More Burning on Hot Inflation

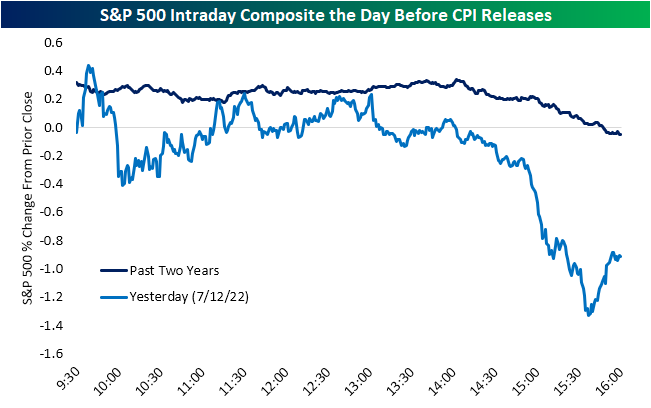

For most of the session yesterday, the S&P 500 was having trouble choosing a direction, but come the final hours of trading with a CPI release looming, the index took a decisive turn lower. Given rampant hot inflation over the past couple of years and its implications for changes to monetary policy, that sort of late day selling ahead of CPI prints has been the norm as shown below. On average for the past two years, the day before CPI releases has typically seen the S&P 500 trade higher for most of the session before turning lower and erasing its gains in the afternoon; just as we saw yesterday.

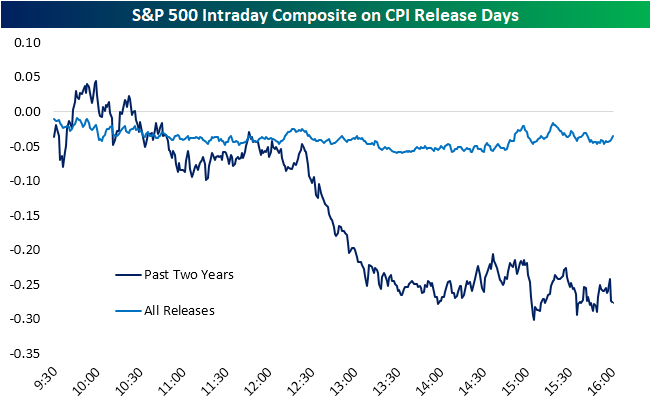

With another hotter than expected print this morning for both headline and core measures of inflation, yesterday’s late day sellers seem to have been on the right side of the trade as the S&P 500 has fallen further and is on pace for the sixth drop on a CPI print in a row. Taking a look at intraday price action of the S&P 500 on CPI release days, historically there has been a downward bias with all releases since 2000 averaging a drop of a few basis points by the close. Over the past two years it has been far worse with an average decline of 28 bps. Most of that drop has actually occurred after a bout of midday selling.

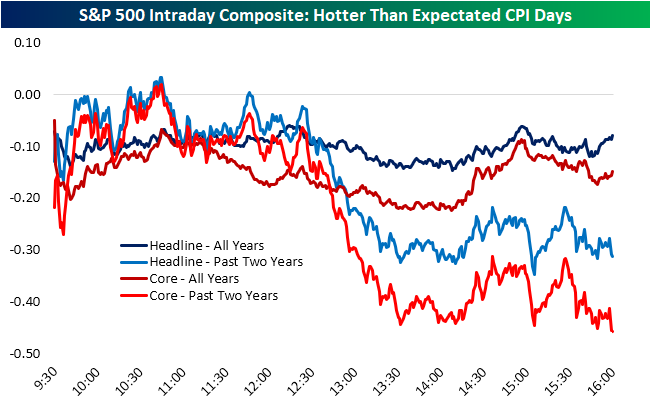

Using data from our Economic Indicator Database, filtering out for only times in which CPI has come in above expectations (on a month over month basis), that same pattern is apparent. The S&P 500 tends to trade in the red for most of the morning but the worst declines occur in the early afternoon before some stabilizing into the close.

