Trend Analyzer – 9/26/18 – Back to Where We Were

With many indices falling on yesterday’s close from shakey investor reactions to political news, more US Index ETFs are below where they were mid-week last week. Eight ETFs are still overbought while six are now neutral. Although—once again similar to last week—the ones that are currently overbought are not at extreme levels. Smaller and Mid-cap funds have taken these recent hits the worst. Core S&P Small-Cap (IJR) continues to lead the charge downward, with S&P MidCap 400 (MDY) and Russell Mid-Cap (IWR) not far behind. Fortunately, IJR is still the only ETF that has moved below its 50-DMA at this point.

Bespoke’s Global Macro Dashboard — 9/26/18

Bespoke’s Global Macro Dashboard is a high-level summary of 22 major economies from around the world. For each country, we provide charts of local equity market prices, relative performance versus global equities, price to earnings ratios, dividend yields, economic growth, unemployment, retail sales and industrial production growth, inflation, money supply, spot FX performance versus the dollar, policy rate, and ten year local government bond yield interest rates. The report is intended as a tool for both reference and idea generation. It’s clients’ first stop for basic background info on how a given economy is performing, and what issues are driving the narrative for that economy. The dashboard helps you get up to speed on and keep track of the basics for the most important economies around the world, informing starting points for further research and risk management. It’s published weekly every Wednesday at the Bespoke Institutional membership level.

You can access our Global Macro Dashboard by starting a 14-day free trial to Bespoke Institutional now!

Morning Lineup – Happy Fed Day

It’s a relatively quiet morning for US equities ahead of this afternoon’s expected rate hike from the FOMC. US futures are slightly higher but have been fading. In trade news, there is some optimism out there on reports that China plans to cut tariffs on up to 1,600 items beginning on November 1st. Read all about today’s news and events in our Morning Lineup below.

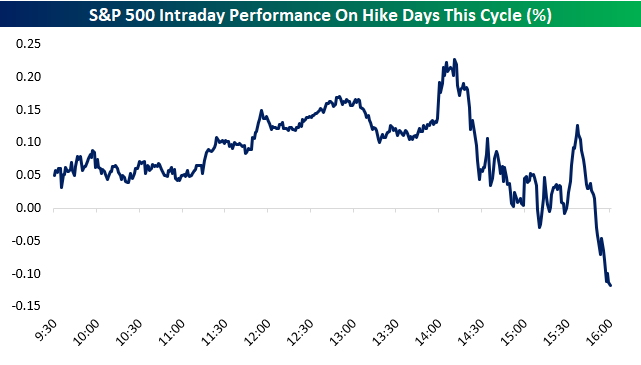

As mentioned above, today is also a Fed Day, and with that, we published our regular preview of the report in a B.I.G. Tips report yesterday. One chart we would like to highlight is a composite intraday chart of the S&P 500 on rate hike days over the last year. There have been 3 of them since last September, and the pattern that the S&P has taken on these days has been noteworthy.

As shown, the S&P has gotten off to a good start in the morning of these Fed Days, but afternoon trading has been a different story. After a drift lower from noon to 1:30 PM ET, we’ve seen the S&P catch a bid into the 2 PM rate announcement. From 2 PM to the close, however, we’ve seen the equity market sell-off pretty sharply to take the index into the red by 20+ basis points by the close of trading. It’s a small sample size, but something to keep in mind especially with futures already off their highs.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

The Closer — The Debt Is Fine, Global Trade & IP, Canada Update, And An SPV — 9/25/18

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, we argue that US corporate debt is less worrisome than it’s been made out to be. We also take a look at July global trade and industrial production data updated today before reviewing Canadian macro and a development from the UN today that signals a much larger trend in the world of global macro.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

FHFA & Case-Shiller Home Price Indices: What’s The Difference?

Two home price indices were released today: S&P CoreLogic Case-Shiller and FHFA House Price Index (sometimes referred to as HPI). These indicators both measure moves in home prices, but subtle differences in the methodologies with which each are calculated can result in variations between the two.

Both indices track the value of homes across the US using a repeat sales methodology. This essentially looks only at the prices of only existing single-family homes (multi-family homes and new constructions are excluded) that have been bought/sold at least twice. This way of indexing home prices helps to control for a property’s qualities—such as the size or style of house—that could affect the price.

While both CoreLogic’s Case-Shiller and FHFA use this type of Case-Shiller methodology, FHFA uses a slightly modified version. FHFA’s version of the house price index weights homes with long periods of time between sales differently than those with shorter time spans between sales. Both indices give less weight to a sale after ten years, but FHFA penalize them more than Case-Shiller. Additionally, FHFA weights all homes equally. Case-Shiller is value-weighted, meaning price trends for higher valued homes tend to have more of an impact on the index.

The way in which data is collected and organized are the other major differentiating factors. S&P CoreLogic uses local government assessor and records offices to get the valuation of homes. FHFA, on the other hand, uses the value of mortgages bought by either Fannie Mae or Freddie Mac. This removes refinancing appraisals that are picked up in the Case-Shiller data. Unfortunately, it fails to include a variety of mortgages such as subprime and VA loans. The FHFA breaks out state and regional prices with a lot more granularity; unlike Case-Shiller, it offers versions for census regions and states, while the Case-Shiller version only offers 20 metros and a national composite.

As you can see in the charts below, both indices closely follow each other. The most recent release has once again reaffirmed weakness in the housing market. The Case-Shiller Index for August has fallen to its lowest level since March 2010, sitting at 0.16% MoM SA. While mean home values are still appreciating, this trend downwards is the closest to depreciating home values that we have been seen in several years. Evident in the chart below, the Case-Shiller Index has been falling on a MoM SA basis for almost a year now. Despite a short uptick, the FHFA has pretty much been in the same boat.

