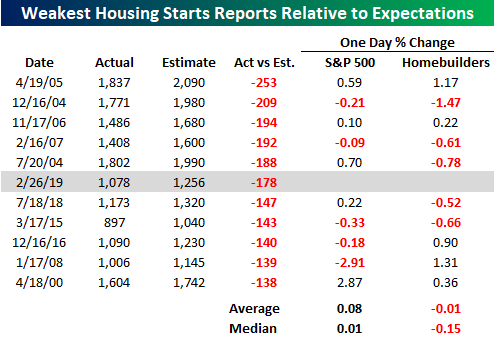

Weakest Housing Starts Relative to Expectations in 12 Years

Now that was a bad Housing Starts report! Just like the recent delayed report on Retail Sales, it may have been better if the finally released report on Housing Starts for the month of December was just swept under the rug. While economists were expecting the headline print to come in at a SAAR level of 1.256 million, the actual reported number came in at 1.078 million, missing expectations by 178K. Using our Economic Indicator Database, we found that there have only been five other monthly Housing Starts reports that missed expectations by a wider amount than the December print with the most recent occurring 12 years ago in 2007!

The table below lists the ten largest prior misses relative to expectations in the monthly Housing Starts report going back to 1998. For each instance, we also include the performance of the S&P 500 and the S&P 500 homebuilder group on the day of the report. While you would expect pretty substantial weakness following a miss of such magnitude, the results are pretty much mixed. Both the S&P 500 and the homebuilders were each up on the day in five instances and down on the day in the other five. In the case of the S&P 500, the bias was ever so slightly to the upside, while for the homebuilders the bias was slightly to the downside.

Morning Lineup – Cautious Tone Ahead of Powell Testimony

What happened in December? Between the delayed December Retail Sales report released earlier this month and this morning’s report on Housing Starts, either the economy hit a cliff or whoever was responsible for tabulating the data while the Federal government was shutdown needs to brush up on their calculations. Today’s report on Housing Starts came in at SAAR of 1.078 million, which was 178K below the consensus forecast of 1.256 million. Looking through our Economic Indicator Database, there has not been that big of a miss in Housing Starts relative to expectations in 12 years! It wasn’t all bad news, though, Building Permits came in better than expected. Besides this morning’s already released data, there’s still a lot on the schedule today, so read all about not only them but also overnight events around the world and this morning’s news in today’s Morning Lineup.

Bespoke Morning Lineup – 2/26/19

Yesterday, we noted the fact that the Shanghai Composite was bumping right up against a very long term downtrend after its 5%+ gain to kick off the week. Overnight, the index rallied higher in the morning but gave it all back throughout the trading day and closed with a decline of just over half of a percent. So, we’re going to have to wait at least another day (and likely more) before that downtrend gets taken out.

Another downtrend that’s provided pretty formidable resistance recently is the short-term downtrend in long-term US Treasury yields. At both the 10 and 30 year maturities, yields just can’t seem to increase the way so many have been calling for. In the case of the 10-year, yields bounced off the early January lows but quickly ran out of steam just shy of resistance at the 2.8% level, and since then have been trending lower right below the 50-DMA. For the 30-year it’s a similar story as the 50-DMA acts as a ceiling and the current yield of 3.02% is just 14 bps above the low print from early January.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

The Closer — Reversal At Resistance, Trade Troubles — 2/25/19

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, with the S&P 500 failing to hold above resistance and given overbought levels, we provide the near term prospects of the index. Moving on to economic data, we focus tonight on the declines in world trade volumes as seen through CPB’s data released today. We give some perspectives on the outlook of trade given what leading indicators and hard data have to say. We finish on a brighter note of stronger global industrial production also via the CPB.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