In response to today’s hotter than anticipated release, the S&P 500 gapped down 1.2% which ranks as the fourth worst gap down for the index on a CPI day since at least 2000. Going back over the past two decades, there have only been a total of seven gaps down of 1% or more on a CPI day. Including today, four of those releases have occurred this year: February (-1.2%), March (-1%), June (-1.64%), and today (-1.23%). Taking a look at the intraday pattern of the S&P 500 across those 1% or larger gaps, the index has tended to continue to fall throughout the session with the lows of the day tending to occur around 2:30 EST with modest sideways action into the close from there. Click here to learn more about Bespoke’s premium stock market research service.

This Isn’t Normal

With inflation running out of control and markets furiously attempting to re-price Federal Reserve interest rate policy, we’re seeing some truly wild moves in the fixed income markets. This week, the big moves have come at the short-end of the Treasury yield curve as three-month Treasury yields have surged by 35 basis points this week alone. While the 2y10y US Treasury yield curve has been inverted for seven trading days now, the 3m10y curve, which is the FOMC’s preferred measure of the yield curve, has remained positively sloped, but the rate of flattening has really picked up in recent days and since early May has gone from around 225 bps to under 75 bps today. Click here to learn more about Bespoke’s premium stock market research service.

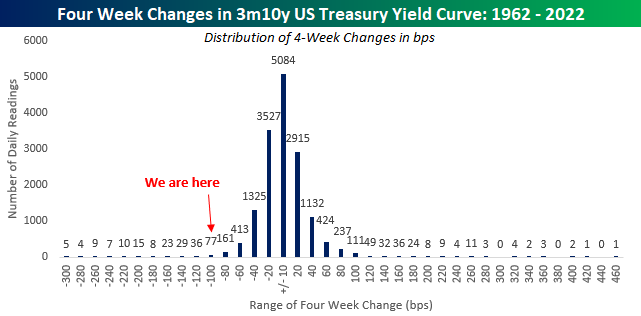

As mentioned above, the bulk of the flattening in the 3m10y curve has occurred more recently. The chart below shows the 20-day rate of change in the 3m10y US Treasury yield curve since 1962. The red line indicates the threshold for 100 bps of flattening in a four-week span which is where we are at now. Prior to the current period, there wasn’t a similar flattening of the 3m10y curve in a four-week span since the Financial Crisis. In August 2011, the rate of flattening got close to 100 bps in a four-week span but came up just shy. In other words, these types of moves in the yield curve don’t happen very often.

How often are they? The chart below shows the distribution of four-week changes in the 3m10y yield curve over time grouped into 20 bps increments. Including the last few days, where we are at in the current period (-100 to -120 bps of flattening in a four-week span) has only occurred on 77 trading days, and there have only been a total of 223 trading days where the yield curve flattened by 100 bps or more in a four-week period. On a percentage basis, that works out to less than 1.5% of all trading days. When it comes to markets, it seems as though there’s always something unique happening out there, and these days, you don’t see what’s happening at the short end of the Treasury curve very often.

Bespoke’s Morning Lineup – 7/13/22 Buckle Up

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Inflation is like toothpaste. Once it’s out, you can hardly get it back in again.” – Karl Otto Pöhl

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

The big CPI report that everyone is waiting for is finally here, and most investors appear to be leaning on the side of a stronger-than-expected report. However, after two weak days for equities futures are indicated higher in early trading.

Update – The report was just released and headline CPI came in at 1.3% compared to the forecast for 1.1%. On a core basis, CPI rose by 0.7% compared to forecasts for growth of 0.5%.

Earlier this morning, the IMF cut its forecast for US GDP growth down to 2.3% from 2.9%. This news is notable for two reasons. First, it comes less than a month after the IMF downgraded its growth forecast down to 2.9% in late June. Second, given the indication from the Atlanta Fed’s GDPNow model, which is calling for a Q2 contraction of 1.2% following Q1’s decline of 1.6%, the US economy would need to grow by 3.2% in the second half in order to reach that goal. Based on the trend in recent data and the Fed’s tightening bias, that level of growth seems optimistic.

