Bespoke Brunch Reads: 10/6/19

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, join Bespoke Premium for 3 months for just $95 with our 2019 Annual Outlook special offer.

Red Meat

Eat Less Red Meat, Scientists Said. Now Some Believe That Was Bad Advice. by Gina Kolata (NYT)

The latest in a long back-and-forth debate over nutritional science and the right amount of red meat to eat, with a side of internecine scientific fighting. [Link; soft paywall]

Are Burgers Really That Bad for the Climate? by Justin Fox (Bloomberg)

How much carbon does your burger habit cost? It turns out the answer is a little bit complicated, and highly sensitive to the various assumptions that get made. [Link; soft paywall]

New York Real Estate

New York City Apartment Prices Hit Four-Year Low by Josh Barbanel (WSJ)

The median sales price for apartments in New York fell 32% in the third quarter, driven by an increase in transfer taxes for higher-end units that came into effect in July. [Link; paywall]

NYC housing prices in near ‘free fall,’ conditions mirror recession era following tax hikes by Brittany De Lea (Fox 5 New York)

The increase in the New York City “mansion tax” moved the maximum taxable rate up to 3.9% from 1%; tax amounts increase as sales prices do over $1mm. That relatively small tax change appears to have driven a massive price response, at least so far as QoQ data goes. [Link]

The Middle Class

The Middle-Class Crunch: A Look at 4 Family Budgets by Tara Siegel Bernard and Karl Russell (NYT)

A view at a range of middle class families with monthly take-homes ranging from $48k-$116k. Note: median family income in 2018 was $63k. [Link; soft paywall]

The Seven-Year Auto Loan: America’s Middle Class Can’t Afford Its Cars by Ben Eisen and Adrienne Roberts (WSJ)

Longer amortizations have come to the US auto market, meaning a more manageable monthly payment…but longer repayment and more risk. [Link; paywall]

Food For Thought

How billionaire Ray Dalio helped launch McDonald’s Chicken McNugget by Emmie Martin (CNBC)

Did you know that the Chicken McNugget wouldn’t exist without the founder of Bridgewater Associates? By matching buyer demand and seller supply, the hedge fund manager allowed for the mass market in fried, boneless poultry nuggets. [Link]

Biggest U.S. Egg Producer Plunges as Supplies Soar and Prices Drop by Lydia Mulvany (Bloomberg)

Egg producers are switching to cage-free varieties, but as customers switch to the more hen-friendly varieties, there hasn’t been any decline in traditional types of eggs. [Link; soft paywall]

Private Markets

Everything Is Private Equity Now (Bloomberg)

Outside ownership by a fund that has experience bringing operations into a more efficient place can be good for businesses and the economy, but like any medicine too much of a good thing is a problem. [Link; soft paywall]

All Revenue is Not Created Equal: The Keys to the 10X Revenue Club by Bill Gurley (Above the Crowd)

This relatively straightforward checklist gives a rundown of when a business is likely to be worth 10x its revenues and when it isn’t. [Link]

The Great Public Market Reckoning by Fred Wilson (AVC)

Is all of the chaos in the transition from private markets to public markets for VC-backed investments simply a question of margins? [Link]

Internet Stuff

Remember Wrinkles the Clown, the viral boogeyman for hire? This new documentary shows his dark side by KC Ifeanyi (Fast Company)

A strange video went viral, as part of a marketing stunt for a very creepy clown that was offering a strange service to parents. But there’s even more weirdness to this uniquely Florida story. [Link]

Fat Bear Week Is Back by Brian Kahn (Gizmodo)

For bears, pigging out over the summer isn’t a function of gluttony, but pure survival. Ursine eaters are in the process of hitting their peak weights, ready to hibernate through the winter, and Katmai National Park and Preserve is keeping track of which predator packs on the pounds best. [Link]

Closing Time

Why are Rural Hospitals Closing? By Emily Wavering Corcoran (Federal Reserve Bank of Richmond)

An investigation into the 155 rural hospitals that have shut their doors over the last 15 years, concentrated in large states and those that did not expand Medicaid with the ACA. [Link]

As Steelmaker Shuts Plant, Governor Points to Tariffs by Jeremy Hill (Bloomberg)

