The Closer — Credit Rally, STIRs Soar, Wages Accelerate, Inflation Expectations Up — 7/31/18

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, we review a credit rally, energy equity outperformance versus crude, and the historically long stretch without an oversold reading for 2 year yields. We also dive into economic data: personal income & spending numbers, wages, and a few specific indicators from today’s Conference Board Consumer Confidence index.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

New High For High Yield Debt

As we’ve seen some of the highest flying stocks in the market pull back in the last couple of days, we haven’t seen much of an uptick in other market measures of risk. Since last Wednesday’s close (which was the day Facebook reported), the VIX has only risen one point from 12.29 to 13.29. That hardly signals a white-knuckle feeling on the part of investors. Similarly, the high yield market has seen virtually no reaction. Since last Wednesday, high yield spreads have actually declined slightly. Granted, most of these stocks getting hit so hard have no debt, so they don’t have much of a direct impact on the debt markets, but if investors are becoming more risk averse by lightening up on high fliers, one would think that there would at least be some sort of indirect impact.

Not only has high yield been relatively unscathed, but the sector has made a new high on a total return basis over the last few days, and that’s something we haven’t been able to say since 1/26, which was also the last time the S&P 500 closed at a new high. High yield debt is just one of many internal indicators we track to gauge the underlying trend and health of the market. In our newest Bespoke Report, we discussed a variety of other indicators and what kind of signals they were giving. To read our analysis, you can start a two-week free trial to Bespoke Premium today!

Bespoke Market Calendar — August 2018

Please click the image below to view our August 2018 market calendar. This calendar includes the S&P 500’s average percentage change and average intraday chart pattern for each trading day during the upcoming month. It also includes market holidays and options expiration dates plus the dates of key economic indicator releases.

B.I.G. Tips – August 2018 Seasonality

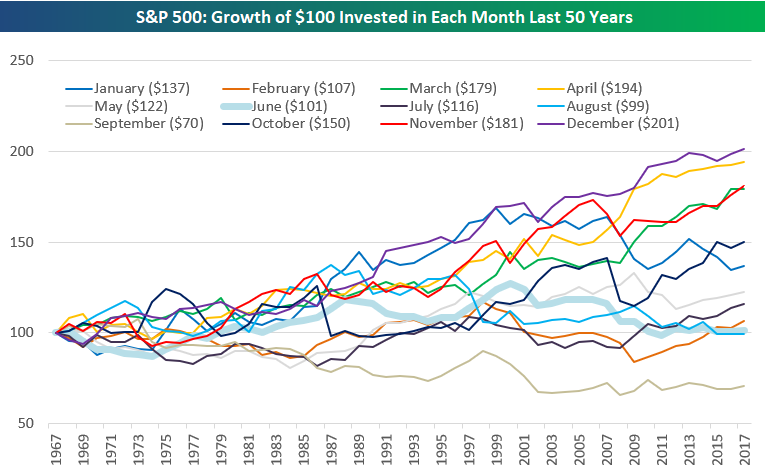

The chart below highlights the growth of $100 invested in the S&P 500 by month starting 50 years ago.

Had you only owned the S&P 500 during the month of August over the last 50 years, your $100 would now be $99 (for a decline of 1%). That’s not very good over a 50-year period! Historically, December has been the strongest month using this strategy, while the weakest month has been September, where $100 would now be worth just $70. Unfortunately, we have the two weakest months on the calendar coming up now that July is ending.

At the start of each month, we publish an in-depth report that analyzes seasonality trends for the US stock market, international markets, sectors, and individual stocks. To see which areas of the equity universe typically do the best and worst in the month of August, check out our just-published August Seasonality report.

This one is a must-read. To see it, sign up for a Bespoke Premium membership now!

