Bespoke’s Consumer Pulse Report – February 2022

Bespoke’s Morning Lineup – 2/4/22 – Jobs Day

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Always buy your straw hats in the Winter” – Benjamin Graham

There’s a lot of ‘straw hats’ on sale in the market lately, but the question is how far they are from their ‘final markdowns’. Futures were much higher overnight, but have been drifting lower ever since Europe opened for trading. Amazon.com (AMZN) is still up over 10% following its earnings report after the close yesterday, and that’s helping to keep Nasdaq futures marginally higher this morning while the S&P 500 is flat and Dow futures are down. One asset not on the sale rack is crude oil as WTI is firmly above $90 and looks headed to triple-digits.

The big market event of the morning was the January Non-Farm Payrolls report, and after two months where economists were expecting a strong report and received much weaker than expected news, today they were expecting a weak report due to Omicron, but as luck would have it, the results came in much stronger than expected. The initial reaction in the markets was for higher rates and lower equities, so it looks like bulls may be heading into the weekend disappointed.

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including the latest US and international COVID trends.

The market couldn’t keep bouncing forever, but even after the rally off of last week’s lows, yesterday’s decline was a tough one for bulls to stomach. As shown in the chart below, while the bounce brought the S&P 500 back above the 200-DMA – a level it still trades above now – it stalled out just below the 50-DMA, and yesterday’s sell-off brought it back below the highs from late last summer. How the S&P 500 trades today following AMZN’s strong report will likely say a lot in whether yesterday’s weakness is the beginning of another leg lower.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Bespoke’s Weekly Sector Snapshot — 2/3/22

A Little Less Negative

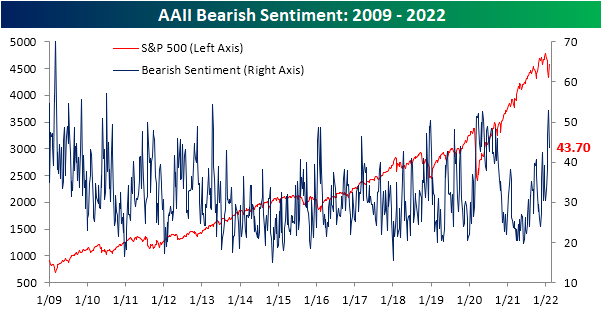

While the S&P 500 and other major indices are being pulled lower today, the past week has generally seen them reverse some of January’s losses, and as a result, sentiment has become modestly more optimistic. The AAII sentiment survey showed bullish sentiment tip back above a quarter of respondents in the most recent week rising to 26.5%.

Bearish sentiment meanwhile fell back to 43.7% after hitting the highest level since April 2013 last week.

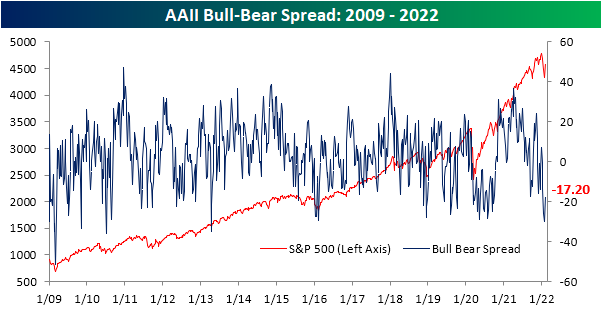

While bulls and bears both moderated in the most recent week’s survey, investor sentiment remains largely bearish. The bull-bear spread rose but remains deeply negative at -17.2. At that level, the bull-bear spread remains in the bottom 8% of all readings in the history of the survey.

While bulls did borrow from the decline in bearish sentiment, a larger share reported neutral sentiment this week. That reading rose six percentage points to 29.9% which is the biggest increase since the second week of December, but that level is still below the 30%+ readings that were common throughout the final quarter of 2021.

Other sentiment surveys like the Investor Intelligence survey of equity newsletter writers and the NAAIM Exposure Index, also saw a rebound in bullish sentiment this week which led our sentiment composite to regain some of the recent large declines. As with the AAII survey though, sentiment remains at a fairly bearish level in spite of this week’s improvements. Click here to view Bespoke’s premium membership options.

