Morning Lineup – A Fresh Start

After a headscratcher of a week last week when it came to market expectations for the FOMC and the size of any potential rate cut at its meeting next week, thanks to a blackout on any further communications ahead of next week’s meeting, we won’t have to worry about any more conflicting headlines. It’s going to be a busy week for earnings, so make sure to check out our Earnings Calendar for a look at what’s on top. In terms of this week’s reports so far, results haven’t been particularly encouraging. Of the eleven companies reporting so far today, just over half have exceeded EPS forecasts while less than a third have topped revenue estimates. One notable loser today is Lennox (LII). Not only did the company miss top and bottom-line estimates but they also lowered guidance citing cooler weather int he quarter.

Read today’s Morning Lineup to get caught up on news and stock-specific events ahead of the trading day and a discussion of trade data out of Korea.

Bespoke Morning Lineup – 7/22/19

Now that the FOMC is in blackout mode, hopefully, the volatility related to expectations for the July meeting will start to subside. After all the ups and downs of the last week, markets are now pricing in a three-quarters chance of a 25 bps cut and a one in four chance of a 50 bps cut. This comes after Friday’s comments from Boston Fed President Rosengren on Friday that he doesn’t see the need for a cut at all.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Bespoke Brunch Reads: 7/21/19

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, join Bespoke Premium for 3 months for just $95 with our 2019 Annual Outlook special offer.

Oversight Needed

The Border Patrol Hits a Breaking Point by Garrett M. Graff (Politico)

Many of the problems faced by CBP are not caused by current political assignments but are the inevitable consequence of years without consistent management, expansion too rapid to handle masses of new recruits, and the theory that money will solve all problems. [Link]

Pentagon fails its first-ever audit, official says by Idrees Ali and Mike Stone (Reuters)

The Department of Defense was given a comprehensive audit by an army of accountants since December. This was the first-ever audit for the Pentagon, despite a 1990 law requiring an audit of all federal agencies. [Link]

Kids These Days

American kids would much rather be YouTubers than astronauts by Eric Berger (Ars Technica)

The latest moral panic over the state of American youths is apparently related to career choice, with a five-choice survey across three countries showing American kids would rather be a “vlogger/YouTuber” than astronaut, the least favored choice. [Link]

Some thoughts on youth sports by Myles Udland (Tumblr)

Myles considers his own struggles and positive experiences with youth sports and the larger incentives that drive children to specialize and hyper-focus on sports at a young age. [Link]

Economics

Measuring Labor-Force Participation and the Incidence and Duration of Unemployment by Hie Joo Ahn and James D. Hamilton (NBER Working Papers)

Statistical biases – that are artefacts of consistent survey methodology, not some sort of political pressure – are responsible for presenting a skewed picture of the US labor market. [Link; 51 page PDF]

Infrastructure Costs by Leah Brooks and Zachary Liscow (Brookings)

A new paper seeks to identify the increased construction costs for basic infrastructure like roads. Contrary to popular perception, materials and even labor inflation aren’t the key drivers, but instead that rising “citizens voice” decision-making processes, higher incomes, and higher home prices explain the results. [Link; 88 page PDF]

Not What You Paid For

Safe Deposit Boxes Aren’t Safe by Stacy Cowley (NYT)

Storing valuables is hard even when you outsource it to a location that should be secure: a bank. Cautionary stories on why your safe deposit box isn’t as safe as you think it ought to be. [Link; soft paywall]

Searches for ‘Canceling Amazon Prime’ Spike on Prime Day by Spencer Soper (Bloomberg)

Advertising doesn’t always work the way it’s intended to, and in the case of Amazon Prime paying customers sometimes forget that they’re paying until Prime Day reminds them. [Link; soft paywall, auto-playing video]

The women who win hundreds of sweepstakes per year by Zachary Crockett (The Hustle)

A unique online culture features a hunt for the ubiquitous sweepstakes, which can yield tens of thousands of dollars per year in winnings for the most dedicated prize hunters. [Link]

