Housing Starts and Building Permits Both Exceed Expectations

This morning’s report on Housing Starts and Building Permits for the month of June both came in stronger than expected. Housing Starts came in at a seasonally annualized rate of 1.189 mln compared to estimates for an increase of 1.165 mln. In the case of Building Permits, June saw an increase of 1.153 mln, which was just slightly ahead of consensus expectations of 1.150 mln. The table below breaks down this month’s report by the size of the unit as well as regions. In the case of unit sizes, both single-family and multi-family saw similar growth. As shown in the top line, overall Housing Starts ticked down 2% on a y/y basis in June. While that would seem to indicate a slowdown, all of the weakness was in multi-family units, which are down 22%. Single-family units, on the other hand, are actually up 13.4%. On a regional basis, Housing Starts in the Northeast surged 46.3% but are still down 47.8% y/y. The fact that there is such a wide disparity between the y/y and m/m numbers shows just how volatile this series is.

This morning’s report on Housing Starts and Building Permits for the month of June both came in stronger than expected. Housing Starts came in at a seasonally annualized rate of 1.189 mln compared to estimates for an increase of 1.165 mln. In the case of Building Permits, June saw an increase of 1.153 mln, which was just slightly ahead of consensus expectations of 1.150 mln. The table below breaks down this month’s report by the size of the unit as well as regions. In the case of unit sizes, both single-family and multi-family saw similar growth. As shown in the top line, overall Housing Starts ticked down 2% on a y/y basis in June. While that would seem to indicate a slowdown, all of the weakness was in multi-family units, which are down 22%. Single-family units, on the other hand, are actually up 13.4%. On a regional basis, Housing Starts in the Northeast surged 46.3% but are still down 47.8% y/y. The fact that there is such a wide disparity between the y/y and m/m numbers shows just how volatile this series is.

The 22% decline in multi-family units is especially notable given that it marks the largest y/y decline in that series in over six years. Part of the reason for the decline is that leading up to last June, there was a rush to get projects started due to the expiration of a tax credit on multi-family units in New York, so the recent decline is a bit of a giveback. We would be more concerned if there were similar declines in single-family units, but as shown in the second chart, that is something we clearly aren’t seeing at this point.

Dynamic Upgrades/Downgrades: 7/19/16

The Closer 7/18/16 – VIX Ain’t A Bargain, Earnings Gaps

Looking for deeper insight on global markets and economics? In tonight’s Closer sent to Bespoke clients, we detail why the low current reading on the VIX doesn’t necessarily mean it’s about to spike, and why even if it is buying VIX-related products may not be a profitable trade.

The Closer is one of our most popular reports, and you can sign up for a trial below to see it and everything else Bespoke publishes free for the next two weeks!

Click here to start your no-obligation free Bespoke research trial now!

ETF Trends: US Indices & Styles – 7/18/16

Over the last five days bond bulls have been reigned in a bit as EDV, TLT, and VCLT have undeperformed. The Japanese yen has also traded poorly, but the local-currency returns of the Nikkei have been strong even though Japanese investors enjoyed a holiday to start the week. That’s helped push up DXJ, which hedges currency exposure. Brazil has performed very well along with a smattering of other EMs like Taiwan and South Africa. Turkey’s coup attempt last Friday helped push it down by over 3.7% today in USD terms.

Bespoke provides Bespoke Premium and Bespoke Institutional members with a daily ETF Trends report that highlights proprietary trend and timing scores for more than 200 widely followed ETFs across all asset classes. If you’re an ETF investor, this daily report is perfect. Sign up below to access today’s ETF Trends report.

See Bespoke’s full daily ETF Trends report by starting a no-obligation free trial to our premium research. Click here to sign up with just your name and email address.

22.5 Analyst Ratings Per S&P 500 Stock

There are now 11,268 analyst recommendations for S&P 500 stocks. For those keeping track, that’s 22.5 analyst ratings per stock! Surprisingly, that’s actually down a bit from last year at this time when there were 23.7 analyst ratings per stock. Of the 11,268 analyst ratings, 5,492 are Buy ratings, 5,099 are Hold ratings, and just 677 are Sell ratings. Yep, analysts are and always have been a bullish bunch.

