Daily Sector Snapshot — 2/4/22

A “Sell First, Ask Questions Later” Earnings Season

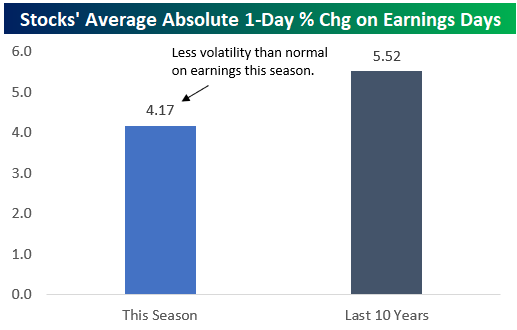

Through Thursday morning, 549 companies had reported Q4 2021 numbers since the current earnings season began the week of Jan. 10th-14th. While it may seem like stocks have been extremely volatile on their earnings reaction days this season due to a number of high-profile names seeing extreme one-day moves, on average, earnings-day volatility has actually been lower than normal. Over the last ten years, the average stock that has reported earnings has seen an absolute one-day change of +/-5.52% on its earnings reaction day. (For stocks that report before the open, its earnings reaction day is that trading day. For stocks that report after the close, its earnings reaction day is the next trading day.) So far this season, the average stock that has reported has seen an absolute one-day change of just +/-4.17%.

While earnings volatility has been lower than normal across all of the stocks that have reported this season, share-price reactions to earnings have also been much weaker than normal. Below are a number of charts showing how stocks have performed on their earnings reaction days this season versus the average over the last ten years based on a number of earnings scenarios.

As shown in the first chart below left, stocks that have beaten consensus analyst EPS estimates have risen by an average of just 0.06% on their earnings reaction day this season. Over the last ten years, the average EPS beat has gained 1.65% on its earnings reaction day. Reactions to top-line sales beats have actually been negative. As shown, stocks that have beaten sales estimates this season have averaged a one-day drop of 0.41% on their earnings reaction days versus an average gain of 1.36% for sales beats over the last ten years.

While EPS and sales beats are usually rewarded with positive share-price reactions, this season they’re not being rewarded at all, and in the case of sales, beats are actually being punished!

Interestingly, while beats have experienced much weaker than normal performance this season, misses are performing in line to better than they normally do. The average stock that has missed EPS estimates has declined 3.34% on its earnings reaction day this season, which is the exact same as the average reading for the last ten years. The average stock that has missed sales estimates has fallen 1.65% on its earnings reaction day this season, which is actually better than the 10-year average of -2.07%.

Stocks that beat both EPS and sales estimates have averaged a one-day gain of 2.36% on their earnings reaction days over the last ten years. This season, stocks that have beaten on both the top and bottom line have seen a minuscule one-day gain of just 0.15%. On the flip side, stocks that have missed both EPS and sales have averaged a one-day drop of 4.22% this season, which is slightly better than the average drop of 4.47% seen for EPS and sales misses over the last ten years.

Finally, below we look at price reactions based on forward guidance. Normally, a stock that raises guidance sees the biggest reward on earnings reaction days with a one-day average gain of 4.04% over the last ten years. This season, the average stock that has raised guidance has gained just 0.82% on its earnings reaction day. Stocks that lower guidance have historically gotten crushed with an average one-day drop of 5.3%. This season, the average stock that has lowered guidance has fallen even more with a one-day drop of 6.03%.

To conclude, investors have simply not been willing to reward companies that have posted strong results this earnings season. In a “normal” market environment where investors are focused more on fundamentals at the micro-level, we see buying in reaction to positive reports and selling in reaction to negative reports. This season, there seems to be much less of a focus on the micro and a much bigger focus on the macro, with the economy (and Corporate America) facing the key headwind of higher interest rates down the road. Of course, this type of environment also presents opportunities for investors to find stocks that may be getting unduly punished because others are looking to “sell first and ask questions later.” Bespoke publishes in-depth earnings analysis for subscribers on a daily basis throughout earnings season, including Conference Call Recaps as well as individual results and share price reactions. You can see these reports by starting a two-week trial to Bespoke Premium today.

Bespoke’s Consumer Pulse Report – February 2022

Bespoke’s Morning Lineup – 2/4/22 – Jobs Day

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Always buy your straw hats in the Winter” – Benjamin Graham

There’s a lot of ‘straw hats’ on sale in the market lately, but the question is how far they are from their ‘final markdowns’. Futures were much higher overnight, but have been drifting lower ever since Europe opened for trading. Amazon.com (AMZN) is still up over 10% following its earnings report after the close yesterday, and that’s helping to keep Nasdaq futures marginally higher this morning while the S&P 500 is flat and Dow futures are down. One asset not on the sale rack is crude oil as WTI is firmly above $90 and looks headed to triple-digits.

The big market event of the morning was the January Non-Farm Payrolls report, and after two months where economists were expecting a strong report and received much weaker than expected news, today they were expecting a weak report due to Omicron, but as luck would have it, the results came in much stronger than expected. The initial reaction in the markets was for higher rates and lower equities, so it looks like bulls may be heading into the weekend disappointed.

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including the latest US and international COVID trends.

The market couldn’t keep bouncing forever, but even after the rally off of last week’s lows, yesterday’s decline was a tough one for bulls to stomach. As shown in the chart below, while the bounce brought the S&P 500 back above the 200-DMA – a level it still trades above now – it stalled out just below the 50-DMA, and yesterday’s sell-off brought it back below the highs from late last summer. How the S&P 500 trades today following AMZN’s strong report will likely say a lot in whether yesterday’s weakness is the beginning of another leg lower.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Bespoke’s Weekly Sector Snapshot — 2/3/22

A Little Less Negative

While the S&P 500 and other major indices are being pulled lower today, the past week has generally seen them reverse some of January’s losses, and as a result, sentiment has become modestly more optimistic. The AAII sentiment survey showed bullish sentiment tip back above a quarter of respondents in the most recent week rising to 26.5%.

