Bespoke Brunch Reads: 8/2/20

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, join Bespoke Premium with a 30-day free trial!

What Could Go Wrong

Researchers revive bacteria from the era of the dinosaurs (The Economist)

Using novel techniques, scientists have extracted bacteria from a layer of sediment at the bottom of the sea. Bacteria are part of “marine snow”, trapping beneath them older bacteria deposited from the part of the ocean closer to the sun. [Link; soft paywall]

Domino’s New Zealand drops ‘free pizza for Karen’ offer after backlash (BBC)

In a misguided effort to appeal to all the Karens out there, Dominos’ New Zealand and Australia division tried to “reclaim” that name used to describe racist middle-aged white women. The results were predictably quite bad. [Link]

Manhattan DA Made Google Give Up Information on Everyone in Area as They Hunted for Antifa by Albert Fox Cahn (The Daily Beast)

The Manhattan DA is using a novel technique to identify anti-fascist protestors from a conflict outside the Manhattan Republican Club last October. “Reverse search warrants” turn the very concept of a search warrant on its head, seeking to identify everyone fitting a condition rather than limiting government access to specific, factually-supported intrusion into what would otherwise be private spaces. Broader use of this technique would be a huge challenge to civil liberties in general. [Link]

Homes Is Where The Heart Is

RV shipments surge as Americans opt to carry home with them to avoid airports, hotels by Timothy Aeppel (Reuters)

While airplanes can be dangerous transmission zones if flyers don’t wear masks, and hotels create lots of contacts with the potentially infected, an RV is a safe zone that allows for comfortable travel without any concern about catching coronavirus. [Link]

The Cold War Bunker That Became Home To A Dark-Web Empire (The New Yorker)

A cold war bunker went on the market for €350,00 in 2012, and was eventually picked up by one of the stranger characters the 90s tech-utopian period ever produced in order to host whatever customers wanted to put online. [Link; soft paywall]

Norms Come, Norms Go

Americans are getting more nervous about what they say in public (The Economist)

While free speech absolutists may cringe at the notion that people should be careful with their words lest they hurt those listening, Americans appear to be feeling a bit more considerate when it comes to voicing their political views. [Link; soft paywall]

‘Hey, You Free on Friday for a Meeting and a Bank Heist?’ by David Segal (NYT)

Virtual meeting places are expanding from the boredom of Zoom calls into the drama and excitement of video games; clients and the firms catering to them have fled into that space for the same reasons they used to go to bars or restaurants together instead of just meeting rooms. [Link; soft paywall]

MacKenzie Scott Donates $1.7 Billion to Charity Within Months by Sophie Alexander (Bloomberg)

The world’s 13th-richest person, MacKenzie Scott, has donated 2.8% of her net worth to charities that promote racial equity, fight climate change, and protect public health. [Link; soft paywall]

COVID

Herd Immunity May Be Developing in Mumbai’s Poorest Areas by Ari Altstedter and Dhwani Pandya (Bloomberg)

More than half of Indians living in some of the largest slums around Mumbai show antibodies for COVID-19, suggesting that those populations are nearing herd immunity for the pandemic; estimates of where that broad level of protection kicks in are around 80% and higher. [Link; auto-playing video, soft paywall]

A national teachers’ union says its members can strike to ensure schools reopen safely. (NYT)

The second-largest teachers’ union said this week that they would support strikes in districts or states that moved to reopen classrooms without safety protocols in place. [Link; soft paywall]

Covid-19 infections leave an impact on the heart, raising concerns about lasting damage by Elizabeth Cooney (Stat News)

A pair of German studies identified significant damage to COVID patients hearts after recovery (including high prevalence of biomarkers that are present after a heart attack) and significant levels of the virus in the hearts of deceased patients. [Link]

Stocks

When Tesla Hits the S&P 500, It’ll Spark the Wildest Passive Trade Ever by Sarah Ponczek (Bloomberg)

It’s uncommon for very high market cap stocks to be added to the S&P 500, but Tesla fits the bill after reporting four consecutive quarters of positive net income with its most recent quarterly release; its addition to the index could spark some pretty wild trading. [Link; soft paywall]

Dumb Money Making Smart Stock Picks in Yearlong Robinhood Rally by Vildana Hajric and Saraha Ponczek (Bloomberg)

Data suggests that Robinhood investors are basically the opposite of the “dumb money” tropes which are typically used to describe high frequency retail trading. [Link; soft paywall]

Coal

Falling giants: Britain’s vanishing cooling towers by Michael Collins (FT)

