending all just hit the taps while Michigan Confidence will hit the wires at 10:00. In terms of the reports already released, the Employment Cost Index rose slightly less than expected while Personal Income saw a smaller than expected increase and Personal Spending dropped right in line with forecasts (-0.6%).

As we have noted throughout the last several trading days, futures have done a terrible job at predicting market direction lately, so there’s a good chance that by the time the closing bell rings, things will look different than they do now.

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including the latest US and international COVID trends.

The S&P 500 is currently down just over 10% from its recent record highs in what has been a relatively rapid deterioration in equity markets. In the span of just two weeks, the S&P 500 tracking ETF has given up both its 50-day and 200-day moving average (DMA), and neither level provided anything in the way of support. The next level to watch is the lows from last fall, and that level may not even hold through the end of the day.

While the 50 and 200-DMAs for SPY didn’t provide much in the way of support, on Wednesday’s first attempt to rally back above the 200-DMA, it acted as resistance. In Wednesday’s trading, the S&P 500 opened higher and briefly rallied above the 200-DMA but faded throughout the trading day. Just as the 200-DMA tends to provide support in an up-trending market, it tends to act as resistance during downtrends, so until SPY can rally back above its 200-DMA, the burden of proof is on the bulls.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

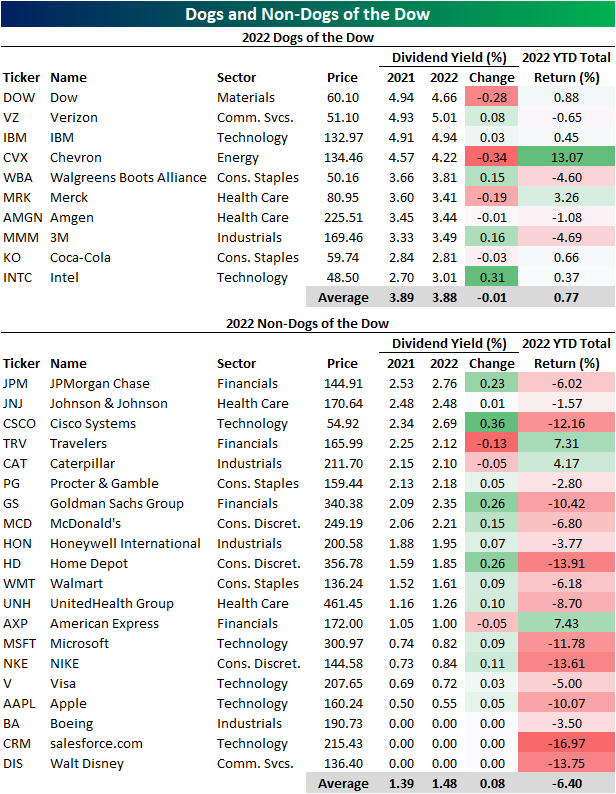

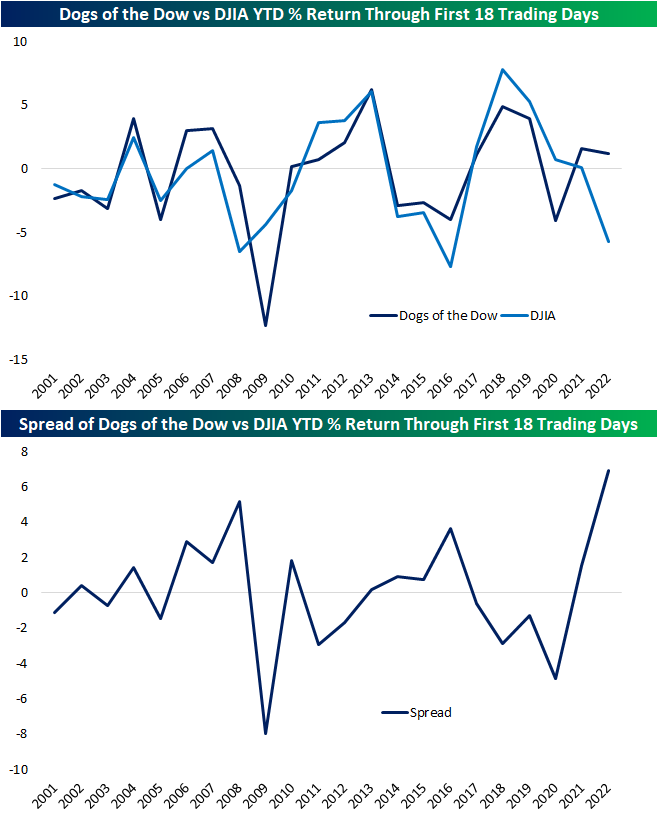

Dogs of the Dow Dominating

At the end of last year, we highlight the performance of the “Dogs of the Dow” in 2021. The Dogs of the Dow is a simple strategy that says to buy the ten highest yielding stocks in the Dow at the end of each year. In 2021, the Dogs underperformed, but so far in the new year, the complete opposite is true. As shown below, a little more than half of the Dogs are in the black year to date compared to only three (of twenty) non-dogs that are positive.

Taking a look at an index of the Dogs of the Dow going back to 2001, this year has marked the widest gap in returns between the Dogs and the broad Dow 30 through the first 18 trading days of the year. The only year that comes anywhere close to the gap in performance was 2008, and unlike this year, back then the Dogs were in the red at this point of the year. Click here to view Bespoke’s premium membership options.

B.I.G. Tips – Wild Intraday Swings Continue

Daily Sector Snapshot — 1/27/22

The Bespoke 50 Growth Stocks – 1/27/22

The “Bespoke 50” is a basket of noteworthy growth stocks in the Russell 3,000. To make the list, a stock must have strong earnings growth prospects along with an attractive price chart based on Bespoke’s analysis. The Bespoke 50 is updated weekly on Thursday unless otherwise noted. There were ten changes to the list this week.

The Bespoke 50 is available with a Bespoke Premium subscription or a Bespoke Institutional subscription. You can learn more about our subscription offerings at our Membership Options page, or simply start a two-week trial at our sign-up page.

The Bespoke 50 performance chart shown does not represent actual investment results. The Bespoke 50 is updated weekly on Thursday. Performance is based on equally weighting each of the 50 stocks (2% each) and is calculated using each stock’s opening price as of Friday morning each week. Entry prices and exit prices used for stocks that are added or removed from the Bespoke 50 are based on Friday’s opening price. Any potential commissions, brokerage fees, or dividends are not included in the Bespoke 50 performance calculation, but the performance shown is net of a hypothetical annual advisory fee of 0.85%. Performance tracking for the Bespoke 50 and the Russell 3,000 total return index begins on March 5th, 2012 when the Bespoke 50 was first published. Past performance is not a guarantee of future results. The Bespoke 50 is meant to be an idea generator for investors and not a recommendation to buy or sell any specific securities. It is not personalized advice because it in no way takes into account an investor’s individual needs. As always, investors should conduct their own research when buying or selling individual securities. Click here to read our full disclosure on hypothetical performance tracking. Bespoke representatives or wealth management clients may have positions in securities discussed or mentioned in its published content.