A Louisiana recycled steel operation filed bankruptcy after shutting down its operations this week. The company uses imported scrap metal to make its products, which has left it badly exposed to tariffs on steel imports. [Link; soft paywall]

Autonomous Vehicles

Waymo Valuation Slashed on Autonomous Vehicle Tech Delays by Gerrit De Vynck (Bloomberg)

A private valuation of the Waymo division of Google has been cut from $175bn to $105bn thanks to “a series of hurdles relating to commercialization and advancement”. [Link; soft paywall]

Fixed Income

Why the U.S. Yield Curve Reliably Predicts U.S. Recessions by Richard M. Salsman (AIER)

A very basic walk-through of the logic behind yield curve inversion and its forecasting power in the US economy. [Link]

Investing

Charles Schwab on the Lessons He’s Learned Over a Lifetime of Investing by Robert Hackett (Fortune)

A profile on the discount brokerage legend, who has led the charge in democratizing the financial markets for discount brokerage clients. [Link]

Central Banking

The education of Jerome Powell: How the Fed chair is adapting to pressure from Wall Street and Trump by Heather Long and Tory Newmyer (WaPo)

As Chair Powell has gotten more press conferences under his belt, he’s worked hard to improve his communication style and avoid some of the past mistakes he’s made. [Link]

Early French and German central bank charters and regulations by Ulrich Bindseil (ECB Occasional Paper Series)

Some original scholarship that provides translations and analysis of six early central bank charters and related regulations for early European central banks. [Link; 94 page PDF]

‘Keep de Rates dem Low’—Jamaica Sets Inflation Fight to Reggae Beat by Robbie Whelan (WSJ)

Reggae is the latest weapon deployed by the Bank of Jamaica in its fight against inflation, a unique approach to public education. [Link; paywall]

Read Bespoke’s most actionable market research by joining Bespoke Premium today! Get started here.

Have a great weekend!

Bespoke 2020 Special

Bespoke Investment Group has been providing investors with clear, actionable analysis since our founding in 2007, and we’re currently working hard on our biggest and most important report of the year — The Bespoke Report 2020 Market Outlook and Investor Toolkit.

It’s not hard to describe the contents of this report because it simply has it all. This report prepares you with everything you need to know for the year ahead, and it’s a must-read for all investors.

How can you gain access to our annual Bespoke Report? It’s easy. Join one of our three membership levels now with our “2020” special offer and the report is included. What is the “2020” special? You’ll get one month of any membership level for just $20, then you’ll get 20% off the regular monthly rate going forward. Join now because this special is only available for a limited time! Choose an option below to sign up now. Click here if you’re looking for more details on what’s included with each membership level.

Bespoke 2020 Special — Bespoke Newsletter

Bespoke 2020 Special — Bespoke Premium

Bespoke 2020 Special — Bespoke Institutional

The Bespoke Report — 10/4/19

This week’s Bespoke Report newsletter is now available for members.

Stocks bounced big late in the week after the details of the Employment Situation Report helped a bid in equities that started Thursday. Big drops in equity markets in response to ISM numbers early in the week were mostly clawed back. So which should matter more, the soft ISM surveys or the hard data on jobs? We give a definitive answer, as well as discussing a range of other economic and market details. To read the Bespoke Report and access everything else Bespoke’s research platform has to offer, start a two-week free trial to one of our three membership levels. You won’t be disappointed!

The Closer: End of Week Charts — 10/4/19

Looking for deeper insight on global markets and economics? In tonight’s Closer sent to Bespoke clients, we recap weekly price action in major asset classes, update economic surprise index data for major economies, chart the weekly Commitment of Traders report from the CFTC, and provide our normal nightly update on ETF performance, volume and price movers, and the Bespoke Market Timing Model. We also take a look at the trend in various developed market FX markets.

The Closer is one of our most popular reports, and you can sign up for a free trial below to see it!

See tonight’s Closer by starting a two-week free trial to Bespoke Institutional now!

