S&P 500 Sector Weightings Report – July 2023

Bespoke’s Matrix of Economic Indicators – 7/3/23

Our Matrix of Economic Indicators provides a concise summary analysis of the US economy’s momentum. We combine trends across the dozens and dozens of economic indicators in various categories like manufacturing, employment, housing, the consumer, and inflation to provide a directional overview of the economy.

To access our newest Matrix of Economic Indicators, start a two-week free trial to either Bespoke Premium or Bespoke Institutional now!

Bespoke’s Morning Lineup – 7/3/23 – Play Ball!

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The essence of America — that which really unites us — is not ethnicity, or nationality, or religion. It is an idea — and what an idea it is: that you can come from humble circumstances and do great things. That it doesn’t matter where you come from, but where you are going.” – Condoleezza Rice

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

Welcome to the second half! It’s going to be a quiet start to the second half as most people seem to have taken the long weekend for July 4th. There’s been little corporate news to speak of, but we will get the ISM Manufacturing for June and Construction Spending report for May at 10 AM. After that, traders will start packing up for the holiday as equity markets close for trading at 1 PM eastern. Happy July 4th!

For anyone who didn’t follow the College World Series (CWS) this year, it ended up being an experience of extremes in the best of three series. Game one looked pedestrian enough with LSU winning 4-3 over Florida. However, it took 11 innings to get there with each team scoring a single run in three different innings during the first nine and LSU taking the lead in the top of the 11th on a Cade Beloso home run deep over the right field wall. In game two, Florida came back with a vengeance demolishing LSU by 20 runs in a 24-4 final. It was the most runs ever scored in a CWS game and the largest margin of victory since Notre Dame beat Northern Colorado 23-2 all the way back in 1957. The next day, it was LSU doing the thumping in game three and taking the title by scoring 18 runs to Florida’s 4. LSU ultimately took the title, but on both sides, pitching wasn’t a strong suit.

The first half of 2023 and 2022 look a lot like this year’s CWS. Last year, it was the bears on top in what was collectively one of the worst years for financial assets as stocks and bonds were all crushed. This year, it’s been the opposite as stocks have surged and bonds of all types are in the black on a YTD basis. Like game two of the CWS, which had the most lopsided win since 1957, the Nasdaq had its best first half since 1983, the Nasdaq 100 had its best first half ever, and Apple (AAPL) crossed the $3 trillion market cap threshold. Is that enough financial dopamine for you? And if pitching wasn’t the strong suit of this year’s CWS, central to the volatility of the last two years in financial markets has been the Fed, which at times has seemed equally inconsistent.

It hasn’t just been a strong for US stocks either. As shown in the snapshot from our Trend Analyzer below, equity ETFs from around the world all finished the first half in positive territory YTD. Not only that, but the last week of June was also positive for every one of the regional ETFs we track, and they are all above their 50-day moving averages. Talk about a tide lifting all boats.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Bespoke’s Brunch Reads – 7/2/23

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market-related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, join Bespoke Premium with a 30-day trial!

Government Regulation

Mama Mia! NYC Rules Crack Down on Coal, Wood, Fired Pizzerias – Must Cut Carbon Emissions Up to 75% (New York Post)

A new mandate by the New York City Department of Environmental Protection is forcing pizzeria owners to hire engineers or architects to design carbon emissions devices that reduce emissions from coal and wood-fired pizza ovens. Is this going too far? [link]

Brazil Votes to Bar Bolsonaro From Office for Election-Fraud Claims (NYT)

Citing a violation of the country’s election laws due to the spread of misinformation, former Brazilian President Jair Bolsonaro has been prohibited from running seeking public office for eight years. In the last election, Bolsonaro received 49.1% of the vote. [link]

Ethics

Harvard Scholar Who Studies Honesty Is Accused of Fabricating Findings (New York Times)

A Harvard Business School scholar with a focus on honesty has been cited for falsifying data in her published studies. Dr. Francesca Gino has authored or co-authored numerous papers studying honesty in insurance claims, tax filings, and other fields, but fellow researchers have found evidence of data manipulation and falsification. [link]

Economy and Markets

The Restart of Student Loan Payments Is Going to Pressure the Strong US Consumer, As 34% of Borrowers Say They’ll Be Unable to Make Payments (Markets Insider)