B.I.G. Tips – Fed Days August 2018

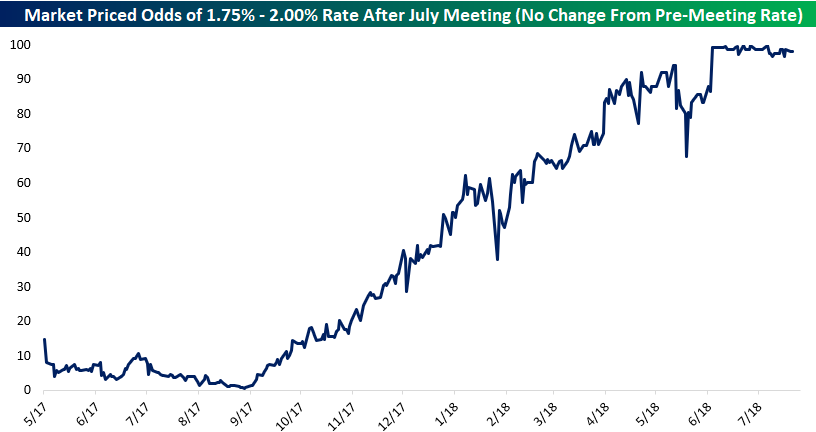

There have been four Fed Days so far this year (1/31, 3/21, 5/2, 6/13), and the Fed held the Fed Funds Rate steady on two of them (1/31 and 5/2) and hiked on two (3/21 and 6/13).

The Fed Funds Rate currently stands at 1.75%-2.00% (roughly 1.91% effective), and as shown below, the odds that the Fed makes no change with tomorrow’s policy release stand at roughly 98%. Earlier this year, odds for this outcome (driven mostly by lower odds of a June hike) fell as low as 68%, driven by concerns over Italian debt selling off, but that was temporary.

Ahead of every Fed Day, we publish a report that looks at the odds of future Fed rate hikes (or cuts), and we also analyze how the US stock market typically performs in response to Fed policy changes. We’ve just published our newest report ahead of tomorrow’s policy announcement.

This one is a must-read. To see it, sign up for a Bespoke Premium membership now!

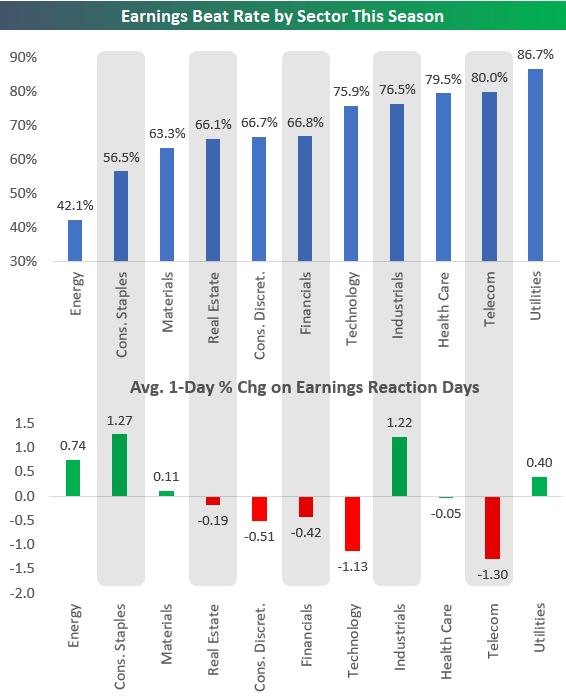

Q2 Earnings Rotation

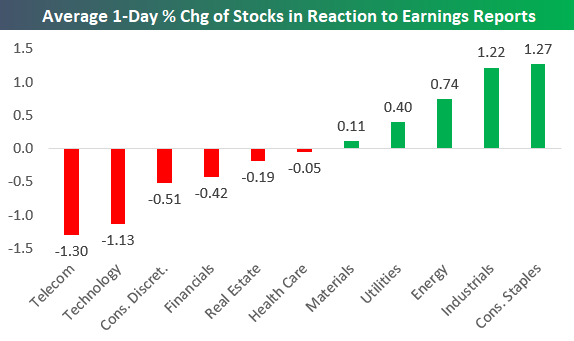

The average one-day price change of the 1,000 or so stocks that have reported earnings this season has dipped into negative territory. This means that investors are on average taking profits in stocks on the first trading day following earnings. This is in stark contrast to gains seen in reaction to earnings reports over the last few quarters.