We’re currently working on a longer piece for paid members that looks at the most loved and hated sectors and individual stocks. Below is another chart from the piece that shows the number of analyst ratings per stock by sector. As shown, Energy stocks are actually the most widely covered at the moment, with 31.2 analyst ratings per stock. Technology ranks second at 27.3, followed by Telecom at 25.4 and Consumer Discretionary at 23.9. Utilities, Materials, and Industrials stocks are the least covered in the S&P 500.

Bespoke Stock Seasonality Report: 7/18/16

Chart of the Day – GOP Convention Starts Off Election Season

The GOP convention is under way in Cleveland, so we took the time to look through historical stock market returns following conventions, with a specific focus on which party goes first in a given year. The table below shows which party went first, the date of the convention, and the election day that followed, with the number of trading days between.

In today’s Chart of the Day sent to paid subscribers, the full table is included along with charts of the S&P 500 for each year divided into years when each party went first. Sign up below for a free trial today to view.

B.I.G. Tips – Post Brexit Record Breadth

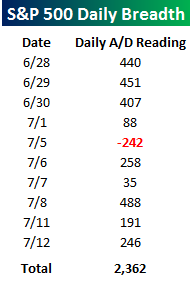

As we have highlighted in prior reports, by a number of measures the ten-day rally that followed the two-day sell-off following the Brexit vote was right up there with the strongest rallies on record. Not only was the rally in the S&P 500 extremely impressive, but breadth was nothing to sneeze at either. The table to the right shows the S&P 500’s daily Advance/Decline reading during that 10-day run. As shown, there were four different days where the S&P 500 had a daily breadth reading of +400 or more. That doesn’t happen very often! Over the entire 10-day span, the S&P 500’s 10-day A/D reading reached an unheard of +2,362.

As we have highlighted in prior reports, by a number of measures the ten-day rally that followed the two-day sell-off following the Brexit vote was right up there with the strongest rallies on record. Not only was the rally in the S&P 500 extremely impressive, but breadth was nothing to sneeze at either. The table to the right shows the S&P 500’s daily Advance/Decline reading during that 10-day run. As shown, there were four different days where the S&P 500 had a daily breadth reading of +400 or more. That doesn’t happen very often! Over the entire 10-day span, the S&P 500’s 10-day A/D reading reached an unheard of +2,362.

Earlier today, we sent an analysis of the market’s performance following prior extreme moves in short-term breadth to Bespoke Premium and Bespoke Institutional members. The list contains some interesting insights in how the market has performed following prior periods as well as how trends in breadth have changed over time. This one is can’t miss!

See the full B.I.G. Tips report by signing up for a monthly Bespoke Premium membership now. Click this link for a 10% discount ($89/month).

Home Builder Sentiment Ticks Lower in July

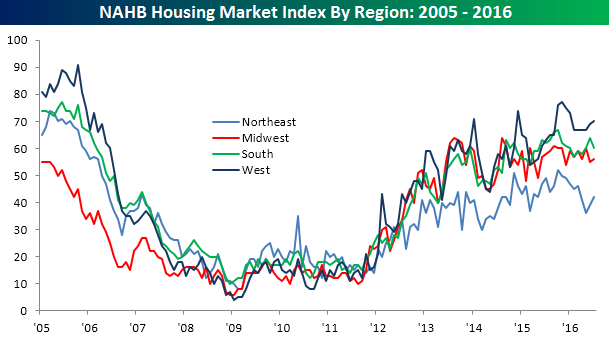

This morning’s release of the monthly sentiment survey from the National Association of Home Builders showed a modest decline in July. While economists were expecting the sentiment index to come in at a level of 60, which would have been unchanged from June, the actual reading declined slightly to 59. The table to the right breaks down this month’s report by traffic and both present and future sales as well as sentiment by region. Interestingly, while sentiment across all categories was down slightly this month, sentiment by region was up in every area of the country except the South, where the sentiment index declined by four points. In the Northeast, on the other hand, sentiment recouped some of its recent weakness by rising three points to 42. As shown in the lower chart, though, despite the big increase in the Northeast and the even bigger sentiment decline in the South, this month’s moves really did little to change the overall trends already in place.