Coal cooling towers (also associated with nuclear power plants) have become a less common part of the national landscape in Europe as the continent has shifted away from that form of electricity. [Link; paywall]

Europe steams towards coal exit – research by Isla Binnie (Reuters)

The drop in electricity demand brought on by COVID has expedited a plunge in the volume of coal burned at power plants, with renewable sources now producing 40% of EU electricity. [Link]

Future Forecasts

Everybody’s An Expert by Louis Menand (The New Yorker)

The science of prediction is somewhat loose, but it does suggest that there are many ways to make mistakes with too much expertise. [Link; soft paywall]

Read Bespoke’s most actionable market research by joining Bespoke Premium today! Get started here.

Have a great weekend!

The Bespoke Report — A False Act?

This week’s Bespoke Report newsletter is now available for members.

Just when they thought Tech was out, they pulled it back in!

Since peaking on July 20th, the Tech sector and FAANG names had been experiencing some downside mean reversion. That downside action came to an end on Friday when Apple (AAPL), Amazon (AMZN), and Facebook (FB) all surged on extremely impressive earnings results.

Below is one chart from this week’s Bespoke Report that shows the strength we’ve seen from the mega-caps in 2020. As shown, the five largest stocks in the S&P 500 have collectively added $1.66 trillion in market cap this year. The other 495 stocks in the index have lost $1.61 trillion in market cap!

We discuss this week’s action across financial markets in our weekly Bespoke Report newsletter. To read the report and access everything else Bespoke’s research platform has to offer, start a two-week free trial to one of our three membership levels. You won’t be disappointed!

