Bespoke’s Morning Lineup – 1/12/22 – CP-High

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“It is a way to take people’s wealth from them without having to openly raise taxes. Inflation is the most universal tax of all.” – Thomas Sowell

The big data release of the day is December’s reading on CPI, and the results came in slightly higher than expected with headline CPI rising 0.5% m/m versus forecasts for an increase of 0.4% while core CPI increased 0.6% compared to forecasts for an increase of 0.5%. On a y/y basis, headline CPI increased 7.0%, and as shown in the chart below, that’s the highest rate of change since 1982.

Despite the higher than expected readings, though, investors must have been expecting worse as futures have legged higher, led by the Nasdaq, in reaction to the report.

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including the latest US and international COVID trends.

Even as it was expected to be high, the rate of increases in consumer prices for the month of December is still a chart to behold. With the y/y change hitting 7.0%, it is the highest rate of change in CPI on a y/y basis since 1982.

Not only are consumer prices up significantly over the last year, but the pace at which we have reached these levels is nearly unprecedented. A year ago at this time, CPI was only rising at a y/y rate of 1.4%. That rate of increase has now accelerated by a full 5.6 percentage points. Going all the way back to 1951, the only other times that the rate of change in Y/Y CPI increased at a similar or higher rate were in 1951 and 1974.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Daily Sector Snapshot — 1/11/22

Small Pickup in Small Business Sentiment

The NFIB’s reading on small business sentiment has generally been on the decline over the past few years, although it’s also well off the lows set during the depths of the pandemic. In October, the index hit the lowest level since last March, and the past two months have seen a modest bounce off that October low, leaving small business sentiment middling versus its historical range.

While the headline number is far from any significant high or low, the individual components of the report are showing another story. Employment-related indicators are around some of the highest readings on record while a handful of other categories like Expectations for the Economy to Improve are near some of the lowest.

Rising slightly off the November reading, which was tied with November 2012 for the lowest on record, firms continue to have a historically sour outlook for the economy. While there are some other areas that are at the low end of their range of historical readings, this index is by far the most depressed area of the report.

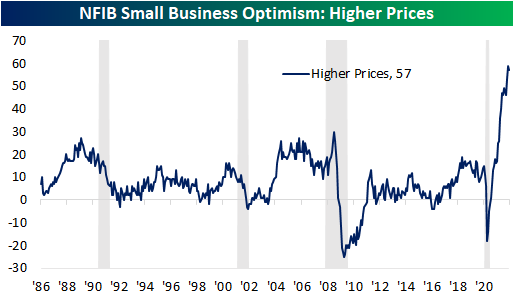

One potential reason for the pessimistic outlook could of course be the resurgence of COVID cases, but another likely reason, as we noted in today’s Morning Lineup, is inflation. The index tracking the rate at which firms report higher prices peaked in November but remains extremely elevated at 57. Meanwhile, a record high 22% of responding businesses reported inflation as their biggest concern.

Although costs are soaring, on the bright side, the employment situation is very strong. Firms reported an increase in hiring plans with the index rising to 28, the highest level since August while the net change in employment was positive for the first time since April. That is also only the second positive reading since the pandemic began. As with other costs, compensation is at an unprecedented level with the index setting a new record high in December. Compensation plans have now gone unchanged at 32 in back-to-back months. Responding firms also are reporting continued difficulties hiring with the Job Openings Hard to Fill index maintaining its lofty readings after gaining one point in December. Click here to view Bespoke’s premium membership options.

Bespoke Stock Scores — 1/11/22

Dividends Outperform With Discrepancy

In last week’s Bespoke Report, we performed a decile breakdown of year to date performance of Russell 1,000 members based on a variety of factors ranging from valuations to performance in 2021. One standout attribute of stocks that has been driving performance this year has been dividend yields. Expanding to the broader Russell 3,000, as shown below, the decile of stocks that pay no dividend is down a dramatic 5.69% on average this year. Meanwhile, deciles 7 through 10 with the highest dividend yields are all firmly in the green with average gains ranging from 1.93% to 2.38%.

