Bespoke’s Morning Lineup – 10/20/22 – Opposite Week

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“It is clearly now the will of the parliamentary Conservative Party that there should be… a new prime minister.” – Boris Johnson 7/7/22

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

Just over three months ago, Boris Johnson resigned as UK PM, and now this morning, his successor, Liz Truss, just announced she will be stepping down as PM. Do you think she had enough time even to unpack her bags? After trading lower throughout most of the night, S&P 500 futures had flipped modestly into positive territory this morning, but in the immediate aftermath of the resignation announcement, they pulled back closer to unchanged while Nasdaq futures are lower. Treasury yields have been behaving with nothing more than modest moves higher in yields across the curve. Crude, however, is rallying an additional 2%+ and back above $87 per barrel while copper is also up over 2%. Over in China, there was some positive news that the country is considering a reduction of the required quarantine time required for travelers in the country.

Here in the US, the general trend in earnings remains primarily positive, but there have been some duds. Tesla (TSLA) is trading lower after reporting weaker-than-expected sales raising concerns over demand, and Allstate (ALL) dropped over 10% after announcing Q3 catastrophe losses of $673 million. Lastly, Alcoa also reported weaker-than-expected EPS and sales and lowered forecasts for shipments, but anyone following the company over the years knows that it is hardly a bellwether.

In economic data this morning, Initial Jobless Claims came in lower than expected (214K vs 233K) while Continuing Claims were only slightly higher than forecasts (1.385 million vs 1.378 million). Also, the Philly Fed Manufacturing report for October improved less than expected rising from -9.9 to -8.7 versus forecasts for a reading of negative five.

This week’s equity market performance has been the opposite of the pattern we have seen this year. Heading into the week, the S&P 500 has averaged negative returns on every weekday this year except Wednesday when the average gain has been 0.20%. This week, the only down day (so far) was Wednesday, and on Monday and Tuesday, the S&P 500 was up well over 1%. While it’s still early, equity futures are once again modestly positive heading into Thursday’s trading. There’s still plenty of time left in the week but wouldn’t that be a welcome trend?

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Bespoke Baskets Update — October 2022

Daily Sector Snapshot — 10/19/22

Chart of the Day: S&P 500 Drawdowns vs. Forward Performance

Housing Continues to Roll…Over

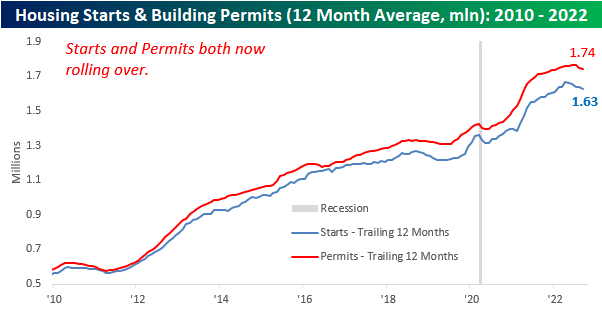

The latest update on Housing Starts and Building Permits from the Census Bureau was released this morning, and the results continue to reflect a significant slowdown in the sector. On a y/y basis, both starts and permits saw declines of 7.7% and 3.2%. respectively. The real weakness, however, has been in single-family units where starts are down 18.5% and permits fell 17.3% even as multi-family units were both up by double-digit percentages y/y. On a regional basis, the west was the only region to register a m/m uptick (4.5%) while the northeast was the only region registering an increase relative to last year. For permits, every region except the northeast was up m/m while it was the only region to register an increase on a y/y basis.

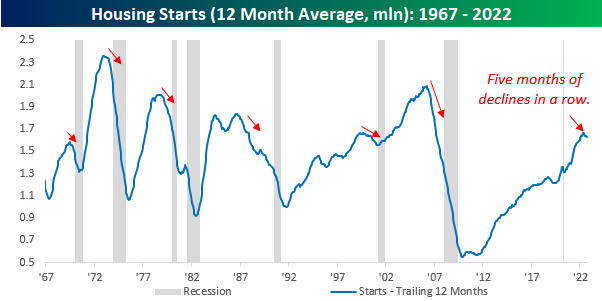

Housing Starts have historically done a good job predicting turns in the business cycle, so the fact that we have now seen five straight months of declines in this reading is just another indication of the risk of a recession on the horizon. We would note, however, that while recessions usually follow peaks in the 12-month average, they weren’t always imminent.

