Bespoke’s Morning Lineup – 3/14/22 – Up (For Now)

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Life is like riding a bicycle. To keep your balance, you must keep moving.” – Albert Einstein

It’s a new week, and while it has been typical to see futures lower on the first trading day of the week so far this year, the S&P 500 and Dow are currently indicated higher. Nasdaq futures were higher earlier but have given up those gains. The catalyst for the weakness in tech stocks this morning is likely due to new COVID lockdowns in China and the impact that these shutdowns will have on tech supply chains.

Crude oil prices are down over 5%, and the cause for that decline seems to be tied to some positive sentiment related to cease-fire negotiations over the Russia-Ukraine war, but it could also be related to concerns over demand as China starts new rounds of Covid lockdowns. One thing for sure, is that a new wave of lockdowns in China, will not be good for global economic growth.

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including the latest US and international COVID trends.

It’s a new week for the markets in what has been a lousy year. Heading into the week, all but four sectors are oversold, while Energy and Utilities actually finished last week at overbought levels. Consumer Staples (XLP) was the big loser last week falling close to 6%, while Technology (XLK) and Communication Services (XLC) fell more than 3%. On a year-to-date basis, the performance disparity between Energy and everyone else continues to widen. While XLE is up over 38% YTD, no other sector is in the black, and Consumer Discretionary (XLY), XLK, and XLC are all underperforming the Energy sector by more than 50 percentage points YTD. Gaps in performance of that magnitude are pretty much unprecedented.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Bespoke Brunch Reads: 3/13/22

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, join Bespoke Premium with a 30-day free trial!

Ukraine

The Dangerous Allure Of The No-Fly Zone by Mike Pietrucha & Mike Benitez (War On The Rocks)

Needed context and discussion for why an American or NATO-established no-fly zone over Ukraine would be both relatively unhelpful to Ukraine and create a massive risk of a devastating wider war in Europe. [Link; paywall]

Energy

The Biden Administration Has The Power: Administrative Authority To Address The Crisis in Oil Supply Right Now by Alex Williams, Arnab Datta, & Skanda Amarnath (Employ America)

A novel approach to reducing the cyclicality of energy production, ensuring lower price volatility and more stable supply by absorbing oil price volatility and demand mitigation on to the American government’s massive balance sheet. [Link]

Lead from gasoline blunted the IQ of about half the U.S. population, study says by Elizabeth Chuck (NBC)

Leaded gasoline created massive exposure to the IQ-blunting metal across the US population, with an average impact of 2 IQ points per person but much higher impacts among earlier generations. Leaded gasoline has been banned for more than a quarter century. [Link; auto-playing video]

Fertilizer giant Yara slashes production in Europe (CNN/Reuters)

Norwegian company Yara is cutting production of ammonia and urea at plants in Italy and France thanks to the extreme prices for natural gas (a key input to fertilizer) in Europe. [Link]

Municipal Matters

‘Booming’ LIRR and Metro-North commuters return to Manhattan in high spirits by Alex Mitchell (NYP)

As offices in Manhattan reopen, commuters are swarming back on to the tracks of commuter rail services around the New York area. [Link; auto-playing]

U.S. Retirement Funds, Heavy on Stocks, Brace for Losses by Heather Gillers (WSJ)

With more than 61% of their assets dedicated to equity markets, US public pensions are highly exposed to the stock market. Declines could pressure state and local finances though of course operating budgets are in excellent shape thanks to the post-pandemic economic boom. [Link; paywall]

Facebook Libra: the inside story of how the company’s cryptocurrency dream died by Hannah Murphy and Kiran Stacey (FT)

An effort by Facebook to launch a digital currency found tentative support from the Federal Reserve Chair before Treasury pulled support. Ultimately, a failed lobbying campaign in Washington meant Diem never took off. [Link; soft paywall]

Facebook allows war posts urging violence against Russian invaders by Munsif Vengattil & Elizabeth Culliford (Reuters)

In a revealing change at the company’s own discretion, Facebook will no longer interdict posts calling for violence against Russian troops invading Ukraine. [Link]

Yikes

Gig App Gathering Data for U.S. Military, Others Prompts Safety Concerns by Byron Tau (WSJ)

Ukrainians paid to take pictures of specific areas in rural Ukraine were unwittingly participating in a US DoD research project designed to assess the accuracy of satellite photos. [Link; paywall]

Some Understaffed PetSmarts Are Dealing With Freezers Overflowing With Dead Pets by Lauren Kaori Gurley (Vice)