The Bespoke 50 Growth Stocks – 2/3/22

The “Bespoke 50” is a basket of noteworthy growth stocks in the Russell 3,000. To make the list, a stock must have strong earnings growth prospects along with an attractive price chart based on Bespoke’s analysis. The Bespoke 50 is updated weekly on Thursday unless otherwise noted. There was one change to the list this week.

The Bespoke 50 is available with a Bespoke Premium subscription or a Bespoke Institutional subscription. You can learn more about our subscription offerings at our Membership Options page, or simply start a two-week trial at our sign-up page.

The Bespoke 50 performance chart shown does not represent actual investment results. The Bespoke 50 is updated weekly on Thursday. Performance is based on equally weighting each of the 50 stocks (2% each) and is calculated using each stock’s opening price as of Friday morning each week. Entry prices and exit prices used for stocks that are added or removed from the Bespoke 50 are based on Friday’s opening price. Any potential commissions, brokerage fees, or dividends are not included in the Bespoke 50 performance calculation, but the performance shown is net of a hypothetical annual advisory fee of 0.85%. Performance tracking for the Bespoke 50 and the Russell 3,000 total return index begins on March 5th, 2012 when the Bespoke 50 was first published. Past performance is not a guarantee of future results. The Bespoke 50 is meant to be an idea generator for investors and not a recommendation to buy or sell any specific securities. It is not personalized advice because it in no way takes into account an investor’s individual needs. As always, investors should conduct their own research when buying or selling individual securities. Click here to read our full disclosure on hypothetical performance tracking. Bespoke representatives or wealth management clients may have positions in securities discussed or mentioned in its published content.

Chart of the Day: Technical Timeframes

Berkshire (BRK/B) Unseats Meta (FB) For S&P 500’s Sixth Largest Stock

Yesterday, the news of the day was Alphabet’s (GOOG) massive gain on earnings that added $132 billion in market cap. The gain pushed Alphabet closer to the $2 trillion market cap club, which currently has two other members: Apple (AAPL) and Microsoft (MSFT).

Today, another mega cap Tech stock is in the spotlight for the opposite reason. After reporting weak quarterly results and forward guidance, Meta Platforms (FB) has shed over $225 billion in market cap. Given that is the stock’s worst single-day drop in its history as a public company, it is also the largest single-day drop in its history in terms of market cap. As a result of the decline, Berkshire Hathaway (BRK/B) has unseated FB for the S&P 500’s sixth-largest stock. At the moment, Berkshire’s market cap of ~$710 billion is more than $20 billion higher than Facebook’s (FB) $687 billion market cap.

Since the end of last year, BRK/B has actually now risen two spots in the rank of S&P 500’s largest stocks, eclipsing both Facebook (FB) and NVIDIA (NVDA). As for some other notables, Exxon Mobil (XOM) and Coca-Cola (KO) have made huge jumps in the rankings this year, rising 10 and 9 spots, respectively, to break back into the top 20 list. Looking at the change in rankings over the past couple of years, NVIDIA (NVDA) has also notably risen through the ranks at a very rapid pace, jumping 31 spots since the end of 2019. While Tesla (TSLA) was not a part of the S&P 500 at the end of 2019, taking where it would have ranked in the index back then, its 79-spot jump is even more impressive. Click here to view Bespoke’s premium membership options.

B.I.G. Tips – Charts We’re Watching

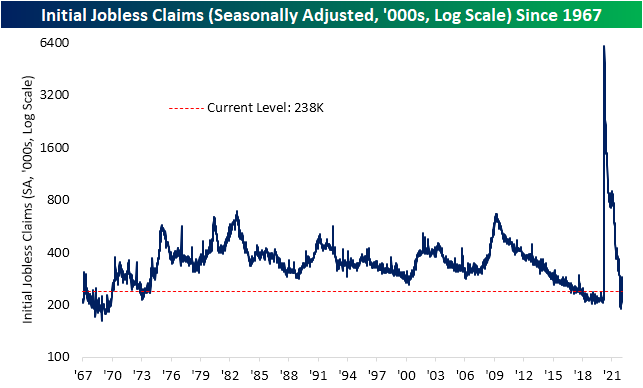

Claims Looking Healthier

Jobless claims spiked higher in early January, but the second half of the month saw some of that unwind with the most recent reading through the week of January 29th showing a drop to 238K from the previous week’s upward revised reading of 260K. That means claims have improved over the past couple of weeks and are still at a historically healthy level even if they remain off the pre and post-pandemic lows.