In today’s Morning Lineup, we discuss moves in Asian and European markets, Chinese trade data, and economic data from around the world.

The days of the monthly employment report being ‘the most important indicator’ are long gone, and the new flavor of the month is CPI. Unfortunately for bulls, the trend of recent reports hasn’t been particularly market-friendly. As we have highlighted repeatedly in recent months, the headline CPI report has rarely come in weaker than expected. In the two years through May’s report, there have only been two weaker-than-expected headline CPI reports, which is easily the lowest number over a two-year span in at least twenty years.

When times are tough, there’s a stage in the process where people think that if they only wish hard enough, things will go their way. Unfortunately, elevated levels of inflation are a reality economists can’t simply hope away by consistently low-balling estimates.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

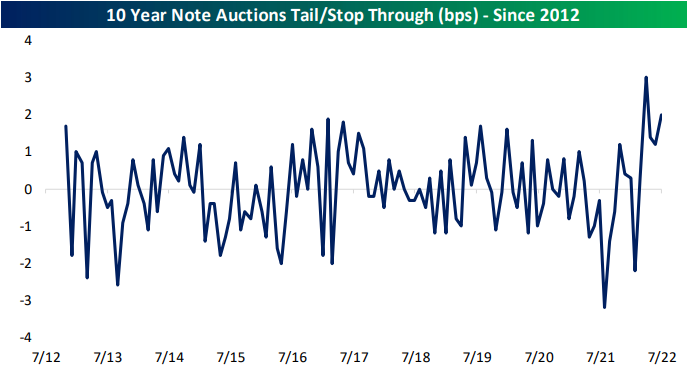

The Closer – Cranes, Dollars, And Auctions – 7/12/22

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, starting out with some comments on KoneCranes and the stock’s usage as a read on global industrial activity, we then take a quick glance across the moves in markets today (page 1). Next, we take a look into the dollar’s 52-week high and the implications for various sectors (page 2) as well as dollar correlated portfolios (page 3). We then turn to the USDA’s outlook for wheat crops (page 4) before finishing with a recap of another bad 10 year note sale (page 5).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Daily Sector Snapshot — 7/12/22

Growth at a Reasonable Price (GARP) Basket

Today we are debuting our Growth at a Reasonable Price (GARP) Basket, which utilizes a proprietary algorithm in an attempt to find stocks that may be mispriced relative to their growth. In this report, we highlight some of the flaws of pure growth and value strategies before diving into the potential benefits of a GARP strategy. There are 50 stocks included in the GARP Basket, with brief descriptions provided for each one. This basket is weighted in proportion to S&P 1500 sector weightings and will be updated on a quarterly basis, which gives each company the ability to report an additional quarter of earnings.

Bespoke’s GARP Basket is available at the Bespoke Premium level and higher. You can sign up for Bespoke Premium now and receive a 14-day trial to read our GARP report. To sign up, choose either the monthly or annual checkout link below:

Chart of the Day: Tarnished Gold and Copper

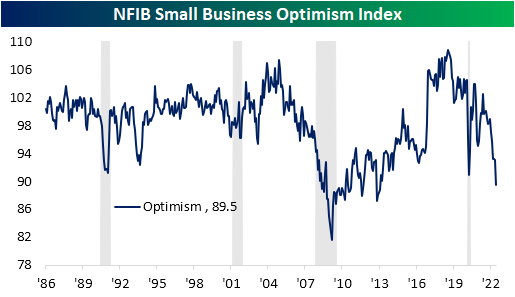

Small Business Expectations Disconnect

The only US release on the economic calendar today was the NFIB’s Small Business Optimism Index, and it was a big dud. Compared to last month’s low reading of 93.1, the index fell to 89.5 versus expectations for a much more modest decline to 92.8. As a result of that larger than anticipated drop, the index is now below the COVID low and down to the lowest level since January 2013.