Looking more closely at the last few years, in addition to the decline in Housing Starts, the 12-month average of Building Permits has also started to roll over.

Single-family starts and permits have been even weaker. and both have now declined for five straight months. Also, the magnitude of the recent decline has been steeper than anything seen since the period from 2010 through 2012. Click here to learn more about Bespoke’s premium stock market research service.

Bespoke’s Morning Lineup – 10/19/22 – Worse Than 1987

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“It’s the nearest thing to a meltdown that I ever want to see.” – John Phelan, NYSE Chairman (1987)

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

35 years ago today, US stocks experienced their largest single-day decline in history as the Dow dropped 22.6%. Back then, before most Americans had 401Ks, the stock market wasn’t nearly as enmeshed in the lives of Americans as it is today, but the plunge still was THE story of the day prompting questions over whether it was a repeat of 1929 and the depression that followed. With the benefit of time and hindsight, the market and economy quickly moved on from the 1987 crash, and it barely even registers as a blip on long-term stock charts. Since the close on 10/19/87, the S&P 500 has had an annualized total return of 10.71%. Even more notable, though, is that had you invested in the S&P 500 on the Friday before the crash, you’re annualized total return over that span would have still been just short of 10% (9.99%). Not bad for the worst-timed trade of all time.

Moving to the present day, 2022 has actually been worse than 1987. After the crash in 1987, the S&P 500 was down less than 8% YTD. Today, even after a gain of nearly 4% over the last week, the S&P 500 is down more than 20% YTD or twice the decline of the S&P 500 at this point in 1987.

This morning, futures are in the red after trading higher overnight as yields surge with the 10-year nearing 4.10%. Building Permits and Housing Starts were just released and came in mixed relative to expectations with starts missing forecasts while starts came in a bit higher than forecast. Mortgage applications continue to decline, though, suggesting that the sector will continue to face pressure.

It’s now been a week since the S&P 500’s closing low on 10/12 (the intraday low was on 10/13), so we wanted to take a bird’s eye look at where things stand at the index and sector level. Of the Russell 2000 (IWM), Nasdaq 100 (QQQ), and S&P 500 (SPY), IWM probably looks best from a technical perspective. Of the three indices shown, it is the only one that didn’t violate the June lows on a closing basis and is also the only one that made a higher high even if it was just on an intraday basis. For both QQQ and SPY, the charts look very similar as last week’s lows represented lower lows, and the rally over the last few days has yet to make a higher high.

At the sector level, Financials have been leading the charge, rallying more than 6% over the last week. Of the remaining ten sectors, the only one not up more than 2.5% is Utilities. Despite the gains from the last week, though, the only sector that has managed to retake its 50-day moving average is Energy, and four sectors (Technology, Real Estate, Consumer Discretionary, and Utilities) still remain at oversold levels.

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Daily Sector Snapshot — 10/18/22