PetSmart stores that have been understaffed are seeing a wave of dead pets that end up stacked in freezer and improperly disposed, adding a horrifying twist to the difficulty of running a business based on selling living things. [Link]

Sovereignty

Corporate Sovereign Awakening and the Making of Modern State Sovereignty: New Archival Evidence from the English East India Company by Swati Srivastava (Cambridge University Press)

A painstaking analysis of the growth of the English East India Company, which grew outside of the English state to the point that it actually challenged the sovereignty of the nation. [Link]

Counting

2020 Census Undercounted Hispanic, Black and Native American Residents by Michael Wines & Maria Cramer (NYT)

Amidst the challenge of the COVID pandemic, the Census likely undercounted the US population by millions of people, though that undercount does not appear to be much larger than previous decennial surveys. [Link; soft paywall]

Read Bespoke’s most actionable market research by joining Bespoke Premium today! Get started here.

Have a great weekend!

Gas Prices Hit A New Record

Crude oil may have reversed lower this week, but it’s hard to tell when drivers head to the pumps. The national average for a gallon of regular gasoline has continued to rise to hit a record high of $4.33 in data from AAA going back to 2004. While prices typically rise this time of year, the vertical move this year has meant prices have grown at a much more rapid rate than normal.Click here to read Bespoke’s premium research.

The Bespoke Report – 3/11/22 – No Way Out?

This week’s Bespoke Report newsletter is now available for members.

No way out is a phrase we’ve heard a lot lately. Whether it’s Putin’s war in Russia, the FOMC, or the market, it’s hard to picture a smooth way out for any of them in the middle of this morass. Concerns aside, life goes on and the markets will open on Monday – or at least most will. So, grab a coffee, or for this week, you may want something a little stronger, and read up on the latest trends impacting markets and the economy in this week’s Bespoke Report.

To read this week’s full Bespoke Report newsletter and access everything else Bespoke’s research platform has to offer, start a two-week trial to one of our three membership levels.

“Verb” Stocks Hit the Curb

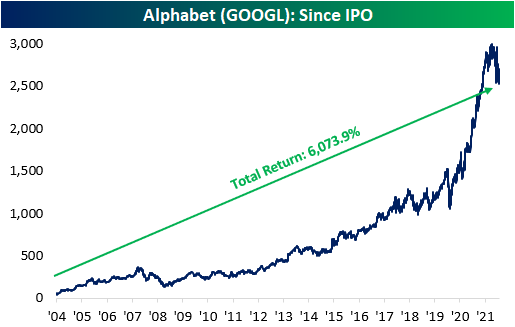

In the business world, there’s an axiom that says: when your company name becomes a verb, you’ve arrived. Take the example of Google in the late 1990s. When people started replacing the phrase ‘online search’ with ‘Google it’, you just knew that Google was going to be a big company. Since its IPO in 2004, Google – now called Alphabet (GOOGL) – has been an absolute behemoth, posting a total return of 6,073.9% and an annualized gain of 26%. GOOGL has taken over the internet search business over the years, making it one of the world’s most influential companies and the ultimate verb stock.

While GOOGL is an example of a verb stock that has seen stellar returns, a group of more recent verb stocks hasn’t fared nearly as well. Over the past few years, certain companies have introduced products and services that have become so integral to their daily lives that their names have become verbs. Owe someone money for lunch? Just venmo them. Not feeling well? Might be a good idea to schedule a teladoc appointment with your doctor before going out. Need to sign a document? No need to print it out and fax it back. Just docusign it. Have a client meeting but traffic is a nightmare? Why don’t you just hop on a zoom.

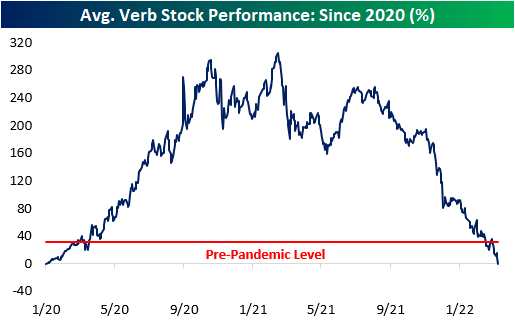

The services these companies offered became necessities of daily life during the pandemic, and because of that their stocks surged. We created an equally-weighted basket tracking the performance of PayPal (PYPL), Teladoc (TDOC), DocuSign (DOCU), and Zoom (ZM). From the start of 2020 (right before the pandemic) through the basket’s peak in early 2021, these stocks tripled. Around that point, investors began to question what the outlook for these stocks would be when the economy re-opened, but proponents argued that the services these companies offered provided such a convenience that they wouldn’t miss a beat.