Europe

Swedes are getting implants in their hands to replace cash, credit cards by Lee Brown (New York Post)

Small RFID chips are being implanted in Swedes who use them to pay at the store, unlock doors, and monitor health metrics. [Link]

Older Employees Breathe New Life Into Europe’s Labor Market by Tom Fairless (WSJ)

Almost 90% of employment growth in the Eurozone between 2012 and 2018 came from workers aged 55 to 74, a function of both an aging society and rigid labor markets. [Link; paywall]

Tinseltown

‘The Town Hall of Hollywood.’ Welcome to the Netflix Lobby. by Brooks Barnes (NYT)

Where can you see Dolly Parton, Leo DiCaprio, John Kerry, Cindy Crawford, David Letterman, Beyoncé, President Obama, Alfonso Cuarón, Jay Leno, or studio heads? Waiting to pitch or be pitched by the biggest content budget in LA. [Link; soft paywall]

IPO Flops

Why Budweiser and Bankers Failed to Sell the King of IPOs by Thomas Buckley, Vinicy Chan, Crystal Tse and Bruce Einhorn (Yahoo!/Bloomberg)

Global brewing behemoth AB-InBev was all set to list its APAC businesses in a massive Hong Kong IPO, but the $10bn listing had to be pulled due to lack of investor interest. [Link]

Laugh More, Live Longer

You’re Not Laughing Enough, and That’s No Joke by Pamela Gerloff (Psychology Today)

Toddlers burst out laughing hundreds of times a day, but adults – especially those later in life – are much less frequent to giggle. But laughter reduces stress hormones and releases endorphins which can improve quality of life. [Link]

Long Reads

Apollo 11 Had a Hidden Hero: Software by Robert Lee Hotz (WSJ)

The story of the code behind the moon landing, and how it helped jump-start the role of computers across industries and applications more broadly. [Link; paywall]

A Carolina Dog by Cy Brown (Bitter Southerner)

The fascinating story of a dog breed which has been wandering around North America with and without human companions for the past 14,000+ years, and has rooted itself in the swamps of the rural south. [Link]

Read Bespoke’s most actionable market research by joining Bespoke Premium today! Get started here.

Have a great weekend!

The Bespoke Report — 7/19/19

This week’s Bespoke Report newsletter is now available for members.

In this week’s newsletter, we try and digest market expectations for rate cuts amid strengthening economic data. We also provide a full rundown of this week’s earnings reports and what’s on tap for next week. Three of the four FANG stocks (FB, AMZN, GOOGL) report next week. To read the Bespoke Report and access everything else Bespoke’s research platform has to offer, start a two-week free trial to one of our three membership levels. You won’t be disappointed!

The Closer: End of Week Charts — 7/19/19

Looking for deeper insight on global markets and economics? In tonight’s Closer sent to Bespoke clients, we recap weekly price action in major asset classes, update economic surprise index data for major economies, chart the weekly Commitment of Traders report from the CFTC, and provide our normal nightly update on ETF performance, volume and price movers, and the Bespoke Market Timing Model. We also take a look at the trend in various developed market FX markets.

The Closer is one of our most popular reports, and you can sign up for a free trial below to see it!

See tonight’s Closer by starting a two-week free trial to Bespoke Institutional now!