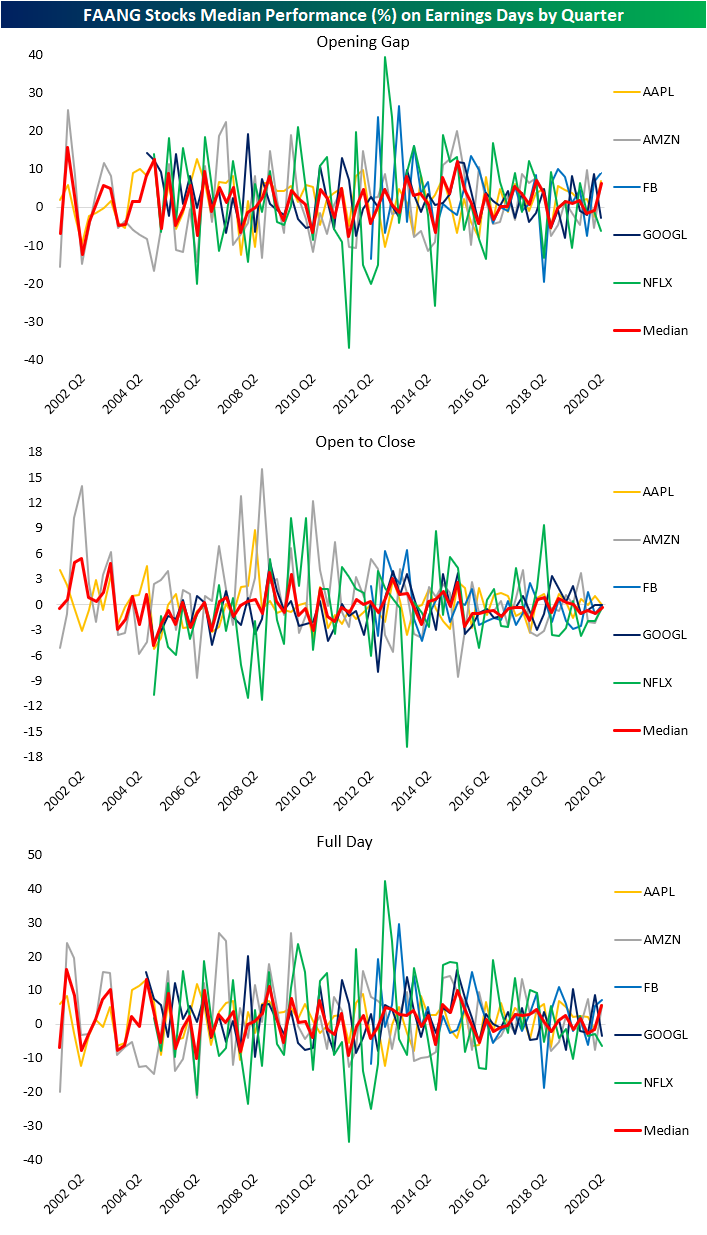

FAANG Flying on Earnings

Earlier this month, Netflix (NFLX) reported a disappointing quarter with EPS missing estimates by 24 cents which led the stock to fall 6.52% on its earnings reaction day. The rest of the FAANG group—Facebook (FB), Apple (AAPL), Amazon (AMZN), and Alphabet (GOOGL)—all reported their second-quarter results last night which we discussed in the Closer. With the exception of GOOGL, the results were very strong. Despite beating top and bottom-line estimates by $954.65 million and $1.9/share, respectively, GOOGL’s revenues were lower year over year for the first time ever and that has the stock lower today. The rest of the group beat estimates, and Amazon (AMZN) even reported a triple play for the first time in over a decade. The last triple play by AMZN was in January of 2010 back when the company’s market cap was ~$54 billion; roughly 3.4% of its current market cap over $1.59 trillion. In fact, at the open today, AMZN added more in market cap than it’s entire market cap back then.

Given the strong earnings, these stocks are flying today. In fact, Apple, Facebook, and Amazon all gapped up over 5% this morning, and as of this writing, AMZN is the only one to have pared some of those gains currently trading just over 3.8% higher on the day. In the charts below, we show how each of the FAANG stocks has performed on earnings days across each quarter in our Earnings Explorer database. On a median basis, this quarter is looking to be the best in terms of full-day performance (based on where they are trading intraday) of FAANG stocks on earnings days since Q1 2018 while the median opening gap of 6.2% is the quarter best since Q2 2015. This quarter also marked the first time since Q1 of 2018 that at least 3 FAANG stocks all gapped up over 5%. If AMZN, moves back above a 5% gain on the day, it would be the first time since Q2 of 2015 that at least three FAANG stocks rose 5%+ on their earnings reaction days.

Of the specific stocks, Facebook’s reaction today is looking to be its best earnings reaction day since January 2019 (10.82%). For Amazon (AMZN), it is the best Q2 earnings reaction day since 2015, but back in January of this year, the stock saw a much larger 7.38% gain in response to Q4 earnings. For Apple, the pop on earnings is looking like it will the stock’s best earnings reaction day since January of 2019 when it gained 6.8%. Click here to view Bespoke’s premium membership options for our best research available.

Bespoke’s Weekly Sector Snapshot — 7/30/20

Please click the thumbnail image below to view our weekly Sector Snapshot report.

S&P 500 Stronger Underneath the Surface

Earlier today we posted a chart showing S&P 500 sector performance since the Nasdaq’s recent peak on 7/20 when Technology stocks began what has now been a 10-day period of consolidation. Below we have updated these performance numbers to include today’s moves. While not as many sectors remain in positive territory, the majority of sectors continue to outperform the S&P 500, while Technology drags the market lower. Along with Technology, Communication Services, and Consumer Discretionary are the only other sectors that have lagged the S&P 500, and their performance has been dragged down by the mega-cap tech-like stocks of Alphabet (GOOGL), Facebook (FB), and Amazon (AMZN).

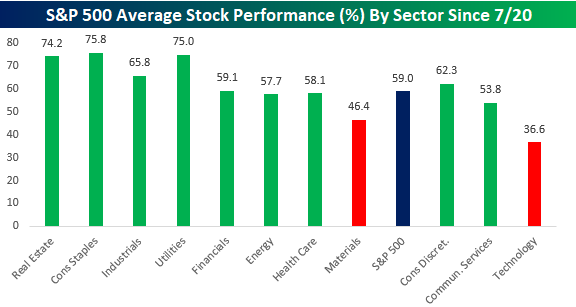

Expanding on this theme of underlying strength in the index, the chart below shows the average performance of stocks in the S&P 500 grouped by sector. On an equal-weighted basis, the S&P 500 is actually up 1.3% since 7/20, and only two sectors (Technology and Materials) have seen negative average returns. On the upside, Real Estate (4.1%) has been the big winner followed by Consumer Discretionary (3.3%), and Consumer Staples (2.2%). The fact that Consumer Discretionary at the cap-weighted sector level is down over 1.4% while the average performance of stocks in the sector has been a gain of 3.3% illustrates what a mammoth impact AMZN has on that sector.

Breadth among S&P 500 stocks has also been overwhelmingly positive. For the S&P 500 as a whole, 59% of stocks in the index have had positive returns since the close on 7/20. Only two sectors (Technology and Materials) have seen fewer than half of their components post positive returns over that time, while Real Estate, Consumer Staples, and Utilities have seen roughly three-quarters of their components rally since 7/20. Like what you see? ]Click here to view Bespoke’s premium membership options for our best research available.

