B.I.G. Tips – Death by Amazon – 1/31/19

Our “Death By Amazon” index was created many years ago to provide investors with a list of retailers we view as vulnerable to competition from e-commerce. In 2016, we also created our “Amazon Survivors” index which is made up of companies that look more capable of dealing with the threat from online shopping. To see how the two indices have been performing lately and view the full list of stocks that make up the indices, please read our newest report on the subject available to Bespoke Premium and Bespoke Institutional members.

To unlock our “Death By Amazon” and “Amazon Survivors” indices, login or start a two-week free trial to either Bespoke Premium or Bespoke Institutional.

Chart of the Day – February Intra-Month Performance

In today’s Chart of the Day available to Bespoke subscribers, we look at the historical performance of the S&P 500 during the month of February and its intra-month pattern going back to 1985. One interesting trend is how much January performance tends to impact February performance. To see the report, start a two-week free trial to any Bespoke membership level.

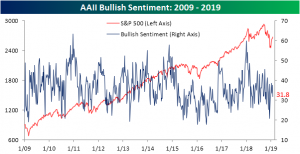

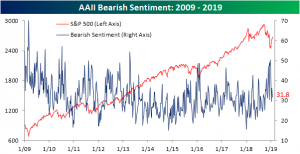

Bulls and Bears Get Even

Sentiment as seen through the AAII survey of individual investors was split evenly between the bulls and bears this week. After a week of the S&P 500 largely meandering sideways—with the exception of the surge yesterday—bullish sentiment dropped to 31.76% from 37.66% the prior week. While this drop is nothing substantial, bullish sentiment still sits firmly below the historical average of 38.5%.

Bearish sentiment is dead even with bullish sentiment at 31.76%. That is slightly down from 32.32% last week. Since peaking in the first week of 2019, bearish sentiment has stayed within a low to mid 30% range. This week’s reading is at the lower end of that range for this year. Unlike bullish sentiment and in spite of the post-Christmas rally, this is actually still slightly above the historical average for bearish sentiment.

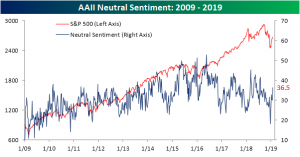

Meanwhile, neutral sentiment ticked up this week to the highest level since the first week of August of last year at 36.5%. Given these readings, investors seem to be increasingly cautious of the current rally. Although—as is the case following any Fed Day—we will have to wait until next week’s data to see the full impact of the Fed’s shift in tone and the subsequent market reaction to their meeting yesterday. The more dovish stance could help to boost bullish sentiment once again. It is also possible that neutral sentiment could drop back to more normal levels given increased clarity on the policy front.

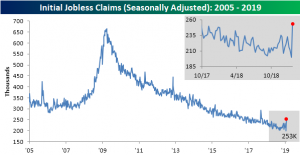

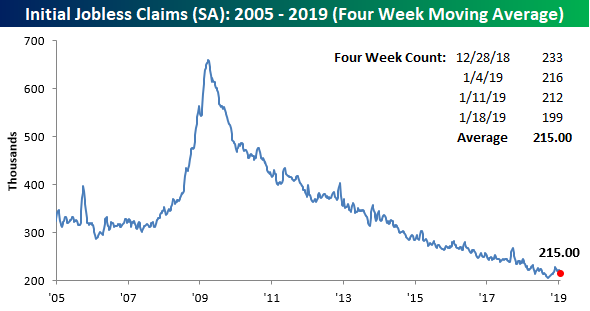

The Streak Ends for Jobless Claims

This morning’s release of Initial Jobless Claims seems to have made an about-face from the impressively strong reading of 199K seen last week. On a seasonally adjusted basis, claims for this week not only went back above 200K but skyrocketed all the way to 253K; their highest level since September 2017. This week’s number also far surpasses the recent jumps seen in October and November of last year when they rose to around 230K. This spike in claims brings an end to the streak of 68 weeks with the seasonally adjusted number coming in below 250K. That was the longest streak since the 89-week streak that ended in January of 1970. Granted, the indicator still has 47K of insurance in its streak of remaining under 300K. That streak is now at 204 weeks long, so while this week’s data raises an eyebrow, it still maintains a healthy level.

Give the large spike in claims, the four-week moving average also rose with a 5K uptick this week to 220.25K. That is right back in line to where the moving average was back in November and December. With the large reading from this week staying in as an input to the average, it will likely remain somewhat elevated for the time being.