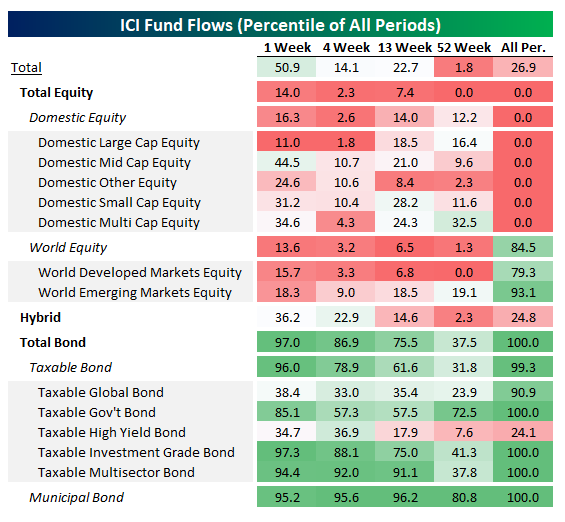

Record Outflows From Equity Mutual Funds

Earlier this week the Investment Company Institute (ICI) released weekly mutual fund flows for the week ending July 10th. Every single category of equity fund flows had outflows this week, which is relatively rare; of the 654 weeks with data since 2007, only 70 have seen that kind of consistency across all equity categories…and four of those have been in the past four weeks! Total equity fund outflows were $46bn this week, versus $6.8bn for the week and $85.4bn over the past three months. On a cumulative basis, $1.2trn has left equity mutual funds since January of 2007. Start a two-week free trial to Bespoke Institutional to access our interactive economic indicators monitor and much more.

With equity fund flows in the bottom quintile of all periods in recent weeks, bond funds have been the complete opposite story. As shown in the table below, bond fund inflows were in the 97th percentile overall this week and in the 94th percentile or higher in four different categories. The only areas that were at all weak were taxable global bonds and high yield bonds. On a cumulative basis, bond fund inflows total $1.7trn since the start of 2007, an interesting mirror image of the $1.7trn in domestic equity fund outflows since 2007.

The bottom line is that equity fund flows have been very large over the past year. As shown in the chart below, more than $320bn has flowed out of equity funds over the past year, more than any other 52-week period in the history of the day. Even at the height of the crisis, investors were pulling substantially less from funds.

B.I.G. Tips – Yield Curve Un-Inverts

Yesterday, the yield curve (spread between yields on 10-year and 3-month US Treasuries) briefly moved into positive territory for the first time since May 23rd and ended a streak of 40 days at inverted levels. While the curve barely moved out of inverted territory (less than one basis point) and is in and out of inversion this morning, positive is positive! As we have mentioned in the past, while it has been a reliable recessionary indicator (sometimes with a lag), an inverted yield curve does not necessarily mean things will immediately turn south for the stock market.

To continue reading this B.I.G. Tips report, start a two-week free trial to Bespoke Premium.

