Bespoke’s Morning Lineup – 3/7/22 – The Market’s Case of the Mondays

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Facts do not cease to exist because they are ignored.” – Aldous Huxley

It hasn’t been a fun morning for equity investors around the world this morning as futures have been in the red everywhere you look. German stocks, while currently off their morning lows are currently on pace to close in bear market territory. Here in the US, futures are also lower, but well off their overnight lows.

The Russia-Ukraine war continues to drive headlines, and the place it is being felt the most is in crude oil prices. While prices of WTI still remain elevated at a price of more than $118, they actually briefly traded as high as $130 in overnight trading. How desperate is the market for additional barrels of oil given the disruption of Russian supplies? This weekend, US government officials actually visited with the Venezuelan government in an effort to boost ties with a country we cut off diplomatic relations with back in 2019.

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including the latest US and international COVID trends.

Mondays (or the first trading day of the week when Monday was a holiday) have not been friendly to bulls this year. In the nine weeks so far this year, the S&P 500 has opened the day lower seven times by an average of 0.54%, and today looks like it will be the eighth). The rest of the week has also been negative, but with an average gap lower of 0.03% for all other days of the week, Mondays have been notably weak.

While stocks have opened the day lower to kick the week off, selling hasn’t necessarily followed through to the rest of the trading day. After opening down by an average of 0.54% to start the week, SPY has averaged an intraday gain of 0.42% with positive returns just over half of the time. That compares to an average intraday decline of 0.20% for all other days of the week.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Bespoke Brunch Reads: 3/6/22

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, join Bespoke Premium with a 30-day free trial!

Ukraine

The bleak market outcome for Russia after Ukraine invasion by Paul McNamara (FT)

The removal of Russia from major financial markets indices is only the start of a long process of capital starvation for the country’s economy, which will have lasting and terrible consequences for Russian state capacity. [Link; paywall]

As Tanks Rolled Into Ukraine, So Did Malware. Then Microsoft Entered the War by David E. Sanger, Julian E. Barnes and Kate Conger (NYT)

Close coordination between the US intelligence community and security experts at Microsoft led to a rapid response against Russian cyberattacks in near-real time as the country sought to cripple Ukraine during the initial invasion. [Link; soft paywall]

The Terrible Truth So Many Experts Missed About Russia by Ben Judah (Slate)

Analysts and strategists across the Western world were operating under the assumption that the Russian President faced a series of constraints that he did not in fact pay any attention to. [Link]

Ripple Effects

Could Congress let you seize this Russian oligarch’s yacht? by Philip Bump (WaPo)

A downright unbelievable proposal is seeking to give private American citizens the right to seize assets of Russian oligarchs via Letters of Marque, a 19th century legal construct that hasn’t been used in almost two hundred years. [Link]

Ukraine war threatens to make bread a luxury in the Middle East by Maya Gebeily and Mena A. Farouk (Thompson Reuters Foundation)

On a combined basis, Russia and Ukraine supply a huge share of the grain that countries with relatively arid climates and weak farming capacity across the Middle East and North Africa rely on for basic calories. [Link]

State Capacity

‘Ways and Means’ Review: Financing the Civil War by Harold Holzer (WSJ)

A new book examines the role that innovative financial arrangements played in winning the Civil War for the Union, ranging from fiat currency to new debt instruments. [Link; paywall]

At cartel examination site; Mexico nears 100k missing by María Verza (AP)

Drug cartels operate with near-impunity in Mexico, and occasionally authorities discover the aftermath. One such example currently under investigation is a 75,000 square foot site miles from the border. [Link]

Former Police Chief Faked Death to Evade Charges, Officials Say by Eduardo Medina (NYT)

A small town police chief facing more than 70 felonies and fled to South Carolina after faking his death on a boat in the Lumber River. The former chief had stolen drugs and firearms from the town’s evidence locker and sold them for thousands. [Link; soft paywall]

Real Estate

L.A.’s most extravagant mansion sells for less than half its list price by Laurence Darmiento (Yahoo!/LAT)

A developer’s dream project collapsed with a mansion listed at $295mm selling for just $126mm, despite carrying a $256mm debt load from its construction. [Link]

COVID

Pfizer Covid vaccine was just 12% effective against omicron in kids 5 to 11, study finds by Spencer Kimball (CNBC)

A New York state study found a huge decline in efficacy among children during the Omicron variant surge, possibly due to lower dosages for young children compared to adults. [Link]

Economic Development

The Jolt: David Perdue targets Gov. Brian Kemp’s prized Rivian deal by Patricia Murphy, Greg Bluestein, and Tia Mitchell (The Atlanta Journal-Constitution)

Most state-level politicians would be thrilled to see $5bn invested in their state by a rapidly growing industrial company, but Georgia Governor candidate David Perdue apparently isn’t a fan. [Link]

Read Bespoke’s most actionable market research by joining Bespoke Premium today! Get started here.

Have a great weekend!

The Bespoke Report – 3/4/22 – War, Peace, And Prices

This week’s Bespoke Report newsletter is now available for members.

The invasion of Ukraine has sparked market volatility beyond equity markets, with historic moves in European fixed income this week alongside the biggest advance in wheat prices on record. We discuss the implications of the commodity price shock for equity markets and the Federal Reserve, which remains the elephant in the room when it comes to the outlook for stocks and the economy. We also review global economic data, the monthly jobs numbers released this morning, implications for the dollar’s rally in stocks, and more in this week’s Bespoke Report.

To read this week’s full Bespoke Report newsletter and access everything else Bespoke’s research platform has to offer, start a two-week trial to one of our three membership levels.