While consumers around the world are still venmo-ing, teledoc-ing, docusign-ing, and zoom-ing, the stocks of all these companies have been imploding. The basket of four stocks has now erased all of its COVID gains and is now in the red relative to where it traded at the start of 2020.

Although there is a little bit of variation in the performance of these four stocks, the overall trend is largely similar. Of the four, ZM is the only one that is still positive relative to where it started in 2020. PYPL, TDOC, and DOCU, on the other hand, have declined 11.4%, 33.6%, and 4.1%, respectively. As you can see from the graph below, these stocks have round-tripped, erasing all of the gains provided by the pandemic. While valuations were certainly stretched for a while, the fact that these stocks are lower now than they were before COVID, even after proving their worth during the pandemic, shows how much sentiment has shifted in the last several months. One trend not working in favor of these verb companies is competition. As the pandemic proved the viability of their business models, competitors have been quick to step in. These days, someone may ‘venmo’ you using the CashApp, do a ‘teladoc’ appointment through CVS, ‘docusign’ an application using Adobe E-signature, or do a ‘zoom’ over Teams or Google Meets. Click here to read Bespoke’s premium research.

Bespoke’s Morning Lineup – 3/11/22 – It’s Friday

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“And Lord, we’re especially thankful for nuclear power, the cleanest safest energy source there is. Except for solar, which is just a pipe dream.” – Homer Simpson

It’s just a coincidence that Google searches for the term ‘nuclear war’ are hitting a record high as we’re marking the 11th anniversary of the Fukushima nuclear disaster in Japan, but the term nuclear has been showing up a lot lately. Whether it is Germany’s plan to shut down its nuclear power plants and make it even more reliant on Russian energy, or the Russian invasion of Ukraine that has raised risks of a nuclear accident at the site of the former Chernobyl plant or Ukraine’s other nuclear power plants that are operational, or the risk of nuclear war with Russia if NATO comes in to actively help defend Ukraine, you can’t get away from the subject of nuclear lately.

Thankfully, equity markets look to be putting a lot of these concerns aside temporarily giving investors a reprieve heading into the weekend. S&P 500 futures are currently up over 1%, crude oil is up over 1%, gold is down 1.5%, the 10-year yield is flat right at about 2.0%, and bitcoin is right around $40,000. The positive tone in equities was present for most of the night but just got an added boost shortly before 7 AM on reports that Russian President Putin said there were positive shifts in talks with Ukraine. At this point, the markets will take whatever good news they can get, but keep in mind that Putin is also the one who said Russia wouldn’t invade Ukraine.

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including the latest US and international COVID trends.

It’s been a pretty nasty week for US equities since the close last Thursday. During that span, the S&P 500 is down over 2% while the Nasdaq is down 3%. The worst performing sector during this period has been Consumer Staples (XLP) which is down close to 5%, while Technology (XLK) and Financials (XLF) are both down over 3%. Rounding out the top five of biggest losers, Communication Services (XLC) and Consumer Discretionary (XLY) are both down over 2.5%. Not surprisingly, all five of the aforementioned sectors are also at short-term oversold levels.

While most sectors are lower, three have managed to buck the trend over the last week. Energy (XLE) has been the biggest winner, rising close to 6%, followed by Utilities (XLU) and Real Estate (XLRE). Unfortunately for the broader market, though, these three sectors are also the smallest sectors in terms of their weightings in the overall S&P 500.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

The Closer – Inflation Surge Continues, Fiscal Tightening, Strong Bond Bidding – 3/10/22

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we start out tonight by taking a look at the backwardation of crude oil and crack spreads followed by an update on the situation in Ukraine. We then dive into today’s inflation data. Next, we look at government receipts and today’s historically strong 30 year bond sale.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