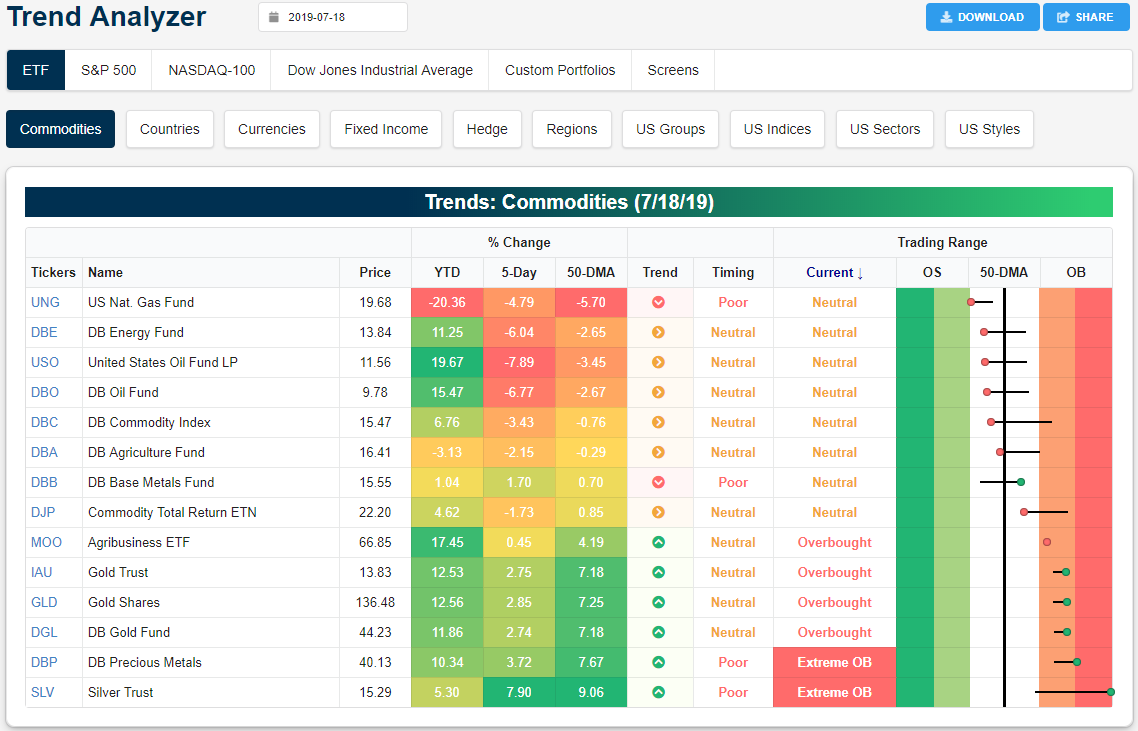

Trend Analyzer – 7/19/19 – Precious Metals Soar

The Dow (DIA) has distanced itself from the other major index ETFs in the past week. While other large-cap ETFs like the S&P 100 (OEF) have dropped 0.23% and the Nasdaq (QQQ) is flat, DIA has managed to rise 0.5%. DIA is also the most overbought of all the major index ETFs, although like other large caps, it is less overbought than it was one week ago. On the other hand, mid-caps like the S&P MidCap 400 (MDY) and the Russell Mid-Cap (IJR) have actually moved higher within their trading ranges on small gains. At their current levels, the S&P MidCap 400 (MDY) and the Core S&P Mid-Cap (IJH) both have good timing scores in our Trend Analyzer.

Equity indices have not managed to see any sort of large move in the past week as each of the fourteen has gained or lost less than 1%. Meanwhile, the commodities space has been much more volatile. In particular, oil (USO) and energy in turn as seen through the DB Energy Fund (DBE) have gotten smashed over the past week. USO is down 7.89%, falling below the 50-DMA and moving towards oversold levels. Similarly, Nat. Gas (UNG) continues this year’s pain falling 4.79% further.

Contrary to the moves in energy markets, precious metals like silver (SLV) have been soaring. After lagging behind gold recently, the Silver Trust (SLV) has finally caught up with the yellow metal. SLV has risen 7.9% over the past week, the best gain of any commodity. Ironically, earlier in the week it was actually negative YTD but these gains over the past five days have brought it to a 5.3% YTD gain. But also with this surge, SLV is now extremely overbought sitting over 2 standard deviations above the 50-DMA. Gold ETFs on the other hand, while not seeing as large of a move, has also done well rising around 2.75%. Precious metals in general as seen through DB Precious Metals (DBP) have become extremely overbought.

Looking at the charts, yesterday’s strong session for precious metals led to a further breakout to 52-week highs across the board. While the DB Precious Metal Fund (DBP) and gold’s break out is above more recent resistance, silver’s 52-week high took out resistance from much earlier in the year. In reaching this new high, SLV’s chart makes it pretty evident as to just how rapid the move has been and the degree to which it is extended to the upside.

Bespoke’s Morning Lineup – Tech Back in Charge

After yesterday’s somewhat strange combination of positive economic data and dovish FOMC commentary, futures are showing continued positive momentum with equities indicating a modestly higher open led by the Nasdaq and Microsoft’s (MSFT) earnings after the close Thursday. The stock is currently up over 3%, further cementing its place in the trillion market cap camp. Treasury yields are modestly higher at the long end of the curve, and the 10-year vs 3-month curve is close to positive territory.

Read today’s Morning Lineup to get caught up on news and stock-specific events ahead of the trading day and a further discussion of recent earnings reports from around the world.

Bespoke Morning Lineup – 7/19/19

Each Thursday in our Sector Snapshots report, we highlight the relative strength of individual sectors versus the S&P 500. One sector that stood out in last night’s update was Technology. While the sector has been a market leader for some time, it has finally erased all of its underperformance from the month of May and is the only sector where relative strength is at a new high.