Bears Double Bulls Again

The S&P is flat over the past week and is roughly 1.3% away from last Wednesday’s high. Even though there has not been any significant push lower, sentiment has taken a hit as AAII’s reading on bullish sentiment has fallen down to 20.23%. That is a 5.83% drop from last week (the largest since a 9.91 percentage point decline on June 18th) and marginally surpasses the recent low last October of 20.31% to mark the lowest reading for bullish sentiment since May of 2016. Think about that. Investors in this survey are less bullish now than they were at any point throughout the COVID crisis

Meanwhile, bearish sentiment rose to 48.47%. Unlike bullish sentiment, that does not surpass any earlier readings for a multiyear high as it is the highest level since only the end of June. But it is also now only 3.6 percentage points away from the March 26th high when more than half of investors were reporting as bearish.

As we discussed in greater detail in today’s Chart of the Day, bears more than double bulls as the bull-bear spread is now at its widest level in favor of bears since the first week of May. Back then it was only slightly wider at 28.99. While not at a new low, the bull-bear spread has been negative for a record 23 week-long streak.

Not all the losses to bulls this week went to bears as neutral sentiment rose to 31.3%. That is the highest since the start of the month. Click here to view Bespoke’s premium membership options for our best research available.

Chart of the Day: Bulls Outnumbered

Bullish Earnings Season So Far

At our Earnings Explorer tool available to clients on our website, we provide a real-time look at beat rates for both EPS and sales. Below is a snapshot from the website showing both the EPS and sales beat rates for US companies reporting earnings on a rolling 3-month basis. Currently, 64.61% of companies have exceeded consensus analyst EPS estimates over the last three months, while 63.75% of companies have beaten consensus sales estimates over the same time frame.

In looking at the chart, you can see a big spike in the EPS beat rate over the last few weeks. Since earnings season began on July 13th, nearly 80% of companies have posted stronger than expected EPS numbers. That’s a huge beat rate and suggests that analysts were too bearish on Q2 numbers heading into July. The revenue beat rate held up much better than EPS beats throughout the first half of 2020, but it too is on the upswing this season.

We also monitor how share prices are reacting to earnings reports. So far this earnings season, the average stock that has reported Q2 numbers has gained 1.31% on its earnings reaction day. That compares to a historical average one-day change of just 0.06% on earnings reaction days. As shown below, stocks that have beaten EPS estimates this season have gained 2.2% on earnings reaction days, while companies that have missed EPS estimates have fallen 1.89%. It’s rare to see beats gaining more than misses decline, but that’s what is happening this season. Click here to view Bespoke’s premium membership options for our best research available.

Claims Higher in Back to Back Weeks

Initial jobless claims (seasonally adjusted) rose from 1.422 million to 1.434 million this week. That marks the first time since the second half of March that seasonally adjusted jobless claims have risen week over week in back to back weeks. While 16 weeks without back to back increases in jobless claims may sound like a very long streak, it is only the longest such streak since April of last year, and there were two other long streaks of 15 weeks and 12 weeks in between. On the bright side, this week’s reading of 1.434 million was better than forecasts for an increase to 1.445 million. Additionally, while claims continue to rise and print deep into the millions, this week’s increase of 12K was much more modest than the 114K increase last week.