With student loan payments resuming soon, nearly one-third of US consumers say they will be unable to make payments on their student loans, while 37% claimed they needed to cut spending to make payments, and 29% claimed they will not have to cut spending. [link]

SEC Says Spot Bitcoin ETF Filings Are Inadequate (WSJ)

After numerous unsuccessful attempts, the SEC has once again refused applications from the Nasdaq and CBOE for a spot Bitcoin ETF. Unlike some rejections in the past, though, the SEC said these applications were insufficiently clear and comprehensive, and that gives the applicants the opportunity to refile the applications. [link]

China’s Economy Shows New Signs of Weakness (WSJ)

China’s reopening was supposed to provide a boost to global growth, but the opposite has been the case in the six months since the country first relaxed COVID restrictions. According to data released overnight, the manufacturing sector contracted for the third straight month. [link]

Corporate Bankruptcies and Defaults Are Surging – Here’s Why (CNBC)

Corporate bankruptcies have soared in 2023 due to high-interest rates. The cost of debt has risen, forcing many companies to file for bankruptcy or even default. So far this year, there have been 324 corporate bankruptcy filings and 41 corporate defaults in the US. [link]

Libor Is Over. We Still Need More Benchmarks to Replace It. (Barron’s)

The world’s most well-known benchmark interest rate for the last 40 years will be officially retired on June 30th. While the demise of Libor has been well-known (it started to lose its relevance after the financial crisis) and has been replaced with SOFR (Secured Overnight Funding Rate), new benchmarks should be created for purposes that SOFR is not an optimal benchmark. [link]

Science and Technology

A.I. May Someday Work Medical Miracles. For Now, It Helps Do Paperwork. (New York Times)

AI is making its way into another sector: healthcare. Many doctors are incorporating AI into their paperwork and write-ups, significantly reducing the time spent on these tasks. However, doctors believe it will take quite some time before AI is contributing to diagnoses for a number of reasons. [link]

“The crew is not drinking urine”: NASA System Helps Astronaut Pee, Sweat to be Recycled (USA Today)

To facilitate long galactic journeys, astronauts aboard the International Space Station are utilizing NASA’s latest innovation: Urine Processor Assembly- a process that recycles human urine by evaporating the liquid and using the humid air byproduct to recover water. The new process helped achieve the team’s goal of 98% water recovery. [link]

Distressed Firms and the Large Effects of Monetary Policy Tightenings (Federal Reserve)

A recent publication from the Federal Reserve showed that firms in high financial distress are significantly impacted by contracting monetary policy, whereas firms without financial distress are not significantly impacted. Firms in distress see lower investment and employment following a tightening shock, but debt decreases more for firms in distress than healthy firms following a tightening shock. [link]

Tropical Primary Forest Loss Up 10% in 2022 Despite International Pledges to End Deforestation (Earth.org)

During calendar year 2022, the equivalent of 11 football fields of tropical primary forest were destroyed every minute as total deforestation increased by 10% relative to 2021. The total loss resulted in an extra 2.7 gigatons of CO2 emissions, which equals the total of India’s annual emissions. [link]

WHO’s Cancer Research Agency to Say Aspartame Sweetener a Possible Carcinogen (Reuters)

The WHO’s cancer research group’s official report on aspartame is scheduled to be released on July 14, however, a leak from the organization reports the group plans on classifying aspartame as ‘possibly carcinogenic to humans’ alongside radiofrequency electromagnetic fields from mobile phones. Previous professional opinions around aspartame concluded a 60kg (132 pounds) human would have to drink between 12 and 36 cans of diet soda every day to be at risk. [link]

Use a loyalty card or digital coupon when grocery shopping? You’re being tracked. (USA Today)

Is the discount worth it? If you use a shopper loyalty card or digital coupons, odds are that the retailer is tracking things like age, marital or family status, languages spoken, education, gender, ethnicity and race, employment information, or other demographic information. They then take that information and sell it to other information brokers. Margins on groceries may not be good, but your personal info is another story. [link]

We are wasting up to 20% of our time on computer problems, says study (Tech Explore)If it seems like your computer is always broken, you’re not wrong. According to one study, people waste 11% to 20% of their time sitting in front of computers that don’t work properly. So much for being a productivity enhancer. [link]

Transportation

Why Pedestrian Deaths Are Skyrocketing in America (New York Magazine)