Next Week’s Economic Indicators – 10/4/19

All-in-all, it was a pretty mixed week for economic data, specifically manufacturing and labor data. While Markit’s gauge on manufacturing was slightly stronger than both expectations and the August print, ISM’s version disappointed with little in the way of bright spots among its components. Hard data, on the other hand, is showing a bit of a different picture as Durable Goods appear healthy with the fastest 3m/3m growth rate since last November as we discussed in Thursday’s Closer. The Markit Services PMI and ISM’s Non-Manufacturing Index were also split with Markit’s reading holding steady as ISM disappointed once again. Employment data was the other major focus of the week with similar disappointments, but some silver linings. Ahead of Friday’s Nonfarm Payrolls Report, ISM’s Employment components for both the Manufacturing and Services sectors further weakened in September while this week’s initial jobless claims rose slightly more than expected (although continuing claims fell again). ADP’s reading on employment also fell more than expected. The NFP report followed suit showing fewer jobs added in September, but new lows in the unemployment rate and underemployment rate added to the case of continued labor market strength.

Economic data takes a bit of a breather next week with only two-thirds as many releases this week. Consumer credit is first up on the docket and is expected to moderate to $15 billion after a very strong print last time around. On Tuesday, we will get confidence numbers out of the small business world. NFIB’s Small Business Optimism is forecasted to fall to 102.5 from 103.1 in August. PPI is also out that morning, although no change is expected for both the headline and core numbers. CPI data is due to be released later in the week on Thursday and likewise, no change is expected. Further in inflation data, on Friday, import and export price indices are also scheduled to be released. In labor data, the Job Openings and Labor Turnover Survey (JOLTS) will come out on Wednesday followed by weekly claims numbers the following day. After rising to 219K this week, claims are expected to improve to 217K. Finally, Friday’s preliminary University of Michigan Sentiment for October will round out the week. It is expected to fall to 92.0 after last month’s rebound up to 93.2. Start a two-week free trial to Bespoke Institutional to access our interactive economic indicators monitor and much more.

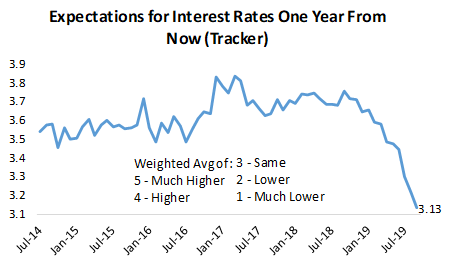

Contrarian Takeaways From Our Monthly Consumer Pulse Survey

Each month Bespoke runs a comprehensive survey on the US consumer, giving us proprietary insights in nearly real-time to the major driver of the US economy. We ask dozens and dozens of questions related to every area of the economy, and we also ask about feelings towards financial markets. One of the questions we ask survey participants is where they think interest rates will be one year from now. Below is a chart showing the monthly reading for this question over the last five years.

When the line is falling, it means consumers expect interest rates to be lower, while a rising line means consumers think interest rates will be higher. As shown, expectations have fallen off a cliff this year as actual interest rates have collapsed, meaning consumers basically just look at what’s been happening and extrapolate it into the future. This is a bad sign for bonds, which fall when interest rates rise and vice versa, in our view. Whenever the masses get so one-sided, it’s usually a sign that a trend reversal is near. Start a two-week free trial to Bespoke Institutional for full access to our research and market analysis. To receive our survey analysis every month, you’ll need to purchase our Consumer Pulse add-on.

The Fall of the Mall

Bespoke’s Consumer Pulse Report is an analysis of a huge consumer survey that we’ve been running each month since 2014. Our goal with this survey is to track trends across the economic and financial landscape in the US. Using the results from our proprietary monthly survey, we dissect and analyze all of the data and publish the Consumer Pulse Report, which we sell access to on a subscription basis. Sign up for a 30-day free trial to our Bespoke Consumer Pulse subscription service. With a trial, you’ll get coverage of consumer electronics, social media, streaming media, retail, autos, and much more. The report also has numerous proprietary US economic data points that are extremely timely and useful for investors.

We’ve just released our most recent monthly report to Pulse subscribers, and it’s definitely worth the read if you’re curious about the health of the consumer in the current market environment. Start a 30-day free trial for a full breakdown of all of our proprietary Pulse economic indicators.

You don’t need the Consumer Pulse Report to tell you that it has been a difficult few years for traditional brick and mortar retailers, especially for department stores. Just this morning, the September Non-Farm Payrolls report showed that the retail sector shed 11,400 jobs in September and has lost a total of 197K jobs since the sector’s peak reading in January 2017. With things being so bad for the sector for so long, though, there seems to be an increasing number of investors who think that the sector is due for a rebound, but based on the latest data from our Pulse report, it doesn’t look like things are showing any sign of improvement. In fact, trends may actually be getting worse.