Bespoke Stock Scores — 10/18/22

Not All New Lows for Homebuilders

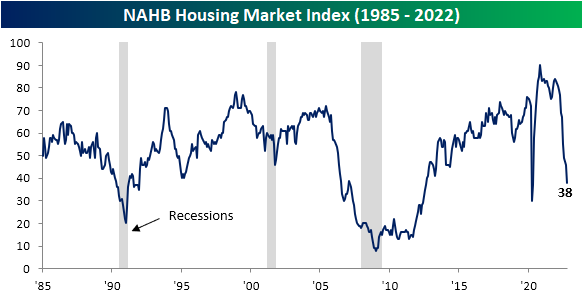

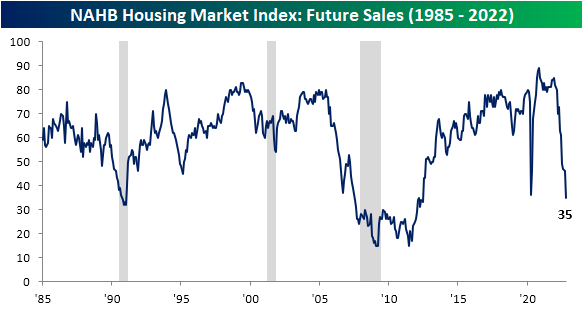

With mortgage rates running higher unabated and mortgage demand decimated, homebuilder sentiment has continued to tank. The latest reading on homebuilder sentiment from the NAHB hit a new post-pandemic low in October dropping from 46 down to 38. Outside of the weaker readings in May and April of 2020, August 2012 was the last time the index was as low as it is now.

Not only is the index at a new cycle low, but the 8-point month-over-month drop also ranks in the bottom 1% of all monthly moves. The declines in the present and future sales indices rank by similar magnitudes.

Although the headline index as well as sub-indices like present sales and traffic have not yet taken out 2020 lows, the index for future sales dropped to its lowest level since June 2012. As shown above, it has the lowest reading within its respective range historically of each of the sub-indices.

The only other index in the report that is below 2020 levels is the sentiment in the West region. While the Midwest and South have also fallen precipitously, the Northeast actually experienced a modest rebound in sentiment. Relative to other indices in the report, homebuilder sentiment in the Northeast is remarkably stronger with the index in the 62nd percentile relative to historical readings.

As for the technical picture of homebuilder stocks, recent declines have been a bit healthier than the broader market. Whereas major indices set new 52-week lows as recently as last week, the lows for the S&P 1500 Homebuilders Group at the end of September and the end of last week were between 7% and 8% above the June lows. While the line is somewhat choppy, relative strength versus the broader market has also been generally trending upward since the spring. In last Monday’s Closer, we further highlighted the disconnect between housing stocks and macro data.

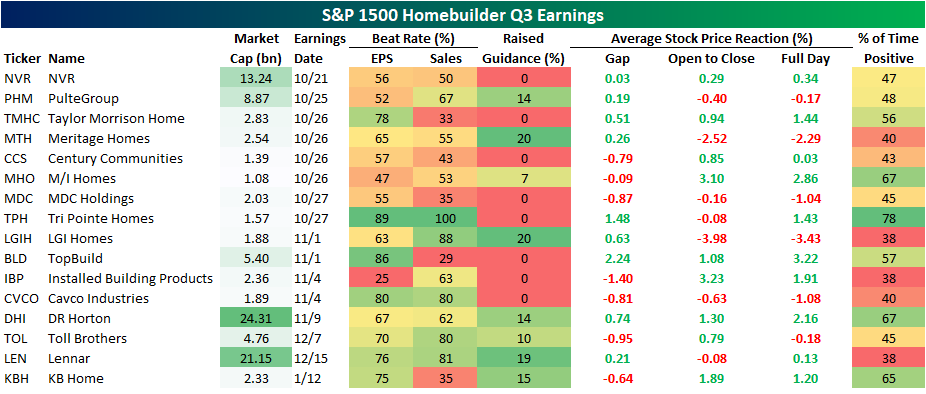

While homebuilder stocks have been holding up surprisingly well, earnings season is on the horizon which has the potential to change that picture; especially if said earnings start to mirror macro housing data. Using data from our Earnings Explorer database, below we show each of the S&P 1500 Homebuilder stocks as well as when they are expected to report earnings and what their historical Q3 earnings beat rates and stock price reactions have been.

Overall, Tri Pointe Homes (TPH) has been one of the strongest performers for Q3 with a positive reaction by the stock 78% of the time as it possesses the strongest beat rates as well. In fact, for TPH Q3 ranks as the best quarter of the year for stock price reactions. That is also the case for TopBuild (BLD) and KB Homes (KBH). Conversely, Q3 marks the weakest response to earnings for LGI Homes (LGIH), Cavco Industries (CVCO), Toll Brothers (TOL), and Lennar (LEN). Click here to learn more about Bespoke’s premium stock market research service.