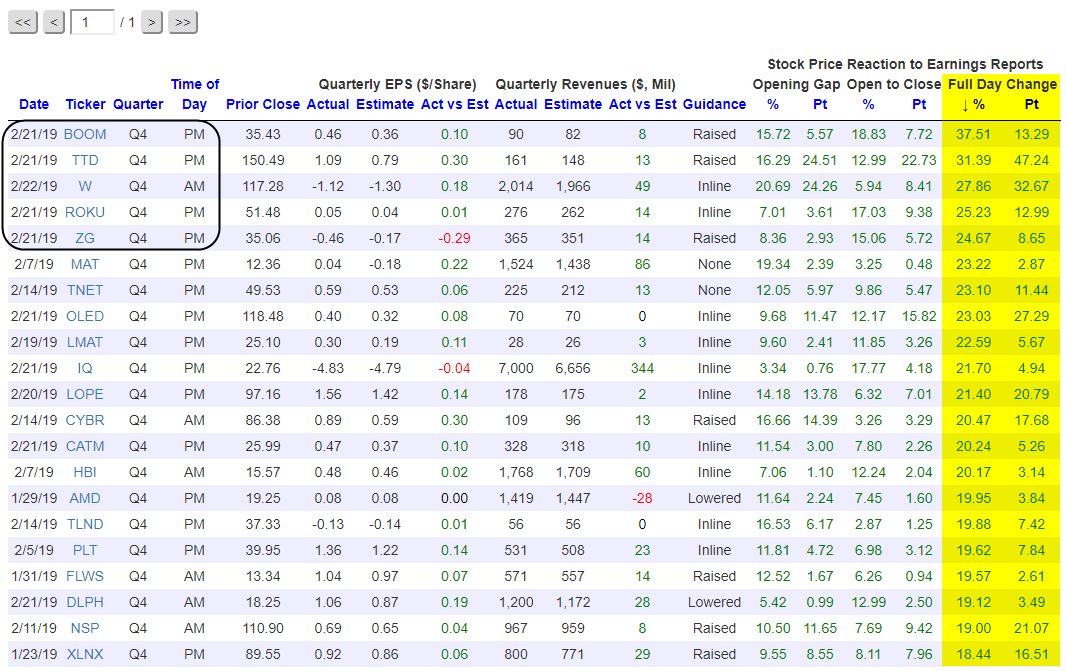

The Biggest Winners and Losers on Earnings This Season

Last Friday turned out to be a monster day for a handful of companies that reported earnings either that morning or the night before. In fact, of stocks trading greater than $10/share, the five best performers on their Q4 2018 earnings reaction days this earnings season (companies reporting between January 10th and February 22nd) all occurred last Friday.

Pulled from our popular Earnings Explorer tool, below we show a list of this season’s best-performing stocks on earnings. Again, to make the list, the stock had to be trading for more than $10/share at the close prior to its earnings report. Metalworking company Dynamic Materials (BOOM) ranks first with a gain of 37.51% last Friday. Media marketing company Trade Desk (TTD) ranks 2nd with a gain of 31.39%, followed by Wayfair (W) at +27.86%, Roku (ROKU) at +25.23%, and Zillow Group (ZG) at +24.67%.

The best performing stock on earnings that didn’t report last Friday was toy-maker Mattel (MAT), which gained 23.22% on February 8th following its report after the close on the 7th. Other notables on the list of biggest winners this earnings season include Advanced Micro (AMD), 1-800-Flowers (FLWS), and Xilinx (XLNX).

Along with seeing the 5 best performers on earnings this season, last Friday also saw the 1st and 3rd worst performers. Online shipping company Stamps.com (STMP) reported earnings after the close on Thursday the 21st, and the company also announced that it was ending its exclusive partnership with the US Postal Service. Investors sold first and asked questions later. STMP lost 57.77% of its value on Friday, which was nearly 30 percentage points more than the 2nd biggest loser this earnings season. Third on the list of biggest losers this earnings season is Kraft Heinz (KHC), which dropped 27.46% on Friday.

There was nothing special about last Friday that would have caused out-sized gains or losses for companies reporting earnings, but there were certainly a lot of fireworks!

Try out our unique investor tools with a free trial to Bespoke Interactive!

China’s Rally on “Trade”

Judging by most of the headlines today, the 5% rally in Chinese equities overnight was due to optimism over a trade deal between the US and China. The catalyst this time was attributed to President Trump’s announcement that the US would not implement previously announced additional tariffs on Chinese goods beginning on March 1st. A look more closely, though, would suggest that while trade may have had a positive impact on the performance of Chinese equities overnight, it is unlikely that it was the main driver.