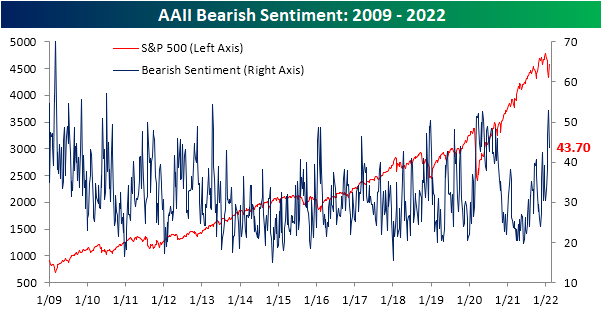

Bearish sentiment meanwhile fell back to 43.7% after hitting the highest level since April 2013 last week.

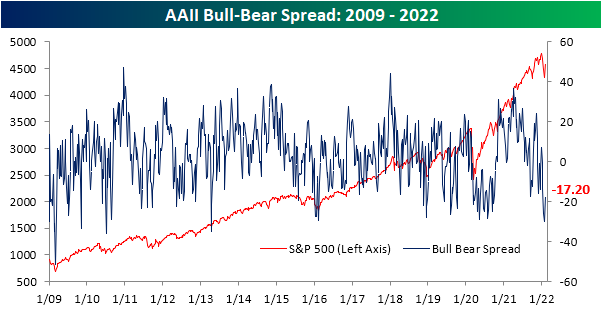

While bulls and bears both moderated in the most recent week’s survey, investor sentiment remains largely bearish. The bull-bear spread rose but remains deeply negative at -17.2. At that level, the bull-bear spread remains in the bottom 8% of all readings in the history of the survey.

While bulls did borrow from the decline in bearish sentiment, a larger share reported neutral sentiment this week. That reading rose six percentage points to 29.9% which is the biggest increase since the second week of December, but that level is still below the 30%+ readings that were common throughout the final quarter of 2021.

Other sentiment surveys like the Investor Intelligence survey of equity newsletter writers and the NAAIM Exposure Index, also saw a rebound in bullish sentiment this week which led our sentiment composite to regain some of the recent large declines. As with the AAII survey though, sentiment remains at a fairly bearish level in spite of this week’s improvements. Click here to view Bespoke’s premium membership options.

The Bespoke 50 Growth Stocks – 2/3/22

The “Bespoke 50” is a basket of noteworthy growth stocks in the Russell 3,000. To make the list, a stock must have strong earnings growth prospects along with an attractive price chart based on Bespoke’s analysis. The Bespoke 50 is updated weekly on Thursday unless otherwise noted. There was one change to the list this week.

The Bespoke 50 is available with a Bespoke Premium subscription or a Bespoke Institutional subscription. You can learn more about our subscription offerings at our Membership Options page, or simply start a two-week trial at our sign-up page.

The Bespoke 50 performance chart shown does not represent actual investment results. The Bespoke 50 is updated weekly on Thursday. Performance is based on equally weighting each of the 50 stocks (2% each) and is calculated using each stock’s opening price as of Friday morning each week. Entry prices and exit prices used for stocks that are added or removed from the Bespoke 50 are based on Friday’s opening price. Any potential commissions, brokerage fees, or dividends are not included in the Bespoke 50 performance calculation, but the performance shown is net of a hypothetical annual advisory fee of 0.85%. Performance tracking for the Bespoke 50 and the Russell 3,000 total return index begins on March 5th, 2012 when the Bespoke 50 was first published. Past performance is not a guarantee of future results. The Bespoke 50 is meant to be an idea generator for investors and not a recommendation to buy or sell any specific securities. It is not personalized advice because it in no way takes into account an investor’s individual needs. As always, investors should conduct their own research when buying or selling individual securities. Click here to read our full disclosure on hypothetical performance tracking. Bespoke representatives or wealth management clients may have positions in securities discussed or mentioned in its published content.

Chart of the Day: Technical Timeframes

Berkshire (BRK/B) Unseats Meta (FB) For S&P 500’s Sixth Largest Stock

Yesterday, the news of the day was Alphabet’s (GOOG) massive gain on earnings that added $132 billion in market cap. The gain pushed Alphabet closer to the $2 trillion market cap club, which currently has two other members: Apple (AAPL) and Microsoft (MSFT).

Today, another mega cap Tech stock is in the spotlight for the opposite reason. After reporting weak quarterly results and forward guidance, Meta Platforms (FB) has shed over $225 billion in market cap. Given that is the stock’s worst single-day drop in its history as a public company, it is also the largest single-day drop in its history in terms of market cap. As a result of the decline, Berkshire Hathaway (BRK/B) has unseated FB for the S&P 500’s sixth-largest stock. At the moment, Berkshire’s market cap of ~$710 billion is more than $20 billion higher than Facebook’s (FB) $687 billion market cap.

Since the end of last year, BRK/B has actually now risen two spots in the rank of S&P 500’s largest stocks, eclipsing both Facebook (FB) and NVIDIA (NVDA). As for some other notables, Exxon Mobil (XOM) and Coca-Cola (KO) have made huge jumps in the rankings this year, rising 10 and 9 spots, respectively, to break back into the top 20 list. Looking at the change in rankings over the past couple of years, NVIDIA (NVDA) has also notably risen through the ranks at a very rapid pace, jumping 31 spots since the end of 2019. While Tesla (TSLA) was not a part of the S&P 500 at the end of 2019, taking where it would have ranked in the index back then, its 79-spot jump is even more impressive. Click here to view Bespoke’s premium membership options.