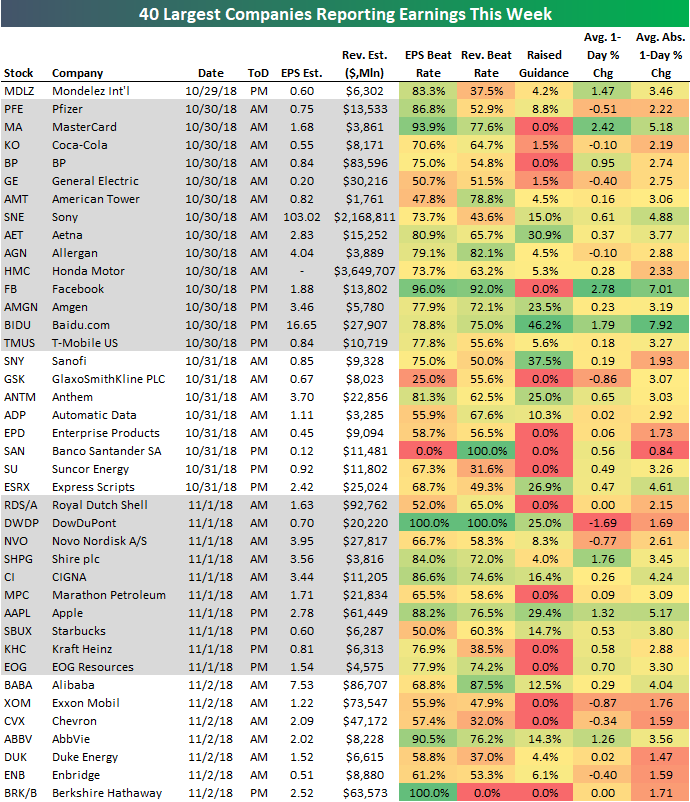

Most Important Earnings to Watch This Week

We’re smack dab in the middle of earnings season right now, and below is a list of the 40 largest companies set to report Q3 numbers this week. For each stock, we include a number of key data points that you won’t find in most earnings calendars. Data points like historical earnings and revenue beat rates, the percentage of the time that the company has raised guidance, and the stock’s average one-day price change in reaction to earnings are all included in the table after pulling them from our popular Earnings Screener tool.

After a slow Monday, we get a number of big reports on Tuesday from the likes of MasterCard (MA), Coca-Cola (KO), General Electric (GE), Facebook (FB), and Baidu (BIDU). Wednesday is relatively slow as well, but Thursday makes up for it with Apple’s (AAPL) release after the close. On Friday, we’ll hear from big oil companies Chevron (CVX) and Exxon Mobil (XOM) as well as the “Amazon of China” — Alibaba (BABA).

Of the stocks on the list, MasterCard (MA), Facebook (FB), and Apple (AAPL) have some of the strongest earnings and revenue beat rates, while Baidu (BIDU) has raised guidance the most. In terms of stock price reaction to earnings, Facebook (FB) and MasterCard (MA) show up again with average one-day gains of more than 2% when they have reported earnings throughout their history. Exxon (XOM), Chevron (CVX), General Electric (GE), and Pfizer (PFE) are four stocks that have historically averaged declines on their earnings reaction days.

Stay on top of everything earnings-related with a Bespoke Institutional membership. Start a two-week free trial to gain access now!

Morning Lineup – Big Blue’s Big Buy

US stock futures are higher this morning giving hope to the idea that last week’s sell-off may have run its course. The Nasdaq is leading the way higher as tech stocks outperform on news of IBM’s purchase of Red Hat (RHT) for more than a 50% premium over Friday’s closing price. The $190 cash offer is also $13 above RHT’s all-time high of $177 earlier this year. In international news, politics is dominating the headlines with important election results in Germany and Brazil.

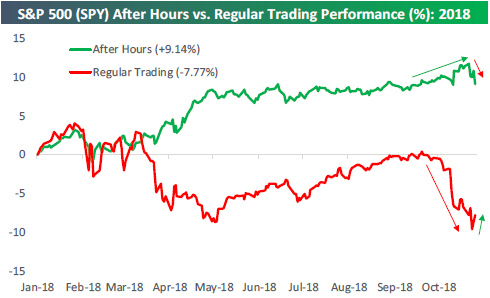

The S&P 500 is set to open over 1% higher this morning, which represents just a continuation of this year’s trend where virtually all of the equity market’s strength has taken place outside of regular trading hours. As highlighted in this week’s Bespoke Report, normally during pullbacks we’ll see a number of big gaps down at the open of trading due to negative news events that occurred either after the prior day’s close or ahead of the open that morning. During this sell-off, though, there has actually been a lack of specific news events that investors can point to and say “that’s the reason everything is down.” These types of sell-offs that can’t be tied to any one specific event are the scariest ones because it suggests that the market knows something that we (as in, we, investors) don’t know.