In Monday’s Morning Lineup, we highlighted a number of factors which suggested that trade was not the primary driver of gains for Chinese stocks. Some of the factors we discussed behind this premise included the relative performance of domestic versus export-oriented Chinese companies, the performance of Financials, credit and capital flows, as well as market technicals. In addition to these factors, the intraday performance of the Shanghai Composite would also suggest that other factors were at work besides trade negotiations.

Looking at a timeline of events, President Trump made the announcement that the US would be delaying planned tariff increases at 5:50 PM eastern time on Sunday. That was more than two-and-a-half hours before the Chinese market opened for trading. Therefore, if the rally was based solely on trade, one would assume that the majority of the gains would have been priced in at the open. When Chinese equities opened for trading, though, the Shanghai Composite gapped up just 1.2% and then went on to rally more than 4% from the open to close. So either the Chinese market is extremely slow to digest news, or other factors played just as large a role in the rally as a delayed implementation of tariffs (that most people assumed was likely anyway). Now, it’s not uncommon for equities to rally on a particular piece of news and then have momentum add to the gains, but normally when events like this are the primary factor behind a move, the bulk of the gains would have been priced in at the open.

Chart of the Day: All the Market Does is Win

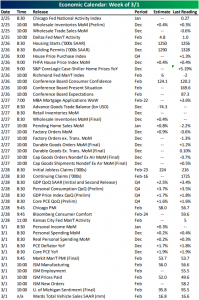

This Week’s Economic Indicators – 2/25/19

Last week, economic data was mixed in what was a light week with only 15 releases. The first half of the week only saw housing data, which came in stronger through homebuilder sentiment and mortgage applications. The Philly Fed’s Business Outlook collapsed to kick off a busy day of data on Thursday. Factory Orders and Markit PMIs also showed some weakening conditions in manufacturing.

This week, data activity picks back up with 34 releases scheduled. Earlier this morning, the Chicago Fed released their National Activity Index with a much weaker print. Later this morning, the Dallas Fed will release its regional Manufacturing activity index. Later in the week, the Richmond and Kansas City releases will come out. Tomorrow will be full of housing data including starts and permits, the quarterly House Price Purchase Index, FHFA Index, and Case-Shiller home prices. Pending Home Sales will come out on Wednesday. Thursday we get the combined first and second release of Q4 GDP data which is being forecasted to show a slowdown of 0.9% from the previous quarter. We will end the week and kick off March with Markit Manufacturing PMIs and the ISM Manufacturing Index.

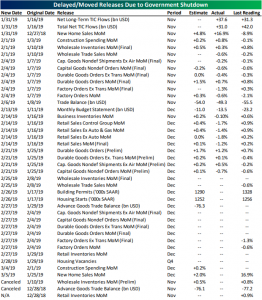

As we noted in previous weeks, a solid portion of recent data is from the backlog of delayed releases as a result of the government shutdown. While last week only crossed off a few of the December indicators, this week will basically get us all caught up. By the end of the day Friday, the only release left will be Construction Spending and New Home Sales for December which will come out next week.

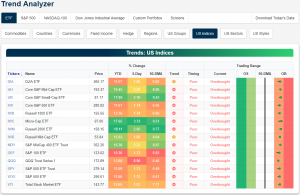

Trend Analyzer – 2/25/19 – Small Cap’s Big Jump

As we enter a new trading week, every major US index ETF remains overbought as small caps continue to lead. The Micro-Cap (IWC) rose the most last week at +3.33%. The next best ETF in the group was the Russell 2000 (IWM) gaining 2.85%. On a year to date basis, these two ETFs have also been the best performers with the Russell 2000 having now risen over 18%. That sort of strength can be seen throughout with every ETF now up double digits on a year to date basis. Last week, both the Dow (DIA) and Russell Mid-Cap (IWR) finally moved out of their downtrends. While these two are still the only ones not in downtrends, with the group broadly seeing solid gains, there is a good chance DIA and IWR’s peers will start to show changing trends as well though this is not guaranteed. Again, each ETF is overbought with the price of some, like IWM, nearing 10% above their respective 50-DMA. At one point last week, the indices narrowly missed moving into extremely overbought territory. In other words, some sort of mean reversion is increasingly possible.