This morning’s release of the monthly sentiment survey from the National Association of Home Builders showed a modest decline in July. While economists were expecting the sentiment index to come in at a level of 60, which would have been unchanged from June, the actual reading declined slightly to 59. The table to the right breaks down this month’s report by traffic and both present and future sales as well as sentiment by region. Interestingly, while sentiment across all categories was down slightly this month, sentiment by region was up in every area of the country except the South, where the sentiment index declined by four points. In the Northeast, on the other hand, sentiment recouped some of its recent weakness by rising three points to 42. As shown in the lower chart, though, despite the big increase in the Northeast and the even bigger sentiment decline in the South, this month’s moves really did little to change the overall trends already in place.

Bespoke Brunch Reads: 7/17/16

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

Labor Market

Big Businesses’ Latest Power Play: Raising Wages by Conor Sen (Bloomberg View)

During the 1990s-2000s, big business leveraged economies of scale to squeeze Main Street via lower costs and price competition. Now, that advantage may be the ability to pay higher wages. [Link]

Labor Pain And Labor Gain by George Casey (Builder Online)

The United States shed literally millions of homebuilding-related jobs in the aftermath of the last housing crash. Now, there’s a pronounced shortage of skilled trades that makes delivering new homes to market at a reasonable cost a major challenge. [Link]

Virtual Reality Versus Reality Itself

Pokémon Go Brings Real Money to Random Bars and Pizzerias by Polly Mosendz and Luke Kawa (Bloomberg)

Pokémon Go is the latest video game craze, and it’s having some impressive real world impacts that might open up new avenues for commerce. [Link, auto-playing video]

Virtual reality and Netflix: The future of in-flight entertainment is coming by Arjun Kharpal (CNBC)

The future of your flight across the Atlantic or the country is likely to be dominated by virtual reality headsets and streaming content; not all that different from the rest of the entertainment world! [Link, auto-playing video]

Business Model Changes

Mall Owners Push Out Department Stores by Suzanne Kapner (WSJ)

Many have wondered what the rise of Amazon and death of retail might mean for landlords (we’ve certainly pondered that question at length) but some malls are already pushing out retailers in favor of new anchor tenants that lean towards services. [Link, paywall]

ESPN reportedly planning to offer streaming package to cord cutters by Chris Welch (The Verge)

As total cable subscriptions come under pressure from fewer subscriptions sold to young people, the ultimate “bundle” member considers alternatives. [Link]

Live Streaming Breaks Through, and Cable News Has Much to Fear by Farhad Manjoo (NYT)

As news of the attempted coup in Turkey broke Friday night, our preferred sources of information were Twitter and Facebook live streaming video. While this article predates that particular news event, it discusses the same shift in consumption away from CNN, MSNBC, Fox News, CNBC, and Bloomberg TV that the above anecdote implies. [Link, soft paywall]

As Online Video Surges, Publishers Turn to Automation by John Herrman (NYT)

Similarly to cable news, online publishers are facing pressures from the explosion in video which dominates attention and traffic numbers. [Link, soft paywall]

Central Banking

The Fed’s FX swap facilities have been quite….to quiet? by Alexandra Scaggs (FT Alphaville)

Despite widespread fear around Brexit, there’s been very little activity on the facility the Fed uses to lend dollars to foreign central banks for re-lending to institutions in their jurisdictions. [Link, registration required]

UPDATE 3-ECB threatens legal action against Slovenia after police raid by Marja Novak and Balazs Koranyi (Reuters)

In a strange turn of events, Slovenian police broke into the country’s central bank to seize documents and computers in a possible violation of the ECB’s broad legal immunity. [Link]

How Have High Reserves and New Policy Tools Reshaped the Fed Funds Market? by Gara Afonso and Sam Stern (NY Fed Liberty Street Economics)

A series of new Fed tools and other non-policy factors have made the Fed Funds market, which the FOMC uses to manage US interest rates via a variety of monetary policy tools, much smaller, more thinly traded, and in all respects less relevant to the overall financial system. [Link]