One contributor to the sector’s strength recently is semiconductors. From its highs in April to the May lows, the Philadelphia Semiconductor Index (SOX) nearly reached bear market territory on an intraday basis falling 19.8%. Since then, the SOX has rallied 18.9%, and while it is still shy of new highs for the year, it did close on Thursday at its highest level since 5/6.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

“We Don’t Need Your Stinking Data”

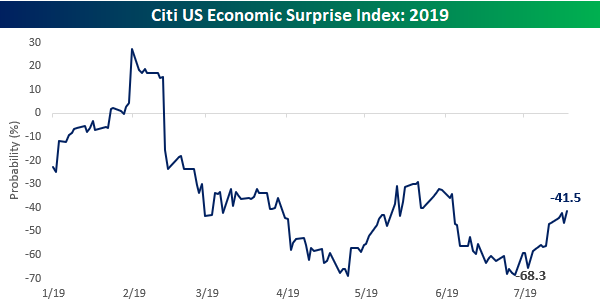

Yesterday was another one of those days that makes you scratch your head. In a relatively busy day for economic data, Initial Jobless Claims came in within 25K of a 50-year low, and the Philly Fed Manufacturing report saw its largest m/m increase in a decade. That follows other data last week where Retail Sales were very strong and CPI and PPI both came in ahead of consensus forecasts. The trend of better than expected data since the June employment report on July 5th is reflected in recent moves of the Citi Economic Surprise Index which has rallied from -68.3 up to -41.5. Granted, it’s still negative, but what was looking like a real dismal backdrop for the economy just three weeks ago seems to be showing signs of improvement.

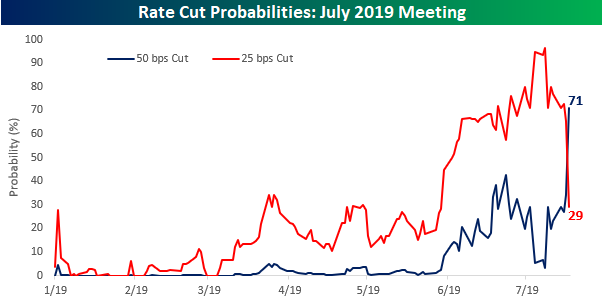

On top of the economic data, two notable interviews from FOMC officials Williams from New York and Vice Chair Clarida moved markets. Given the strong tone of economic data, one would expect both officials to try and tone down rising market expectations regarding any aggressive policy moves at the July meeting. Well, markets don’t always make sense.

In their respective interviews, both Williams and Clarida not only didn’t tone down expectations, but they added fuel to the fire. Williams noted that “it pays to act quickly to lower rates” and “vaccinate” the economy “against further ills.” Clarida was even more direct when he said that “Research shows you act preemptively when you can.” In other words, the data-dependent Fed is casting the data aside and ready to move anyway. In his interview on Fox Business, Clarida almost got a chuckle when asked whether there was any chance the Fed wouldn’t cut rates in July.

The dovish turn from the Fed was immediately reflected in market expectations for rate policy at the July meeting. Back in June, market expectations for a 50 basis points (bps) cut at the next meeting peaked out at under 50%. Then, in the days following the June employment report, expectations dropped all the way down to 3%. In the last ten days, though, the trend has completely reversed, and as of yesterday’s close topped out at 71% versus just a 29% chance for a 25 bps cut. Probabilities for a 50 bps cut came in a bit overnight but are still at about 50/50. Yesterday alone, though, expectations for a 25 bps cut and a 50 bps cut more than completely reversed from the prior day, and remember, that’s after what was a good day of economic data! Can you imagine what expectations would be like if the data was actually bad? Become a Bespoke Premium member today with a two-week free trial.

The Closer – Consumer Cruising, Silver Flying, Leading Index, Five Fed – 7/18/19

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, in the face of more talks of rate cuts by Fed officials today, we show the strength of the consumer in addition to the strength of silver in recent trading. Next, we look at the only notably weak data point released today: the leading index. After today’s strong Philly Fed Manufacturing Activity Index, we provide an update to our Five Fed Manufacturing Composite.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!