As shown, below, had you bought SPY at the close every trading day this year and sold it at the next open, you’d still be up 9.14% this year (and another 1% today!). Had you only bought SPY at the open every trading day and sold it at the close, you’d be down 7.77%! Over the last month or so as the market has collapsed, the intraday selling has been extreme, to say the least. Earlier this week we noted that 70% of the time that the market has been open over the last three weeks, it has been down, which is not seen very often. The key test for the market today will be whether it can finally hang on to early strength for a change.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Bespoke Brunch Reads: 10/28/18

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, try a two-week free trial to Bespoke’s premium stock market research!

Science

Redrawing the Map: How the World’s Climate Zones Are Shifting by Nicola Jones (Yale Environment 360)

A review of shifting boundaries for temperate or fertile regions around the world. Some of the shift is driven by our own impact on the broader climate through fossil fuel emissions and other factors but those aren’t the only reasons that arid regions are expanding. [Link]

Toxin or treatment? by Jennifer Couzin-Frankel (Science)

New treatments for extreme allergies are focused on gradually exposing children to very small amounts of allergen, gradually ramping up doses to build a tolerance and cure their allergy. [Link]

History

Joachim Ronneberg: Norwegian who thwarted Nazi nuclear plan dies (BBC)

In 1943 a daring team of saboteurs orchestrated the most under-appreciated mission of the Second World War, blowing up a key Nazi installation that could have allowed progress on a nuclear bomb. Its last member and a long-time advocate of peace has died. [Link]

Weird News

The Unsolved Murder of An Unusual Billionaire (Boomberg)

A penetrating investigation of the death of one of Canada’s richest men, whose philanthropy and idiosyncrasies drew attention but nothing even approaching the ire that could motivate his murder and that of his wife. [Link; soft paywall]

Disney World’s Big Secret: It’s a Favorite Spot to Scatter Family Ashes by Erich Schwartzel (WSJ)

Roughly once per month, guests scatter the ashes of loved ones somewhere in Walt Disney World or Disneyland, in a combination of touching gesture and extremely weird tie-in of consumerism to last rites. [Link; paywall]

Flops

This Bank Lost 50% Of Its Value And Taught Us All A Lesson We Forgot by The Dividend Guy (Seeking Alpha)

We talked about Bank OZK last week, but this write-up is a nice summary with investing lessons in addition to the specific facts related to portfolio write-downs at the bank. [Link]

Auto dealers see slowing sales, sparking fears that a long-expected decline is here by Phil LeBeau (CNBC)

Auto dealers are reporting slowing traffic and declines in business amidst higher interest rates, though declines in volumes are not uniform by any means. [Link]

Business Models

Apple News’s Radical Approach: Humans Over Machines by Jack Nicas (NYT)

A look at how Apple News aggregates its top stories each day, and an even closer look at Apple News’s business model and its ungodly 30% rake. [Link; soft paywall]

Uber’s Secret Restaurant Empire by Kate Krader (Bloomberg)

Because Uber Eats restaurants don’t need a storefront, they’re creating opportunities for businesses within businesses or other unusual firm arrangements. [Link; soft paywall]

This Thermometer Tells Your Temperature, Then Tells Firms Where to Advertise by Sapna Maheshwari (NYT)

Your thermometer may be feeding the fact that you’re sick to companies that want to sell you bleach, one of the major downsides to internet-connected devices. [Link; soft paywall]

Saving money should be easy. Automate it with Trim. (Trim)

This start up is trying to do the tough work of negotiating with companies for you, saving consumers hundreds of dollars on their bills for cable or cell phones. [Link]

Credit

New Type of Credit Score Aims to Widen Pool of Borrowers by Ann Carrns (NYT)

The creator of FICO credit ratings is testing a way to ultimately let more consumers borrow big money. Have they not seen the housing data lately?? [Link; soft paywall]