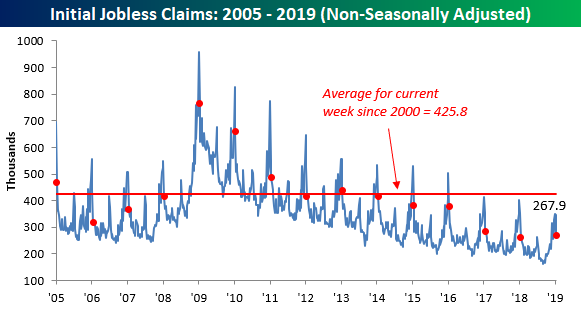

Turning to the non-seasonally adjusted (NSA) data, believe it or not, claims actually fell by almost 20K. The NSA number for this week was 250.2K versus 269.8K last week. Once again, that is well below the average for the current week since 2000 and the lowest reading for the current week in that same timeframe. While the seasonally adjusted number may have come in exceptionally high, labor markets still seem healthy through this non-seasonally adjusted number. The large divergence between the SA and NSA data could very well come as a result of certain quirks in the SA calculations. Also important to note, the government shutdown should not play too large of a role in these readings as government workers are supposed to apply for jobless benefits through other programs, meaning they would more than likely not be counted in these initial jobless claims numbers (although contractors impacted by the shutdown may have started to show in the numbers)

Morning Lineup – Jobless Claims Surge

After the FOMC came through in a big way for the bulls yesterday, equity futures are quiet this morning. Over in the Nasdaq, things are looking brighter as an 11% rally in Facebook (FB) following its earnings report last night has the stock on pace for its best earnings reaction day in three years! In more global macro data, the President is busy on Twitter this morning discussing the topic of Chinese trade and saying that no deal will be made until he personally meets with Chinese President Xi in the “near future.” Jobless Claims were just released and saying they surged would be an understatement, as they rose from 200K up to 253K, the highest weekly reading since September 2017! Read today’s Bespoke Morning Lineup for more on what’s driving the markets this morning.

Bespoke Morning Lineup – 1/31/19

It wasn’t long ago that the market would seemingly go months on end without a daily move of 1% let alone 2%. With the help of the Fed’s dovish turn yesterday, though, the Nasdaq rallied over 2%, making it the 24th time in the last 100 trading days that the index moved up or down 2% in a single day. That works out to an average of more than once a week!

The chart below shows the historical 100-day rolling total of occurrences where the Nasdaq saw an up or down move of 2%+. The current level of 24 is now the highest total we have seen since early 2012, and only the fourth such period in the index’s history. Granted, the period in the late 1990s/early 2000s lasted a long time and saw a much higher frequency of 2% at its most extreme points, but these periods of large day to day moves are still relatively uncommon. Just as interesting is how the period from 1972 through the mid-1990s saw so little in the way of big daily moves. But once the late 1990s rolled around, the beast was awoken.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Chart of the Day: Big Fed Up Days

In today’s Chart of the Day available to Bespoke subscribers, we look at the historical performance of the S&P 500 in the days and weeks after the index experiences a gain of more than 1% on Fed Days. With the S&P 500 trading up 1.5% with 30 minutes left in the trading day, it’s looking like this analysis will be very applicable after the close. To see how the market performs after big Fed up days, start a two-week free trial to any Bespoke membership level.

Fixed Income Weekly – 1/30/19

Searching for ways to better understand the fixed income space or looking for actionable ideals in this asset class? Bespoke’s Fixed Income Weekly provides an update on rates and credit every Wednesday. We start off with a fresh piece of analysis driven by what’s in the headlines or driving the market in a given week. We then provide charts of how US Treasury futures and rates are trading, before moving on to a summary of recent fixed income ETF performance, short-term interest rates including money market funds, and a trade idea. We summarize changes and recent developments for a variety of yield curves (UST, bund, Eurodollar, US breakeven inflation and Bespoke’s Global Yield Curve) before finishing with a review of recent UST yield curve changes, spread changes for major credit products and international bonds, and 1 year return profiles for a cross section of the fixed income world.

In this week’s report we return to STIRs markets.

Our Fixed Income Weekly helps investors stay on top of fixed income markets and gain new perspective on the developments in interest rates. You can sign up for a Bespoke research trial below to see this week’s report and everything else Bespoke publishes free for the next two weeks!

Click here and start a 14-day free trial to Bespoke Institutional to see our newest Fixed Income Weekly now!

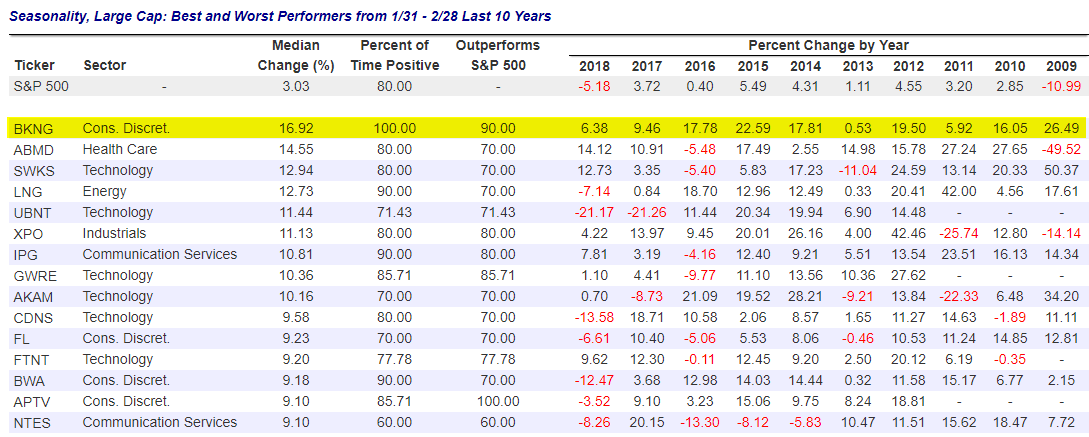

Booking (BKNG) Beats

Seasonality is very much on the side of Booking Holdings (BKNG), formerly known as Priceline.com, heading into February. Using our Seasonality Tool, below is a list of the large-cap stocks that have performed the best during the month of February over the last 10 years. At the top of the list is BKNG with a median gain of 16.92%! Going back to 2009, BKNG has been up during the month of February every single year.