On a nonseasonally adjusted basis, after two weeks of smaller declines than what has historically been the norm, claims fell 11.7K WoW to 257K which was a larger drop than what could have been expected for the given week of the year (average decline of 4.89K since 1967). Heading into the next several weeks, NSA claims will continue to have seasonal tailwinds at their back while declining COVID caseloads will also likely help improve the claims situation.

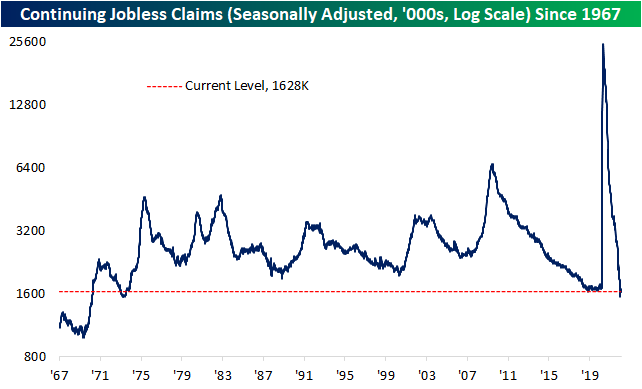

Delayed an extra week, continuing jobless claims continued to sit at the low end of the past several decades’ range. Seasonally adjusted continuing claims fell 44K this week down to 1.628 million. That is now slightly above the absolute low of 1.555 million set in the first week of January. Click here to view Bespoke’s premium membership options.

Bespoke’s Morning Lineup – 2/3/22 – It Was Fun While it Lasted

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“There are decades where nothing happens, and there are weeks where decades happen.” – Vlad Lenin

Good Morning Subscriber,

This earnings season, you could even say there are after-hours sessions where decades happen. Between earnings reports from Netflix (NFLX), PayPal (PYPL), and Meta Platforms (FB) last night, some very large market cap stocks have lost a fifth of their value overnight. These kinds of declines in reaction to one quarter’s worth of corporate performance are not exactly normal market events, and in the case of FB, today’s decline could be the largest single-day decline in market cap for a single stock in history! These are some unprecedented moves, and we’re not even halfway through earnings season!

We have a busy day of economic data ahead as well with Non-Farm Productivity, Unit Labor Costs, Jobless Claims, ISM Services, Durable Goods, and Factory Orders. Jobless Claims were already released and came in right around expectations while Non-Farm Productivity topped forecasts and Labor Costs were lower than expected. Following last month’s weaker than expected ISM Services report, the headline index is expected to show further deceleration this morning but still come in at a healthy reading of around 60.0. Durable Goods and Factory Orders, meanwhile, are both expected to show declines of less than 1%.

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including the latest US and international COVID trends.

Yesterday looked like an encouraging day for the Nasdaq 100 as the index traded and closed back above its 200-DMA, but that’s unlikely to last long as the index is expected to gap down more than 2% at the open this morning putting it back below its 200-DMA.

Going back to 2000, today will likely be the Nasdaq 100 ETF’s (QQQ) 106th downside gap of more than 2%. In the charts below, we show its performance from the open to close on the day of prior downside 2%+ gaps broken out by weekday along with the frequency of positive returns for each day of the week. Overall, the best day for QQQ to gap down 2% has been Wednesday as it has averaged a gain of 1.52% from the open to close with positive returns 54.5% of the time. Average intraday gains on Tuesday haven’t been nearly as strong (0.42%), but QQQ has been more consistent to the upside with gains 60% of the time. Unfortunately, Thursdays haven’t been a very good day for QQQ to gap down 2%+. On those 17 prior occurrences, QQQ’s average performance from the open to close has been a decline of 0.02% with positive returns less than a third of the time.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.