Pedestrian deaths in the United States are increasing faster than other transportation deaths. The main causes for this trend include the increased number of SUVs on the road and a migration out of cities where streets are less optimal for pedestrians. [link]

Joby Aviation reaches new FAA milestone as its electric flying vehicles get closer to takeoff (Fast Company)

With EV automobiles reaching the tipping point in terms of adoption, are air taxis next? Startup Joby Aviation announced that it has received a permit from the FAA to begin flight testing of its electric flying vehicle. [link]

Turn On Tune In, Drop Out

Magic Mushrooms. LSD. Ketamine. The Drugs That Power Silicon Valley. (WSJ)

Many CEOs and entrepreneurs in Silicon Valley are micro-dosing, or intentionally taking very small amounts of psychedelic drugs to reap productivity and creativity benefits. Some are micro-dosing to help with mental health issues. The development of legal psychedelics has already received significant investment and are projected to more than double by the end of the decade. [link]

Weed-GPT: A New AI Platform Helps Cannabis Consumers Learn ‘What’s Right For Me?’ (Forbes)

AI’s latest use: cannabis-education assistant. Los Angeles-based company Jointly is launching an AI chatbot (SparkAI) on its website aimed at helping cannabis consumers have purposeful consumption. Users can ask the chatbot “What types of cannabis products will help me solve my [insert health problem] problem?” and SparkAI will generate a response based on Jointly’s data collection. [link]

Read Bespoke’s most actionable market research by joining Bespoke Premium today! Get started here.

Have a great weekend!

June 2023 Headlines

The Bespoke Report Newsletter — First Half Review — 6/30/23

This week’s Bespoke Report newsletter is now available for members. (Log in here if you’re already a subscriber.)

Continue reading this week’s Bespoke Report newsletter by starting a one-month trial, or click the image below to view our membership options page.

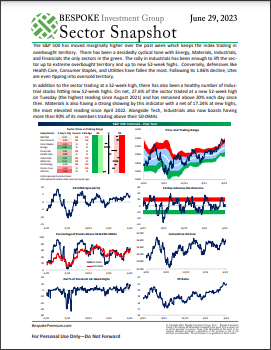

Daily Sector Snapshot — 6/30/23

Bespoke’s Morning Lineup – 6/30/23 – That’s a Wrap

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Perfection is a theory.” – Mikhail Baryshnikov

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

It’s been a quiet overnight session in terms of US-centric news, but European stocks have rallied to close out the first half as inflation data for the Eurozone was lower than expected. Headline CPI dropped from 6.1% down to 5.5% on a y/y basis, while core ticked up to 5.4% from 5.3%. Both reports, however, were lower than expected.

The only data on the calendar today is Personal Income, Personal Spending, and PCE inflation data at 8:30. Then at 10 AM, we’ll get the final reading of consumer sentiment from the University of Michigan. Personal Income came in at 0.4% versus forecasts for a gain of 0.3%. Personal Spending was weaker than expected rising just 0.1% versus forecasts for an increase of 0.2%. Headline PCE was right in line with forecasts at 3.8% while Core PCE rose 4.6% which was slightly below the 4.7% forecast.

With the Nasdaq having the third-best first half in its history, it has been as close to a perfect year as one could imagine for the index. The only two years that were better were 1975 (45.5%) and 1983 (37.1%), and with the Nasdaq up 29.9% heading into today, those two years are out of reach. Similarly, the next closest year behind this year is 1991, and back then the Nasdaq was up 27.3% in the first half. Therefore, unless the Nasdaq falls over 2.5% today, its ranking in the third spot seems safe. If this were the NFL, we’d be sitting Apple (AAPL), Microsoft (MSFT), Alphabet (GOOGL), Amazon.com (AMZN), Tesla (TSLA), Nvidia (NVDA), and Meta (META) today. Although AAPL may just get the start so it could cross the $3 trillion threshold.

It has also been a steady year for the Nasdaq as well. So far this year, the maximum peak-to-trough decline for the index has been 8.7%. That doesn’t sound too benign, but it’s well below the 12.5% first-half average dating back to 1972. It’s also the smallest first-half decline since 2017 when it fell just 2.9% in the first half. Looking back throughout the history of the Nasdaq, while years with sub-10% drawdowns in the first half haven’t been very common in the years since 2000 (just 8 in 24 years), prior to that they were much more common with 17 in 28 years.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.