B.I.G. Tips – US Dollar Breakout

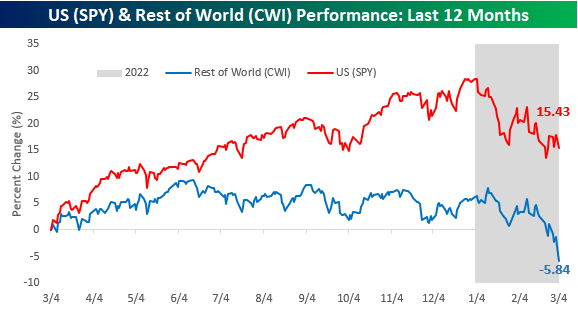

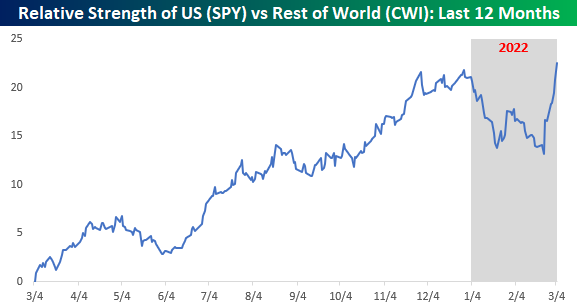

US Back on Top (Sort of)

Heading into 2022, there was a ton of optimism towards international stocks. After years of underperformance, the feeling was that valuations had become so skewed in favor of international stocks that they were due for their day in the sun. When the calendar finally did flip, international stocks came out of the gate positively, and as US stocks pulled back, international stocks held up much better. The resilience of international stocks didn’t last long, though. As the Russia-Ukraine war has escalated, investors have been ditching international equities en masse, while US stocks have actually held up relatively well. Over the last year now, US stocks, as measured by the S&P 500 tracking ETF (SPY) are up over 15%. International stocks, on the other hand, as measured by the SPDR MSCI ACWI ex-US ETF (CWI) are now down over 5%!

The relative strength picture between US and international stocks really illustrates how international stocks appear to have had their 15 minutes come and go. When 2021 ended, the relative strength of US stocks versus the rest of the world was right near a 52-week high. Once 2022 kicked off, though, US stocks saw a big slide in relative performance bottoming out on 2/23 – the day before Russia invaded Ukraine. Since that invasion, US relative performance has spiked higher and is right back to levels it started the year at. Investors have clearly fled to the relative safety of US stocks given the geo-political turmoil, so as long as these conditions remain, international stocks are subject to headwinds. If tensions do start to de-escalate, though, international equities may find themselves back in the spotlight again. Click here to view Bespoke’s premium membership options.

Bespoke’s Morning Lineup – 3/4/22 – The Least Important Jobs Report in Years

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“If you’re changing the world, you’re working on important things, you’re excited to get up in the morning.” – Larry Page

Every month at about this time, the financial world stops everything to focus on what is often considered the most important jobs report in years. Today’s employment report looks like an exception, though. With Fed Chair Powell already telling the markets that March’s meeting will come with a 25 bps rate hike, the Russia Ukraine war intensifying, and commodity prices spiraling out of control, today’s report could be the least important jobs report in years.

Futures are sharply lower this morning following a big sell-off in Europe as war tensions escalate. The big headline last night was news of Russia attacking and seizing control of Europe’s largest nuclear power plant. While initial concerns of a nuclear accident have subsided, investors are coming to a realization that the longer this all drags on, the more damaging to the global economy it all becomes. European benchmark indices are currently down over 3%, while US futures are down about 1%.

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including the latest US and international COVID trends.

Rising commodity prices have been the most direct impact of the Russia-Ukraine war, and crude oil is the most concrete example. Through this morning, WTI crude oil is up just over 20% on the week, and if these gains hold through the end of the day, it would be just one of five periods where crude rallied more than 20% in a week. In 1998, it got close to 20% but came up just short. As shown in the chart below, we’d also note that three of the prior four periods where prices spiked occurred during recessions. We’re at the point now where prices at the pump are higher on the way home from work than on the way in.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

The Bespoke 50 Growth Stocks – 3/3/22

The “Bespoke 50” is a basket of noteworthy growth stocks in the Russell 3,000. To make the list, a stock must have strong earnings growth prospects along with an attractive price chart based on Bespoke’s analysis. The Bespoke 50 is updated weekly on Thursday unless otherwise noted. There were 16 changes to the list this week.

The Bespoke 50 is available with a Bespoke Premium subscription or a Bespoke Institutional subscription. You can learn more about our subscription offerings at our Membership Options page, or simply start a two-week trial at our sign-up page.

The Bespoke 50 performance chart shown does not represent actual investment results. The Bespoke 50 is updated weekly on Thursday. Performance is based on equally weighting each of the 50 stocks (2% each) and is calculated using each stock’s opening price as of Friday morning each week. Entry prices and exit prices used for stocks that are added or removed from the Bespoke 50 are based on Friday’s opening price. Any potential commissions, brokerage fees, or dividends are not included in the Bespoke 50 performance calculation, but the performance shown is net of a hypothetical annual advisory fee of 0.85%. Performance tracking for the Bespoke 50 and the Russell 3,000 total return index begins on March 5th, 2012 when the Bespoke 50 was first published. Past performance is not a guarantee of future results. The Bespoke 50 is meant to be an idea generator for investors and not a recommendation to buy or sell any specific securities. It is not personalized advice because it in no way takes into account an investor’s individual needs. As always, investors should conduct their own research when buying or selling individual securities. Click here to read our full disclosure on hypothetical performance tracking. Bespoke representatives or wealth management clients may have positions in securities discussed or mentioned in its published content.