The Business Of Finance

Reduced Viability? Banks, Insurance Companies, and Low Interest Rates by David Schawel (CFA Institute Enterprising Investor)

A thoughtful overview of what the low interest rates and an FOMC hesitant to move them up quickly means for investors in financial businesses from the New River Investments portfolio manager. [Link]

Some international trends in the regulation of mortgage markets: Implications for Spain (BBVA Working Papers)

While the focus of this white paper is the Spanish mortgage market, it provides a helpful overview of mortgage and housing markets for a variety of countries that is a helpful reference for investors and economic observers. [Link, 31 page PDF]

London Metal Exchange faces broker revolt over fee rise by Henry Sanderson and Neil Hume (FT)

The venerable LME is trying to ramp up revenues and drive volumes to standardized products but the result may be a flight from the historically important pricing venue. [Link, soft paywall]

Eurozone Economics

Placing Ireland’s economic “recovery” in context by Matt Klein (FT Alphaville)

Ireland’s small economy and status as an international tax haven make traditional measures of its economy’s size largely unreliable, as Klein shows in this excellent post. [Link, registration required]

Can Europe Declare Fiscal Victory and Go Home? by Brad Stetser (Council on Foreign Relations Follow The Money)

An overview of fiscal policy in the Eurozone, which is constrained in aggregate by limitations on specific members of the currency bloc and an unwillingness to ramp up budget deficits from others. [Link]

Personal Geopolitics

Turkey flies the Coup by Emad Mostaque (Governments and Markets)

An informed overview of what the attempted coup in Turkey Friday night means for one of the largest EM economies, from one of our favorite commentators in the space. [Link]

The Shadow Doctors by Ben Taub (The New Yorker)

An intense, personal, fascinating, and horrifying story of the doctors at work amidst the chaos of the Syrian civil war, with special attention paid to the innovation and technological tactics they and their instructors in the West use to save lives. There’s also a heartwarming anecdote regarding Queen Elizabeth and her corgis, which long-time readers familiar with our appreciation for canines will enjoy. Warning: this story contains graphic descriptions of violent injuries and the treatments applied to save the lives of those hurt. [Link]

Strange But True

Banker Sitting in U.S. Prison Has a Most Incredible Tale to Tell by Christie Smythe (Bloomberg)

A former Wall Street trader in prison for insider trading in Alabama purports to shed light on the wiold world of Central Asian organized crime. [Link]

The Fake Factory The Pumped Out Real Money by Mario Parker, Jennifer Dlouhy, & Bryan Gruley (Bloomberg)

Faked production of biodiesel that led to cash subsidies from the US government is the focus of this fascinating read on an imaginary factory. [Link]

Investing

35-Year-Old Bond Bull Is on Its Last Legs by James Mackintosh (WSJ)

Unless you think interest rates can go deep into negative territory (to levels that would make it cheaper to store physical cash than own an interest-bearing asset; we think this is unlikely to occur anywhere around the world) there’s a feasible limit to how much further bond prices can rise. [Link, paywall]

Why I Like This Market by Andy Harless (Medium)

A brief overview of where the stock market currently sits on a relative and behavioral basis. [Link]

Ridesharing

Vancouver Is Silicon Valley North. So Why Doesn’t It Have Uber? by Gerrit De Vynck (Bloomberg)

The regulatory tale of Uber’s failure to impress the powers that be in Canada’s third-largest city. [Link]

War of Words

Bill Ackman Says This Eccentric Short Seller Is ‘Certifiably Crazy’ by Tom Redmond, Adam Haigh, and Bei Hu (Bloomberg)

One of the more colorful Twitter accounts out there belongs to Australian investor John Hempton, who has proven to be a constant thorn in the side of acclaimed (and reeling) investor Bill Ackman. [Link]

Legal Questions

Are Police Allowed to Robot-Bomb Suspects? by Steven Nelson (U.S. News and World Reports)

Police used a robot with an explosive device to neutralize the killer in Dallas who targeted officers during a peaceful demonstration. That brings up complicated questions about the role machines should play in situations that could end with the death of a suspect; these are related to but distinct from ongoing questions about US drone policies overseas. [Link]