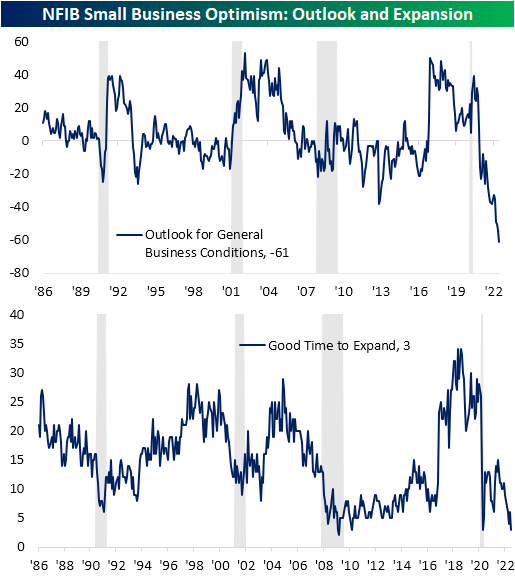

As the headline number is now in the 6th percentile of its historical range, several other components are similarly depressed including a record low reading in expectations for the economy to improve. Although some indices have managed to hold up decently—for example, reported inventory levels and the difficulty in filling openings remain in the top few percentiles since the survey began—breadth in June was very weak with many of the declines being historically large.

As we noted in today’s Morning Lineup, labor market indicators within the report have cooled off in recent months but remain at historically impressive levels. Meanwhile, inflation readings are also continuing to come in very elevated in spite of coincident declines in sales expectations.

Again, the worst category of the report was the reported outlook for general business conditions. This index set the bar for a record low even lower as a net 61% of respondents reported that they expect the economy to worsen in the months ahead. Given this, there is also a historically muted share of respondents reporting now as a good time to expand their businesses. That reading came in at a meager 3, which alongside April 2020 and March 2010, was the joint lowest level since March 2009.

The NFIB also provides some detail as to why businesses are reporting such a soured outlook regarding expansion. Half of the responses blamed broader economic weakness as the reason. Ironically, that goes against the fact that only 2% reported weak sales would be a reason while another 3% reported strong sales would be the reason to expand. Additionally, while inflation remains such a major concern, only 4% blamed higher costs as a reason to not expand. So while half blamed economic conditions as the reason not to expand, there were some contradictory cross currents.

While it is a drastically lower share at only 10%, the next biggest reason for not expanding was the political climate. As we have frequently noted in the past, one issue with the NFIB survey is that there has been a sensitivity to politics, namely a bias in favor of Republicans. Given the Democratic administration, it is not exactly surprising that political climate would come in second.

Another interesting point to note on this month’s survey regarded the uncertainty index. This measure essentially tracks the number of times respondents select “uncertain” or “don’t know” as an answer to a survey question. Here was another index that has reached the lowest level in over a decade. This month’s low reading would imply that firms have a decidedly negative outlook for the economy.

While sales expectations are down near the worst levels since the Global Financial Crisis and the COVID Crash, actual observed changes in sales have not yet cratered in the same way. That being said, on net there are more firms reporting lower sales than higher.