Taken from our Chart Scanner tool, below you can see the impressive run these ETFs have gone on so far this year. More recently, they are approaching the upper end of the range seen during the market volatility at the end of 2018. For each ETF in the group, the 50-DMA has begun to pick up as well.

Morning Lineup – Shanghai Express

Here we go again. For what could possibly be the 100th time in the last two years now, futures are rallying on positive news regarding trade negotiations with China. The President tweeted last night that the US would be delaying planned increases on Chinese goods that were set to take effect on 3/1. Chinese stocks also had a monster night rallying over 5%. Now that China is out of the penalty box for the time being, though, it looks like the President is moving on to OPEC and telling the cartel that oil prices are too high and that they should “relax and take it easy.” Read all about overnight events around the world and this morning’s news in today’s Morning Lineup.

Bespoke Morning Lineup – 2/25/19

While Chinese equities rallied overnight for reasons related to trade and other developments (see the commentary section of our Morning Lineup), the long-term chart of the Shanghai Composite is currently at an interesting juncture. Looking at a chart of the index going back to 2015, last night’s rally sets the stage for a test fo the long-term downtrend starting at the 2015 highs. If bulls can take the Shanghai above this downtrend line, Chinese stocks could be off to the races.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Bespoke Brunch Reads: 2/24/19

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, join Bespoke Premium for 3 months for just $95 with our 2019 Annual Outlook special offer.

Economics

Deficits are Raising Interest Rates. But Other Factors are Lowering Them. by Ernie Tedeschi (Medium)

A quantitative explanation for why interest rates haven’t seemed to pay much attention to drastic increases in budget deficits, with attribution to a range of variables. [Link]

Disruption

“Hollywood is now irrelevant,” says IAC Chairman Barry Diller by Eric Johnson (recode)

Diller argues that movie studios used to exercise an effective cartel power over the movie business, but the entry of deep-pocketed tech giants has broken that power. [Link]

4Q Results Disappoint; Uber Feels Competitive Pressure as Growth Slows by Asad Hussain (PitchBook)

Quarterly financial results published by Uber suggest the company is struggling to maintain growth and may be at risk of losing out in core ridesharing markets, both significant concerns ahead of a potential IPO this year. [Link; 3 page PDF]

Dogs

Meet the dogs of the 2020 presidential race by Heather Timmons (Quartz)

Regardless of how you feel about the candidates, there are a parade of potential Presidential pooches to appreciate in the growing field of Democrats vying for a White House nomination. [Link]

The story behind the guy who went to a Dallas dog park covered in peanut butter by Matt Howerton (WFAA)

In the latest example of a fantasy football excess, a man covered himself with peanut butter and said hello to some canines in a Dallas dog park. [Link; auto-playing video]

Archaeology

Scientists discover the origin of Stonehenge stones – quarries 180 miles away by Ben Guarino (WaPo)

The famed rocks at Stonehenge have been traced to quarries in Wales, which for a Neolithic civilization dated to 3000 BC is a simply staggering achievement. [Link; soft paywall]

CRISPR

China’s CRISPR twins might have had their brains inadvertently enhanced by Antonio Regalado (Technology Review)

A widely-condemned experiment involving gene editing of human babies may have served to raise the intelligence of the twins, as well as making them resistant to HIV. [Link]

Climate

Look Who’s Betting on Climate Change by Matthew C. Klein (Barron’s)

Markets directly tied to the changing climate have very closely tracked the predictions of climate models which predict rising average temperatures. [Link; paywall]

Flight reaches 801 mph as a furious jet stream packs record-breaking speeds by Matthew Cappucci (WaPo)

Savage jet stream activity over the eastern seaboard drove a commercial jetliner to hit a ground speed of more than 800 MPH this week. [Link; soft paywall]

Sports

How Bryson trains his brain by Mike McAllister (PGA Tour)