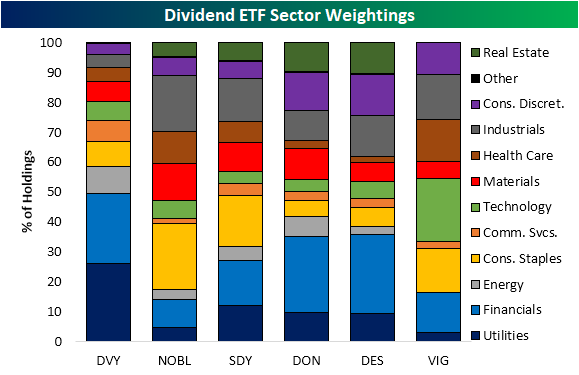

With dividend payers significantly outperforming, it is worth mentioning which stocks tend to have the highest dividend yields. In the chart below, we show the average dividend yield for stocks of each sector of the Russell 3,000. Utilities, Real Estate, and Financials all top the list with average yields above 2% while Health Care and Technology stocks, on an average basis, offer hardly any yield at all.

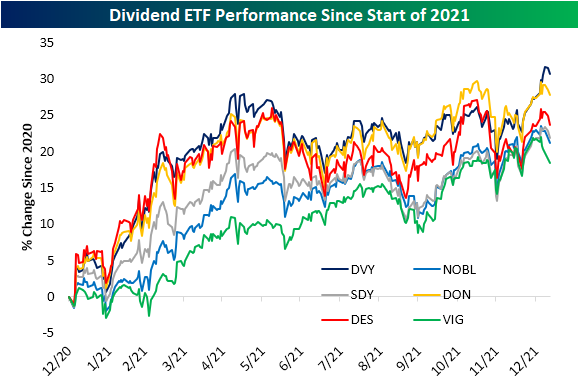

Given the outperformance of high-yielding stocks this year, some dividend-focused ETFs are up the most versus other investment styles highlighted in the styles screen of our Trend Analyzer, but there is a decent bit of dispersion for various ETFs tracking this theme as they have slightly different methodologies/more granular focuses.

The iShares Select Dividend ETF (DVY) is currently up the most year to date ( 2.5%) as it has also outperformed for most of the time since the start of last year (dark blue line). Additionally, the recent move higher resulted in a significant breakout to the upside. The next best performing dividend ETFs this year have been market cap focused with the WisdomTree SmallCap Dividend ETF (DES) gaining 0.09% and its mid-cap centered peer (DON) which has risen 0.29% YTD. Like DVY, these two ETFs have also tended to outperform over the past year, though neither has broken out in the same way as DVY, stopping short of prior highs even with solid gains late last year and to start this year.

On the other hand, dividend growers proxied by ETFs like the S&P 500 Dividend Aristocrats (NOBL), Dividend Appreciation ETF (VIG), and S&P Dividend ETF (SDY) have underperformed some of their peers since the end of 2020, but recently hit new highs and have generally trended higher since last year. More recently in 2022, though, they have actually sold off and are each in the red YTD.

Again, each of the ETFs shown above have different methodologies for selecting their holdings, ranging from a history of dividend growth or market cap size which factors into performance. One other factor, however, for the difference in performance also has to do with sector exposure. This year, Financials have been one of the top-performing sectors and as mentioned earlier, is one of the highest yielding sectors. The top-performing dividend ETFs have the highest weight in Financials. DVY, DON, and DES each have around a quarter of their holdings in this sector. The other best performing sector this year, Energy, also accounts for a significantly larger portion of DVY and DON versus other dividend ETFs. Conversely, VIG has a much larger weight in Tech and Health Care, which have been the second and third-worst performing sectors this year, and that exposure helps to explain much of its YTD underperformance. Click here to view Bespoke’s premium membership options.

Chart of the Day – Nasdaq 5-Day Declines of 5%+

Bespoke’s Morning Lineup – 1/11/22 – Powell Time

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“We will use our tools to support the economy and a strong labor market and to prevent higher inflation from becoming entrenched.” – Jerome Powell

It’s a generally quiet day for data today, so investor attention will be focused on the Senate as Fed Chair Powell sits in front of the Senate Banking Committee for his renomination hearing this morning. With four rate hikes in 2022 now more likely than unlikely, investors will be intently focused on any comments from Powell related to rates and the pace of balance sheet run-off once lift-off begins.