The chart below is from a question that asks respondents which department stores they have visited over the last month or whether they haven’t visited any of them at all. In this month’s survey, a record 55.4% of respondents said they didn’t visit any of the department stores listed, while the percentage of consumers visiting each individual department store is at or near record lows. There was a time in the not so distant past where the seven stores listed were the first store shoppers thought of when they were planning to shop, but today they don’t even come to mind.

You can see in the chart that the seasonal holiday shopping period has been getting worse and worse for department stores as well. In 2015 and 2016, we saw huge dips in the “None of the above” reading in December, meaning lots of department stores saw a pick-up in visits. In 2017 and 2018, though, the dips for “None of the above” were much smaller.

What’s it going to take to get consumers back to stores? That’s the question every brick and mortar retailer has been trying to answer for the last few years along with how to maximize sales online. Providing a better “experience” for in-store shoppers has been the major focus, but experience can only take you so far.

Bespoke’s Morning Lineup – 10/4/19

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

The Closer – Range Bottoms, Bull Steepener, Big Reversals, And Manufacturing – 10/3/19

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, as equities found technical support today, we show the bull steepening of the curve and what it means in regards to policy. Next, we show other times that the S&P 500 experienced big intraday reversals as it did today. We finish with a look at today’s manufacturing data including durable and capital goods as well as consumer confidence and spending data.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

Dividend Stock Spotlight: Cola Wars With PepsiCo (PEP) and Coca-Cola (KO)

PepsiCo (PEP) is one of the world’s largest food and beverage corporations. In its long history, PepsiCo has come to offer a much broader range of products than just Pepsi Cola, which was first introduced all the way back in 1893 (when the soda was named “Brad’s Drink”). At the time, the cola was actually being pitched as a healthy, energy drink by pharmacists at drugstores. “Delicious and Healthful” was one of Pepsi’s first big ad promotions in the early 1900s as it was supposed to aid in digestion as well (from Wikipedia).

Over 125 years since its first product was created, consumers still are loving PEP’s offerings like Frito Lays and other popular sodas as the beverage giant announced strong third-quarter results this morning. EPS were reported at $1.56 per share, exceeding estimates of $1.51, while revenues came in $254 million above forecasts. This has led the stock price to respond well with a 4% rally today. That is a better than normal reaction as PEP has averaged just a +0.31% full-day change in response to earnings since 2000. In fact, over the last 19 years, this would be PEP’s sixth best one-day reaction to quarterly earnings if the gains hold into the close. From a chart perspective, this has led to a 180 from where things stood at yesterday’s close. Amidst yesterday’s broad market declines, PEP broke below support around $134. This support had been in place over the past month and could be traced back to prior resistance at spring/early summer highs. Today, the stock has reversed and the picture is much more bullish as the stock reached new 52 week highs.

In addition to solid technicals with today’s breakout, PEP also has an attractive dividend. PEP currently yields 2.75%, which is a higher yield than the broader market’s yield just under 2%. PEP is a member of S&P’s “Dividend Aristocrats” index, which is made up of stocks that have increased their dividends for at least 25 consecutive years. For Pepsi, the company has now increased its dividend for 46 consecutive years with the most recent increase being to the dividend paid in June. While the payout ratio for PEP is at the higher end among other dividend aristocrats, at 63.89%, the ratio is not overly concerning as the company has some cushion to continue to payout this dividend. Among other stocks in the Food, Beverage, and Tobacco industry, though, PEP’s dividend comes up just short of the group’s 3% average yield.

PepsiCo (PEP) stacks up closely with one of its oldest and largest competitors, Coca-Cola (KO). Like the broader industry group, Coca-Cola possesses a higher yield than that of PEP, but only slightly so at 2.97%. But KO also has a less attractive dividend payout ratio of 65.5%. Both stocks have P/E ratios right around 25. While KO is moving higher by 1.5% today on the back of PEP’s strong earnings, KO’s steep declines yesterday violated the past several months’ uptrend line from which it has not yet recovered, unlike PEP. Start a two-week free trial to Bespoke Premium for more dividend stock insights!