There have been major differences in price reactions to earnings by sector this season. Five sectors are seeing their stocks catch bids following earnings, while six are seeing declines.

Below we show the average one-day price change in reaction to earnings for stocks by sector so far this season. As shown, Consumer Staples and Industrials stocks are averaging gains of more than 1.2%, meaning investors are snapping up shares in these sectors immediately following earnings releases.

On the flip side, stocks in Telecom, Technology, Consumer Discretionary, and Financials are averaging declines on their earnings reaction days. The declines have been most prominent in Telecom and Technology, where the average stock that has reported has fallen more than 1% on its earnings reaction day.

Leading up to the current earnings season, the Technology sector could do no wrong, and it was up by far more than any sector on a year-to-date basis. It’s only natural to see investors take some profits after a period of big gains, and it looks like they’re using earnings news this quarter to do just that. It has been a “sell the news” environment for Tech earnings so far this season.

Earnings beat rates have had a minimal impact on the performance of stocks in reaction to earnings this season. Energy and Consumer Staples stocks are beating earnings estimates at the lowest rate, but they’re both averaging one-day gains in reaction to their earnings reports. Tech stocks are beating at a very high rate of 75.9%, but as we noted above, they’re getting sold off on the news.

Sign up for our $1 New Member Special for more in-depth earnings season analysis!

Chart of the Day: Consumer Confidence – Mind the Gap

Bespoke Summary of Economic Indicators: 7/31/18

Bespoke Stock Scores — 7/31/18

Month End Rotation or Something Else?

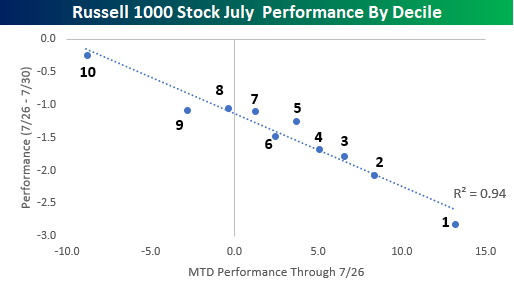

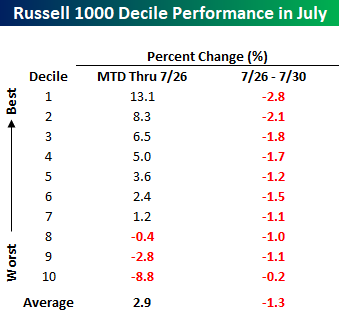

After a second straight day where growth stocks and July’s biggest winners up until late last week (in many cases one in the same) sold off sharply, bulls could use the proverbial ‘Turnaround Tuesday’ right about now. When looking at the performance of individual stocks within the Russell 1000 over the last two trading days, it’s hard not to see what looks an awful lot like month-end rotation and rebalancing out of winners. The table below groups the Russell 1000 components into deciles based on how they performed leading up to last Thursday (7/26). The stocks in the decile of top performers (decile one) were up an average 13.1% heading into last Friday, while the stocks in the decile of worst performers (decile ten) declined an average of 8.8%. Looking at how these stocks have performed since last Thursday’s close shows a clear trend where the top stocks have declined the most, while the stocks that were down the most have gotten by mostly unscathed.

The chart below further illustrates the trend as the deciles of top performers MTD through 7/26 are down the most, while the worst performers have held up much better.

Looking at the performance of each decile on a scatter chart, where the horizontal axis represents MTD performance through 7/26 while the y-axis shows performance since the close last Thursday, further illustrates the trend. As shown, each dot is practically right on the trendline! Clearly, these charts suggest that there is a good deal of rotation and re-balancing going on in portfolios as we approach month-end. That doesn’t mean it has to stop when August begins, but it is a trend we have seen to varying degrees towards the end of prior months in 2018.

With July winding down, we’ve been covering market seasonality for the month of August and how market internals stack up heading into the final full month of summer. To read all about it, you can start a two-week free trial to Bespoke Premium today!