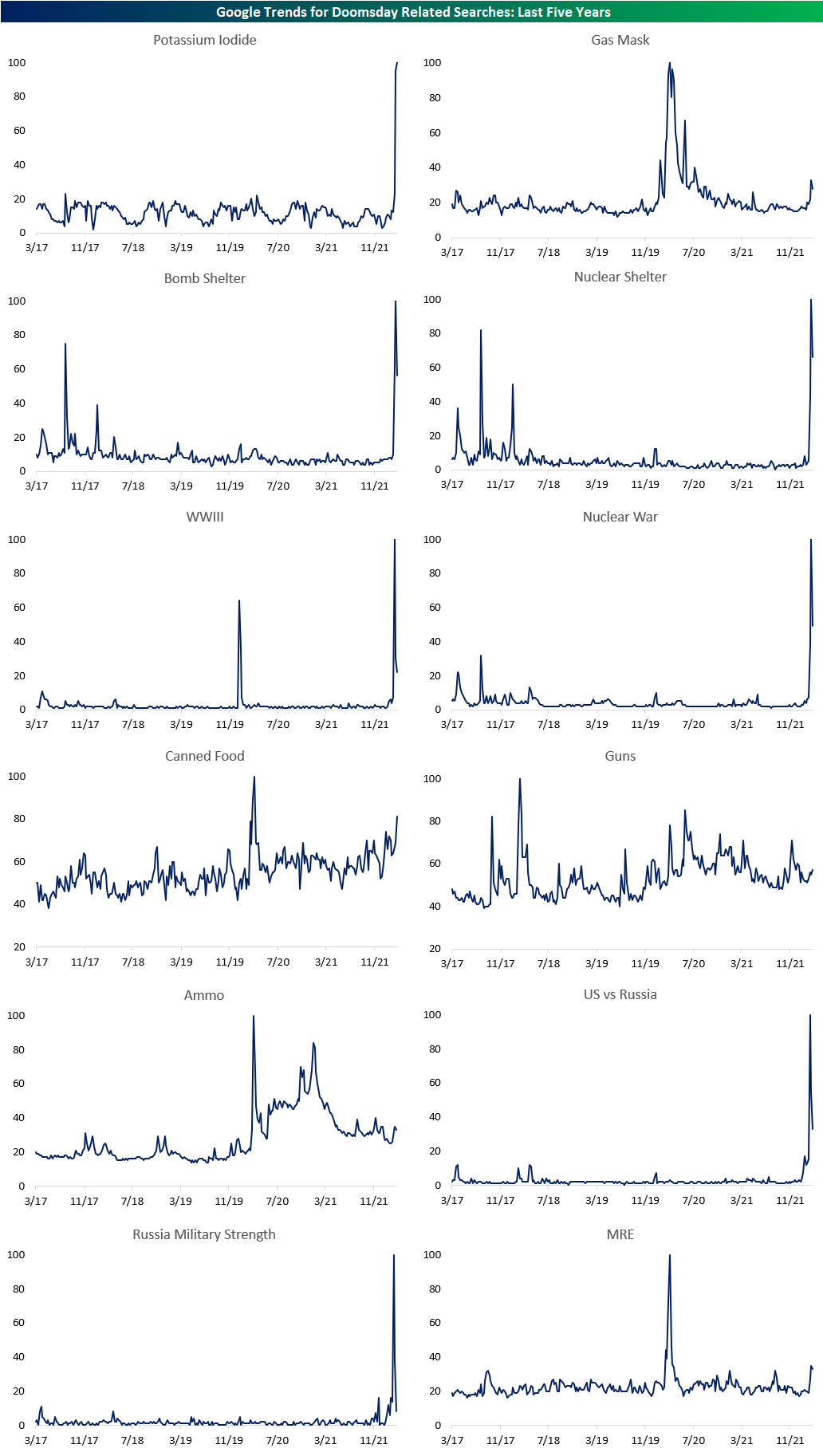

Doomsday Fear Index

During the Cold War, American children and adults were educated on how to best protect themselves from a nuclear explosion. This included measures from the silly “duck and cover” campaign to nuclear fallout shelter instructions. If you happen to be curious about the federal government’s current recommendations in regards to protection from a nuclear blast, you can read up on the instructions here. We’re not sure how focused people will be about wearing a mask in the event of nuclear fallout, but we guess you can never be too careful!

{kind=link}

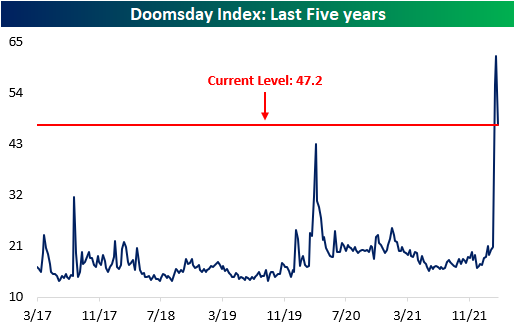

With tensions between Western nations and Russia reaching levels not seen since the Cold War, we took a look at Google Trends to identify the level of fear in the American population with respect to the current war in Ukraine. We looked at the search volumes for terms like nuclear war, WWIII, canned food, Potassium Iodide, and gas mask. Searches for many of these terms hit five-year highs in the early days of the Russian invasion but have subsided since. The current level is still well above normalcy, but fears appear to have eased over the last week as the West’s retaliation has been almost entirely economic (or maybe there is no internet service in the fallout shelters). The aggregate index is pictured below.