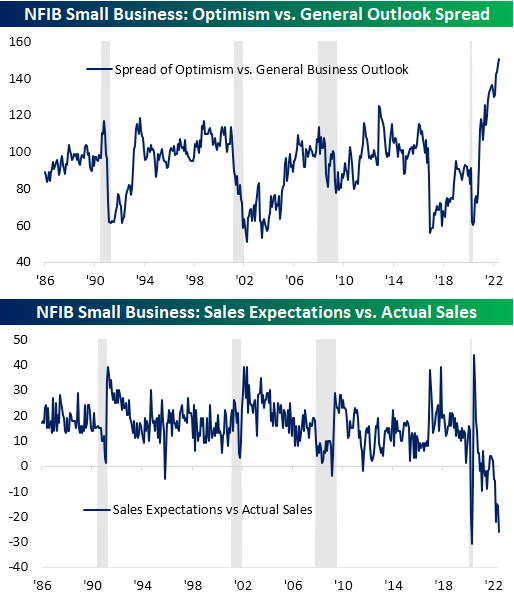

In other words, small businesses expect sales to get much worse than what current levels of sales would have historically implied. As shown below, the spread between those two indices has only been lower once on record and that was at the start of the pandemic. Similarly, the record low in General Business Outlook starkly contrasts with where the headline optimism index has been sitting. That spread is at a record high meaning again economic outlook is far worse than the overall level of optimism.

Another Curve Inverts

As of today, the percentage of inverted points on the yield curve reached the YTD highs seen in mid-June of 17.9%. This comes as the 10-year and 1-year invert, as well as the 5-year and 2-year. The inversion of points on the yield curve (particularly 2s&10s) tends to be cited as a leading recession indicator, due to the fact that higher near-term yields imply a higher risk in the near-term rather than the long-term, the inverse of what is typically true. The graph below shows the rolling percentage of inverted points on the curve over the last six months. Click here to learn more about Bespoke’s premium stock market research service.

As mentioned above, the spread between the 10-year and 1-year treasury inverted today, which is the first occurrence since October of 2019. Following prior inversions of this part of the yield curve since 1970, a recession has followed in the next two years 99.8% of the time which would suggest that a recession at some point in the next two years is almost certain. Following the first inversion in at least one year when a recession did follow, it has taken an average of 271 trading days to officially enter a recession. The shortest time it took to enter into a recession following 1s and 10s inversion was in 1973, when it took just 191 trading days. As mentioned, going back to 1970, recessions have followed within two years of an inversion 99.8% of the time. The only time that this part of the curve inverted and a recession did not follow within two years was after a brief stint in the fall of 1998.

Bespoke’s Morning Lineup – 7/12/22 – Euro Not Gonna Believe This

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The euro was born with great hopes. Reality has proven otherwise.” – Joseph Stiglitz

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

As the European economy continues to crater given rampant inflation, geopolitical instability, and labor/supply issues, the collapse in the bloc’s currency continued overnight as the euro reached parity with the US dollar for the first time since December 2002. While the round number generates a lot of headlines, it really means little in the broader picture of a weak European economy and what looks to be an even weaker outlook in the months ahead.

Over here in the US, things don’t seem all that much better. The week has started off slowly in terms of economic data, but this morning’s report from the NFIB on small business optimism came in much weaker than expected at 89.5 versus estimates for a reading of 92.5. Would you believe that sentiment among small businesses is now lower than it was at any point during the COVID lockdowns? Admittedly, the NFIB survey does tend to lean Republican, so with Democrats in control of DC, it’s not a complete surprise to see sentiment so weak. Given the macro backdrop, though, you can’t fault small business owners for being pessimistic. The last time the headline index from the NFIB was as low as it is now was in January 2013 at the beginning of President Obama’s second term. With the NFIB report behind us, the focus will now shift to tomorrow’s CPI.

In today’s Morning Lineup, we discuss moves in Asian and European markets, the latest developments on the war in Ukraine, and economic data from around the world.

Here is a surprising aspect of recent market events. With what seems like a near-constant focus that the ARK Innovation ETF (ARKK) gets, we were surprised that given the near 7% decline in the ETF yesterday there wasn’t more attention given to the fact that it had one of its 15 worst days since its inception in late 2016. The chart below shows the performance of ARKK since the start of 2017, and we have included red dots to show each of the 15 largest daily percentage declines in the ETF’s history. In the five-plus years that the ETF has been trading, all fifteen of the largest daily percentage declines occurred in either 2020 or 2022. Even more surprising is the fact that seven of the fifteen largest declines have all occurred since the start of May. What does it mean when extreme moves become the norm?

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.