This picture is only slightly rosier when looking at year-over-year seasonally adjusted data. We are nowhere close to home values depreciating, but it does appear that both indices are beginning to change their slight uptrend. Once again, this is nothing new for housing data, which has been on a rough run of late. Existing home sales missed estimates last week, while mortgage applications, new home sales, and pending home sales are all on the calendar this week. Perhaps, that will offer a brighter picture.

Chart of the Day: Confidence in Jobs

No Fears From Florence

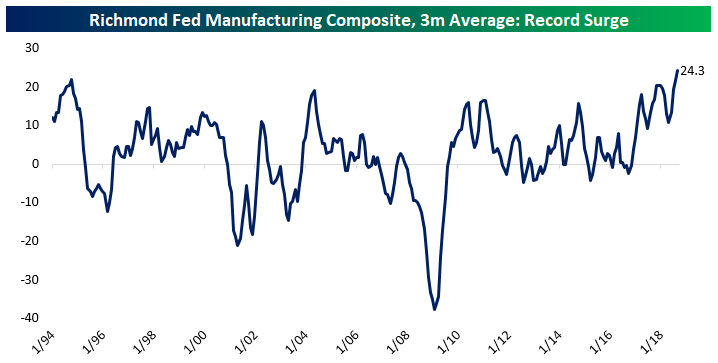

With Hurricane Florence crashing into the North Carolina coast earlier this month and the subsequent flooding that followed, a natural question among investors is how would the hurricane the regional economy. North Carolina is part of the Richmond Fed district, so a quick way to asses the damage would be to look at the most recent data from the Richmond Fed Manufacturing report. Below we show the three month average of the Richmond Fed’s manufacturing composite index. This index tends to be very volatile so we’ve smoothed it out a bit, but the September reading was a record at 29. For the states covered by the Richmond Fed (Maryland, Virginia, West Virginia, and the Carolinas), this was the best manufacturing backdrop in the history of the index’s data.

One thing to keep in mind with the most recent data is that while it covers the month of September, most of the survey responses were gathered before Hurricane Florence made landfall, so the full impact of the hurricane won’t be borne out until next month’s report. That being said, with the index at an all-time high, there doesn’t seem to be much of a negative impact even from survey responses that came in after the hurricane made landfall.

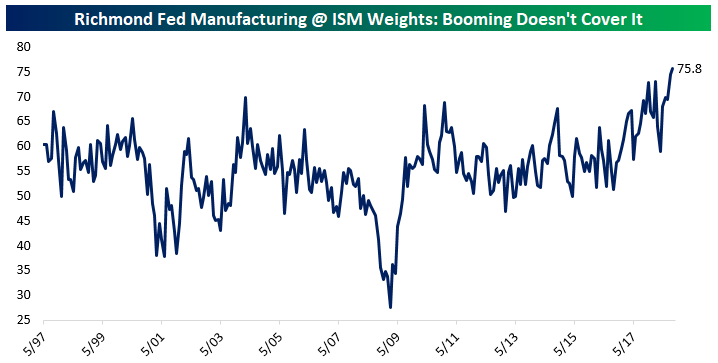

We would argue that re-weighting the Richmond data to be consistent with the ISM Manufacturing index delivers an even more impressive result. In the chart below, we show that re-weighted version of the index. Similar to the aggregate index, this re-weighted version is at a record, with a reading equivalent to an ISM Manufacturing print over 75! Simply put, the South Atlantic economy is cooking despite the challenge posed by Hurricane Florence.

The strong performance of the regional economy is also visible in home prices. The South Atlantic Region (which includes Delaware, Maryland, District of Columbia, Virginia, West Virginia, North Carolina, South Carolina, Georgia, and Florida) has seen its home price performance come in much stronger than the national since relative strength bottomed back in 2011. July data, updated this morning by the FHFA, showed new highs for the region’s prices versus the broader national index. Of course, this data does not include the impact of Florence, but it still shows a very positive backdrop for the regional economy heading into the storm.

B.I.G. Tips – Fed Days September 2018

Bespoke Stock Scores — 9/25/18

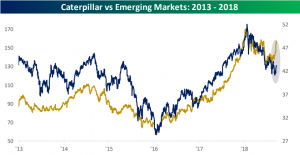

CAT vs Emerging Market

Shares of Caterpillar (CAT) have been an underperformer for most of 2018 due to slower sales growth outside of the United States. In recent weeks, this has not been the case. We have witnessed a big rotation into CAT as well as other Industrials as investors are looking to jump on laggards eyeing a rally.

CAT has resembled the performance of emerging markets over the past five years. Logically, this should not come as any surprise seeing as most emerging markets are reliant on natural resources, which is just the right market for CAT’s earth moving equipment. But in recent weeks, we have seen CAT far outpacing the MSCI Emerging Market ETF.

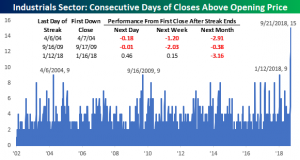

Again, CAT is not the only one of the Industrials that investors have rotated into in September. The sector as a whole has been stronger of late. As we discussed in our Morning Lineup today, the sector just went 15 trading days closing at a level higher than it opened. Back to when our data begins in 2002, that streak is by far the longest. April 2004, September 2009, and January 2018 were the only ones that come close — each at 9 days. In each of these periods, in the month following the last day of each streak, the Industrials sector was down for an average decline of 2.5%.