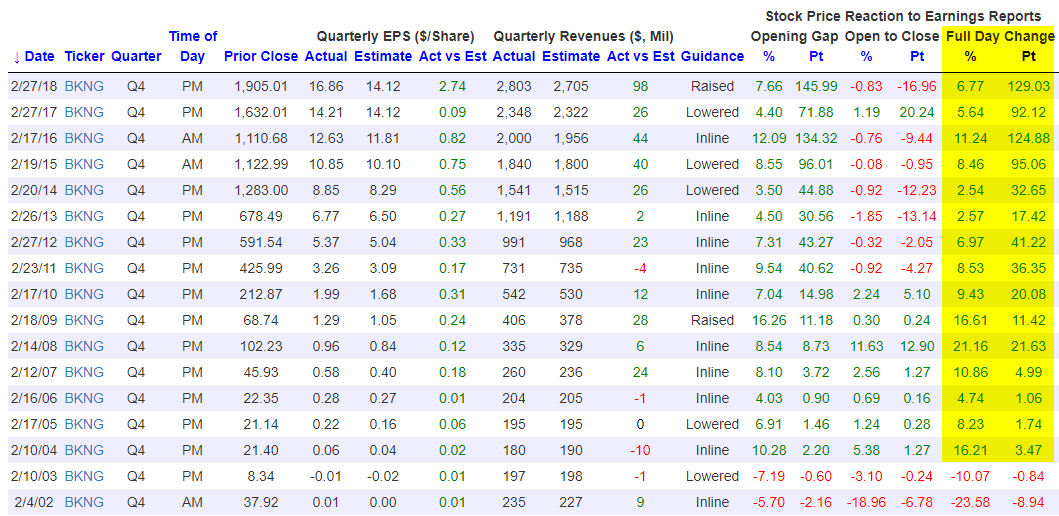

Using our Earnings Screener, it becomes evident why February has been so positive for BKNG as its Q4 earnings report plays a large roll in its February gains. For 15 straight years, BKNG has posted a gain on its Q4 earnings reaction day in February. That’s an incredible streak! Last February, BKNG gained 6.77% on its earnings reaction day, while it gained 5.64% the year before that. The last time BKNG declined on earnings when it reported in February was back in 2003. Below is a snapshot highlighting BKNG’s Q4 earnings reports since 2002. We’ve shaded the stock’s streak of positive February earnings reactions in yellow.

Trend Analyzer – 1/30/19 – Mid-Caps Surge

Despite some minor declines yesterday in the S&P 500 and the Nasdaq, every index ETF has held above their 50-DMA and are still sitting in a neutral range. The large-cap S&P 100 (OEF) and Nasdaq (QQQ) are now the only index ETFs that are down from their levels one week ago. Mid-caps, on the other hand, have continued to rally. The Russell Mid-Cap (IWR) has gained the most at 1.61% over the past week and is very close to overbought territory. Just a little more upwards movement today could easily place the ETF into this range. While more firmly in neutral, the Core S&P Mid-Cap (IJH) and S&P 400 Mid-Cap (MDY) are both up just under 1.5% over the past five days. Additionally, these two are now the best performers on the year (MDY is tied with the IWM for second place).

Morning Lineup – Futures Fly on Boeing

Big earnings from Apple (AAPL) last night after the close and Boeing (BA) this morning have pushed the Dow futures sharply higher. While the gains aren’t as large in the S&P 500 and Nasdaq, they are also both pointing in the right direction for bulls. Now, all we have to do is get through this afternoon’s rate decision from the FOMC and the subsequent press conference. The number one wish from the bulls for Fed Chair Powell? Stick to the script and end the record streak of declines on FOMC days since he became the Chair! Read today’s Bespoke Morning Lineup for more on what’s driving the markets this morning.

Bespoke Morning Lineup – 1/30/19

Even as the equity market has recovered in January, the percentage of consumers who are bullish on the market declined to 30.9%, which is the lowest reading since July 2016. Even more extreme, the percentage of consumers who are negative on stock prices increased to 38.6%, which is the highest reading since December 2012!

Like a lot of sentiment measures, this reading from the Consumer Confidence report also tends to be contrarian in nature. The last time the spread was this skewed to the bearish side was in February 2016, and if you don’t remember, that was right around the lows of the 2015/2016 market correction.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.