Crypto

Coinbase and Circle announce the launch of USDC — a Digital Dollar (Coinbase)

Crypto exchange Coinbase and payments company circle are launching a fully-collateralized USD-linked stablecoin tied to the value of the US dollar. [Link]

Autism

500,000 teens with autism will become adults in next 10 years. Where will they work? by Suzanne Garofalo (Houston Chronicle)

Autism diagnosis rates have surged, and there are hundreds of thousands of young people on the spectrum who could benefit from the social and developmental challenges of employment, but training them is challenging and requires a very different approach from employers. At the same time, business could benefit from either direct hiring or public-private partnerships seeking to place folks with autism in either internships or full time employment. [Link]

Intellectual Property

Copyright Office Ruling Issues Sweeping Right to Repair Reforms by Kyle Wiens (iFixIt)

Some background on a ruling by the US patent office that gives consumers the right to jailbreak voice assistant devices, unlock new phones, repair smartphones, home appliances, and home systems, and repair motorized land vehicles including tractors by changing their software. None of this had been permitted explicitly prior to the ruling this week. [Link]

AI

Generating custom photo-realistic faces using AI by Saobo Guan (Insight Data Science)

An interesting tool that can change someone’s facial features using a few specific metrics while not making them look unrealistic. [Link]

Read Bespoke’s most actionable market research by starting a two-week free trial today! Get started here.

Have a great Sunday!

2018 Week 8

Week 7 Results: 11-2, Overall: 55-40 (61.1%)

Outside of financial markets, we’re also sports fans here at Bespoke. With new legal sports betting avenues now available across the US, we figured we’d have some fun and pick each NFL game versus the spread this season (as of Saturday evening). Let’s see how we do…on to Week 8.

We were 11-2 in week 7, bringing our overall record through 7 weeks to 55-40 (61.1%).

2018 NFL Week 8 Bespoke Picks:

Philadelphia (-3) at Jacksonville (in London): Jacksonville +3

NY Jets at Chicago (-9.5): NY Jets +9.5

Tampa Bay at Cincinnati (-3.5): Tampa Bay +3.5

Seattle at Detroit (-3): Seattle +3

Denver at Kansas City (-9.5): Kansas City -9.5

Washington (-1) at NY Giants: NY Giants +1

Cleveland at Pittsburgh (-8): Cleveland +8

Baltimore (-2.5) at Carolina: Carolina +2.5

Indianapolis (-3) at Oakland: Indianapolis -3

Green Bay at LA Rams (-8): Green Bay +8

San Francisco (-1.5) at Arizona: Arizona +1.5

New Orleans (-1.5) at Minnesota: Minnesota +1.5

New England (-13.5) at Buffalo: New England -13.5

2018 NFL Week 7 Bespoke Results:

Tennessee at LA Chargers (-7): Tennessee +7 Win

New England (-3) at Chicago: Chicago +3 Loss

Buffalo at Indianapolis (-7.5): Indianapolis -7.5 Win

Detroit (-3) at Miami: Miami +3 Loss

Minnesota (-3.5) at NY Jets: Minnesota -3.5 Win

Carolina at Philadelphia (-4.5): Carolina +4.5 Win

Cleveland at Tampa Bay (-3.5): Cleveland +3.5 Win

Houston at Jacksonville (-4): Houston +4 Win

New Orleans at Baltimore (-2.5): New Orleans +2.5 Win

LA Rams (-9.5) at San Francisco: LA Rams -9.5 Win

Dallas at Washington (Even): Washington Even Win

Cincinnati at Kansas City (-6): Kansas City -6 Win

NY Giants at Atlanta (-4): NY Giants +4 Win

The Bespoke Report — Earnings Season Hits Stocks Hard

The Closer: End of Week Charts — 10/26/18

Looking for deeper insight on global markets and economics? In tonight’s Closer sent to Bespoke clients, we recap weekly price action in major asset classes, update economic surprise index data for major economies, chart the weekly Commitment of Traders report from the CFTC, and provide our normal nightly update on ETF performance, volume and price movers, and the Bespoke Market Timing Model. We also take a look at the trend in various developed market FX markets.

Below is a snapshot from today’s Closer highlighting positioning of speculators in interest rate futures. If you’d like to see more, start a free trial below.

The Closer is one of our most popular reports, and you can sign up for a free trial below to see it!