Below are charts of each search term we utilized in the composition of our index. Potassium Iodide, the compound utilized to mitigate the effects of excessive radiation exposure, is the only term that remains at a five-year high in terms of search volume. While searches for some of these terms were actually much higher during the early days of COVID, they all experienced upticks in the last few weeks. All-in-all, based on search trends based on fears of a nuclear situation or war with Russia spiked when the Ukraine invasion first started, but those fears have over the course of the last week. Click here to view Bespoke’s premium membership options.

Chart of the Day: The Immaculate Correction

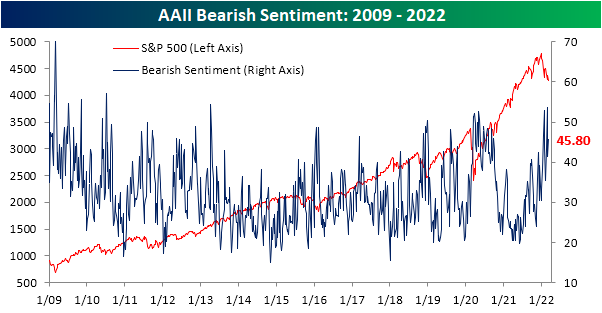

Investor Sentiment Remains Volatile

Considering equities and other risk asset prices continue to swing violently, so too have readings on investor sentiment. The weekly AAII survey of individual investors saw the percentage of respondents reporting as bullish fall back below 25% this week after rising above 30% last week. While that is not the largest drop in recent months (the second week of January saw bullish sentiment fall 7.9 percentage points compared to 6.4 today), it nonetheless reaffirmed that investor confidence is shaky, if not undecided, at the moment.

The drop in bullish sentiment was mostly picked up by those reporting as bearish. Bearish sentiment rose 4.4 percentage points to 45.8%. While that reading is roughly 15 percentage points above the historical average for bearish sentiment, the reading is still lower than an even more pessimistic reading only two weeks ago when more than half of respondents reported as bearish.

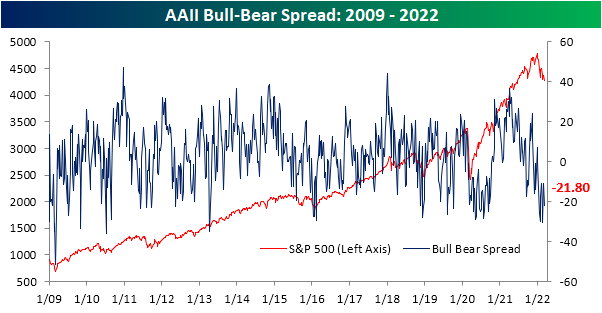

With the inverse moves in bullish and bearish sentiment, the bull-bear spread has pulled back to -21.8. As with bullish and bearish sentiment, even if that does not set a new low, it is only in the 5th percentile of readings going back to the start of the survey.

After the largest single-week decline in nearly 20 years two weeks ago, neutral sentiment has been clawing its way back into the range it was in for most of the past year. Gaining another 2 percentage points this week, the reading is now back above 30%.

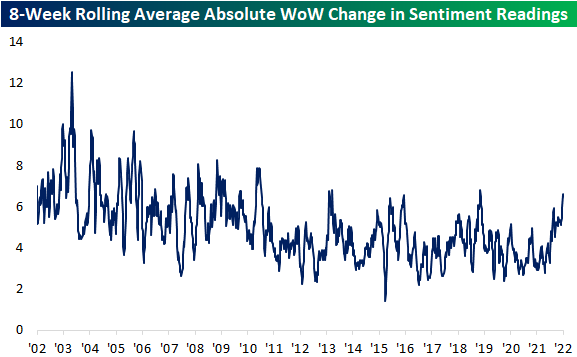

Across each category of the report, there have been sizable swings in the past two months. To highlight this, in the chart below we show the eight-week rolling average of the absolute week over week change for each sentiment reading (bullish, bearish, and neutral) over the past 20 years. Over the history of the survey, weekly changes have gravitated towards smaller swings meaning the past decade is structurally a bit different relative to the decade before that. That being said, the weekly swings in the AAII readings on sentiment have been some of the largest of any period of the post-Global Financial Criss era. In fact, not even the COVID crash saw such volatility in sentiment (given optimism collapsed and then remained muted for some time rather than swing back and forth) while the only times this average was as high as now in the past decade were the spring of 2013, February 2016, and January 2019. Click here to view Bespoke’s premium membership options.