Futures are essentially flat with a positive bias heading into the opening bell this morning as Europe rallies and gold and crude oil are trading higher.

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including the latest US and international COVID trends.

It was a moral victory for bulls yesterday as the Nasdaq 100 erased an intraday decline of more than 2.5% to finish the day modestly in positive territory. As good as the reversal felt yesterday, it is important to keep in mind that even with the reversal, QQQ, finished the day below the low end of its Q4 trading range and also lower than the prior high from early September. Once a solid level of support breaks to the downside, it can often act as upside resistance, so it will be important to watch how those levels hold in the days ahead on any rally attempts.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Daily Sector Snapshot — 1/10/22

J.P. Morgan Health Care Conference Kickoff

The 40th annual J.P. Morgan Health Care Conference kicks off today, and because of COVID concerns, this year’s event will be held virtually. One of the largest conferences for the Health Care sector, especially in regards to health care investment, this conference brings together investors and hundreds of companies to stay up to date on the pulse of the Health Care sector. Looking back since 2001, the conference has coincided with solid performance for the S&P 500 Health Care sector with positive performance 62% of the time and an average gain of 0.56% during the four-day event. During last year’s conference, which was also held virtually, the Health Care sector declined 0.7% which was the worst performance since 2009. As for the biotech industry, which the conference’s focus is rooted in since it began in the early 1980s, it heads into this year with three consecutive years of positive performance. Compared to the broader sector, the S&P 500 Biotech industry has averaged an even better 1.15% gain during the annual conference since 2001 and has seen a move higher a little better than three-quarters of the time. Click here to view Bespoke’s premium membership options.

Differentiation Within Growth

So far in 2022, growth stocks have broadly sold-off and the Russell 1000 Growth Index has declined by 6.9%. However, not all growth stocks are the same, and it may be inaccurate to say that “growth stocks” in general are getting hit with this market downturn. Within the Russell 1,000 Growth index, names with the most aggressive valuations and higher multiples have performed far worse than those will lower multiples. Certain groups of the Russell 1000 Growth Index members have outperformed the S&P 500 on a year-to-date basis. The 20% of members with the lowest price to earnings ratios have averaged a YTD decline of just 1.7% while the S&P 500 has lost 3.3% of its value. The 10% of stocks with the lowest price to book ratio have outperformed the market as well, declining just 1.8% this year. As you can see from the charts below, the higher the multiple, the worse the 2022 performance. The 20% of members with the highest P/B ratios have averaged a loss that is over three times that of the S&P 500 (10.5%). The 20% of stocks with the highest PE ratios in the index have averaged a reduction of 12.6%, almost four times the loss of the S&P 500.

A similar trend is seen when comparing YTD performance against price to sales deciles. The 10% of members with the highest P/S ratios have averaged a 15.9% turn down in 2022, while the 40% of names with lower P/S ratios have averaged a decline of 3.5%.

For investors looking for growth, there are two ways to look at this. The first line of thought is to believe that the most aggressive equities (think RIVN, PLUG, DOCU, CVNA, and UBER) have sold off at unreasonable rates, and there are presently buying opportunities. The other available option is to think that the outperformance from growth at a reasonable price stocks (i.e. OLN, RKT, OPEN, VRM, and GS) will continue moving forward as, among other factors, the fed hikes interest rates. Stay on top of market trends like growth versus value by becoming a Bespoke subscriber today. Click here to view Bespoke’s premium membership options.

Of the 25 stocks with the lowest P/E ratios in the Russell 1000 Growth Index, the average YTD performance is -1.5% (median: -1.4%), which is far better than the broader market. The average stock on this list is off of its 52 week high by 20.6% (median: 18.0%) and returned 33.3% from price appreciation alone in 2021 (median: 33.7%). 48% of these names are positive so far in 2022, which is impressive given that the Russell 1,000 Growth index has already fallen by 6.9% this year.