See tonight’s Closer by starting a two-week free trial to Bespoke Institutional now!

Morning Lineup – That Was Fast

It seems like longer ago now, but it was just on Monday that everyone was focused on the big 4% rally in China and how that could have marked the bottom indicating some stability for the global financial markets. As we noted at the time, big up moves typically occur in weak overall market environments, and sure enough, the next day, Chinese equities gave up more than half of Monday’s gain and global markets continued to sink

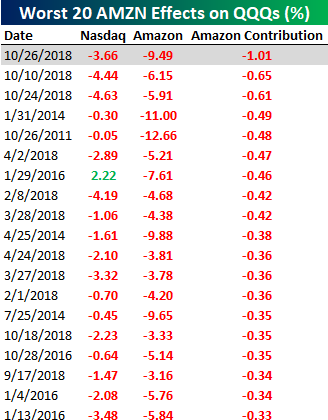

Yesterday, it was our turn to rally, but before the closing trades had even settled and before anyone even had the chance to ask if that move marked a low, Amazon (AMZN), Alphabet (GOOGL), and some other high profile tech stocks issued poor earnings reports sending the QQQs sharply lower. As things currently stand now, QQQ is set to open lower than Wednesday’s close, erasing all of Thursday’s gains! Just plain brutal.

With AMZN trading down over 9%, it is set to have a massive negative impact on the Nasdaq 100 this morning. Of the QQQ’s indicated decline of 3.66% at the open, 28% of the entire drop is due to AMZN. As shown in the table below, never in the stock’s history has it had such a large one-day negative impact on the performance of the Nasdaq 100. When you add in the fact that Alphabet (GOOGL) is trading down over 5%, these two stocks are accounting for about 40% of the Nasdaq 100’s entire decline today.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Trend Analyzer – 10/26/18 – Small and Mid Caps Continue to Lag

Even after huge rallies of nearly 2% for SPY and DIA yesterday and a gain of 3.5% for QQQ, every US index ETF that we track in our Trend Analyzer remains oversold. Given where futures are trading ahead of today’s open, things are set to get a lot more oversold at 9:30 AM ET.

While the overall picture has been less than optimistic, weakness in the major index ETFs focused on small to mid caps has been downright terrible. These ETFs have lagged behind the rest of the market considerably. At the current moment, each one of these names are down year-to-date and have entered into downtrends. With gains yesterday, some other ETFs such as the Core S&P Small-Cap (IJR) and the Russell (IWB) were able to move back to positive returns on the year, but with futures indicating a lower open today, this should not be expected to hold.

On a sector basis, Consumer Staples (XLP), Real Estate (XLRE), and Utilities (XLU) are the only ones to have thrived over the past week. XLP and XLRE are in oversold territory but are still down on the year. The Energy sector on the other hand (XLE) is down big this week at 7.19%. This month has not done any favors for the materials sector (XLB) either as it is now down big 14.35% YTD.

The Closer — Market Observations, Manufacturing, Trade — 10/25/18

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, we look at some notable price action in Ford (F) and the Nasdaq 100 means for stocks going forward. We also review the pickup in earnings reactions, price action in the ten year yield, and the relative performance of Exploration & Production names versus WTI. We then take a look at economic data: durable goods, our Five Fed manufacturing activity index, and advance trade data from the US Census.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

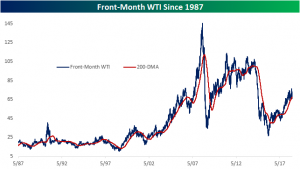

Future of Oil Is A Coinflip

Earlier this week, oil prices did something they have only done a couple times in the past. After spending 262 consecutive trading days above the 200-DMA, oil closed below this average. Similar streaks of more than a year (254 trading days) above the 200-DMA has only happened two other times in the past 3 decades. The first occurrence was on April 10, 2000 ending a 272 day streak, and the second was back on September 2, 2008 when a 330 day streak came to a close.

As you can see in the chart below, it is basically a coin flip to see what will happen now. In 2000, oil managed positive returns over the course of the following year. But the opposite happened in 2008. The year following a move below the 200-DMA saw consistent declines. Of course, keep in mind that oil prices were nearly twice as high in the summer of 2008 and the economy and financial markets were melting down until Q2 2009 at the least, meaning a repeat of the 2008 declines looks pretty unlikely today. Only time will tell which scenario the current one will more closely resemble.