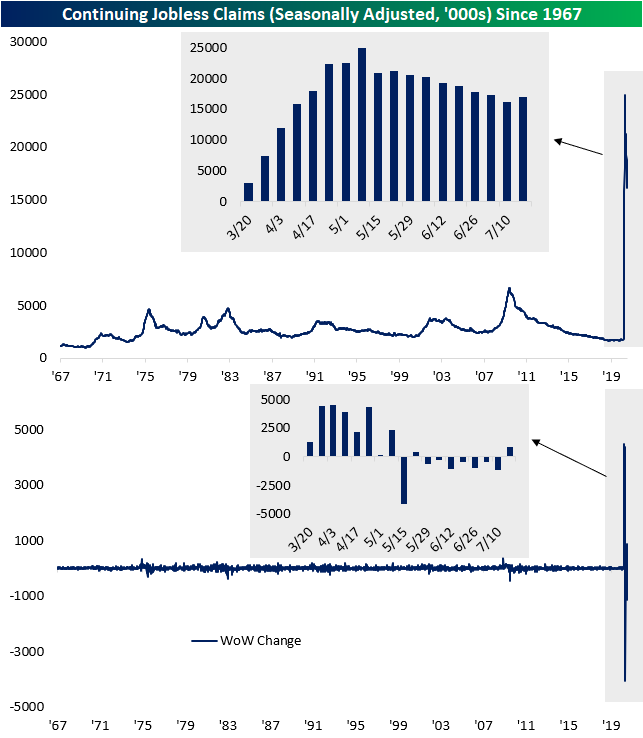

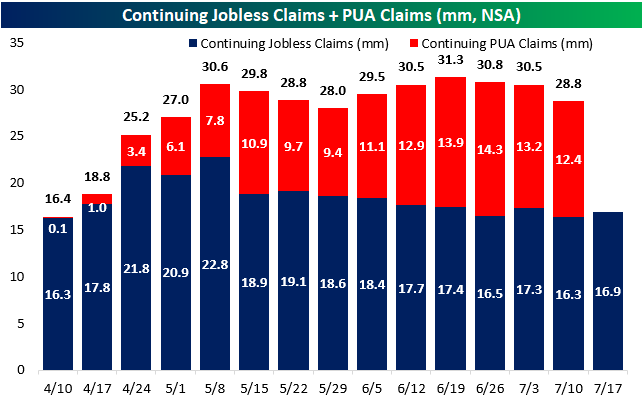

Given that large uptick in initial claims last week, seasonally adjusted continuing claims also picked up. Continuing claims for the week of July 17th (continuing claims are lagged one week to initial claims) rose back above 17 million this week. That was above expectations for claims coming in at 16.2 million.

As we noted last week and was again the case this week, there is a divergence between the seasonally adjusted number which is rising, and the non-seasonally adjusted (NSA) number which is falling. As shown below, the massive upswing in claims in the spring that has persisted through the summer makes it somewhat hard to compare for seasonal patterns, but in the past few weeks, the data has risen and is now falling consistent with typical seasonal patterns for this time of year. In other words, as the seasonally adjusted data has deteriorated a bit in recent weeks, it is hard to distinguish if recent improvements in the unadjusted data are material improvements in the labor market or more a factor of seasonality.

As such, NSA initial claims fell from 1.377 million down to 1.205 million this week. That is the lowest level of jobless claims since the first reading above one million earlier in the pandemic in March. That was also the largest decline since the last week of May.

Factoring in Pandemic Unemployment Assistance (PUA) claims shows the same story. Like the standard NSA number, PUA claims have fallen for a third straight week totaling 0.83 million and bringing the grand total to 2.04 million. For PUA claims, this was the lowest initial claims print since the second week of June when PUA claims came in at 0.77 million. Again, it is hard to distinguish how much of this improvement may be seasonality versus more concrete improvements in the data, but this is the lowest reading since PUA claims began to be tracked in April.

It is a similar story for continuing jobless claims (NSA) which are also down for a third straight week when including PUA claims (lagged an additional week to the already lagged continuing claims). PUA claims were at their lowest level since the first week of June, and total continuing claims are at their lowest since the last week of May. Click here to view Bespoke’s premium membership options for our best research available.

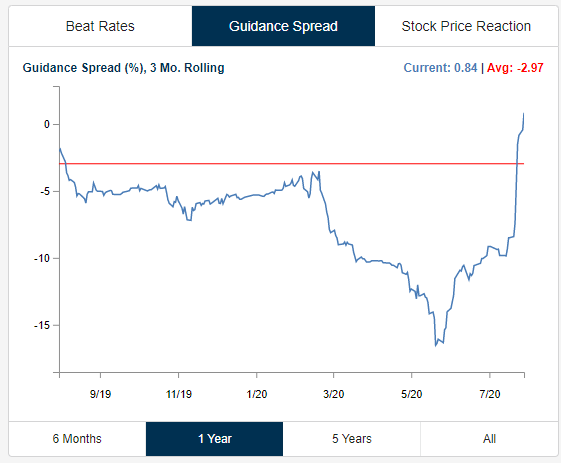

Raising Guidance

We saw another 13 earnings triple plays (beat EPS, beat sales, raised guidance) after hours today. Companies are raising guidance like crazy this earnings season, causing our Guidance Spread tracker (see chart below) to spike up into positive territory in the span of two weeks. It seems that worst fears either failed to materialize or the “Covid Economy” is actually benefiting a lot of public companies. Or maybe it’s a little bit of both. You can track the 100 most recent earnings triple plays at our Tools page. Learn more about Bespoke Premium.