Professional golfer Bryson DeCahmbreau uses a brainwave monitoring device to train himself to hone his ability to remain calm under pressure. [Link]

How former ref Tim Donaghy conspired to fix NBA games by Scott Eden (ESPN)

The inside story of how a ref rigged games, leading to hundreds of millions of dollars of ill-gotten gains and shedding new light on the challenges of maintaining a fair marketplace as sports betting balloons. [Link]

Nike Negativity

A Software Update Is Breaking Nike’s Expensive, Auto-Lacing Sneakers by Dan McQuade (Deadspin)

Nike recently released a pair of sneakers that rely on connection to an app in order to function properly, leading to predictably terrible results when a firmware update bricked some purchasers’ sneakers. [Link]

Zion Williamson’s injury from rare shoe failure puts spotlight on Nike by A.J. Perez (AZ Central)

A catastrophic failure for Nike footwear in prime time this week resulted in a knee strain for Duke’s projected first round draft pick. [Link]

Tech Dystopia

On YouTube, a network of paedophiles is hiding in plain sight by K. G. Orphanides (Wired)

Videos featuring children in what most people would consider innocuous situations are racking up millions of views and lots of advertising dollars thanks to interest from pedophiles. [Link]

You Give Apps Sensitive Personal Information. Then They Tell Facebook. by Sam Schechner and Mark Secada (WSJ)

Apparently not content to stockpile every scrap of data on its own users that it can, Facebook is also hoovering up data from other apps, typically without consent of users. [Link; paywall]

Mark Zuckerberg Promised A Clear History Tool Almost A Year Ago. Where Is It? by Ryan Mac (BuzzFeed)

Nine months after Facebook announced they would give users a “Clear History” function (giving them more control over their data), the tool is nowhere to be found; that’s part of a revealing pattern of behavior that the company has towards privacy. [Link]

Growing Up

The Overprotected American Child by Andrea Petersen (WSJ)

Denying children the freedom to learn independence may lead to anxiety, and parents aren’t alone in trying to find new strategies to let little ones try and experience a little more on their own. [Link; paywall]

WTF

At least 4 American veterans among group arrested in Haiti with weapons and tactical gear by Paul Szoldra (Task & Purpose)

In one of the strangest stories we’ve seen in a long time, Haitian police arrested a quintet of military-grade weapons-toting Americans driving unlicensed Chevy Suburbans through Port-au-Prince. [Link]

Health Care

Florida GOP governor working with Trump to import cheaper drugs from Canada by Peter Sullivan (The Hill)

Republicans in Florida are hoping to undercut the US pharmaceutical industry by importing drugs from Canada, a move the President reportedly supports. [Link; auto-playing video]

Drink

My Restaurant Was the Greatest Show of Excess You’d Ever Seen, and It Almost Killed Me by David McMillan (Bon Appétit)

A tale of withdrawal from the indulgence of the restauranteur lifestyle which was bringing nothing but misery to the owner of one of Montreal’s finest establishments. [Link]

Taxes

IRS data shows initial drop in average tax refund by Naomi Jagoda (The Hill)

It’s still very early but the early data suggests the average tax payer is getting a smaller return this year, one sign of how voters will assess the TCJA, passed at the end of 2017. [Link; auto-playing video]

Local Development

Scaring Off Amazon Will Backfire for the Left by Conor Sen (Bloomberg)

An argument that progressive energy tied to recent electoral success and policy innovation is only so much hot air. [Link]

Credit

The Bank for Japanese Farmers That Fuels the Global Lending Market by Telis Demos and Sam Goldfarb (WSJ)

A Japanese bank charged with investing the deposits of small farmers and fishing cooperatives has become a giant player in the CLO market, which securitizes loans made to US companies. [Link; paywall]

Radiation

Grand Canyon tourists exposed for years to radiation in museum building, safety manager says by Dennis Wagner (AZ Central)

Uranium ore stored in a few paint buckets at the South Rim of the Grand Canyon caused inadvertent irradiation of guests and workers. [Link]

Read Bespoke’s most actionable market research by joining Bespoke Premium today! Get started here.

Have a great weekend!