Consumers Run From Stocks

The New York Fed runs a monthly survey of consumer expectations (SCE) which covers topics ranging from inflation, the labor market, and household finances, and while its history is limited (starts in 2013), it provides a great look at where US consumers see the state of the economy and financial markets. The latest update for the month of June was released earlier today and provided some really interesting insights regarding different trends, but one we wanted to focus on here is how Americans view the prospects for stock prices.

As the equity market has weakened this year amid higher inflation and the Fed’s rate hike cycle, consumer sentiment towards the stock market has been declining, but the pace has really picked up in the last two months taking the total percentage of consumers expecting higher stock prices to its lowest level (33.8%) in the history of the survey. Put another way, just about two-thirds of US consumers expect stock prices to remain flat or decline over the next 12 months. Add this to the long litany of other sentiment surveys showing investors and consumers alike have little confidence in the stock market. Click here to learn more about Bespoke’s premium stock market research service.

Chart of the Day – What About That Yield Curve?

Bespoke Brunch Reads: 7/10/22

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, join Bespoke Premium with a 30-day free trial!

Autos

Registrations for electric vehicles soar, signaling increasing mainstream acceptance by Jayme Deerwester (USA Today)

Electric vehicle sales industry-wide were up 60% YoY in Q1 despite an 18% drop in overall registrations. Fully electric vehicles in the US are just below 5% of total passenger sales in the US with roughly 60% of sales driven by Tesla. [Link; auto-playing paywall]

Monthly car payments have crossed a record $700. What that means by Brittany Cronin (NPR)

The combination of car price inflation and more feature-laded vehicles along with soaring interest rates are driving a surge in the monthly payment required to cover a car purchase. [Link]

New York Waterways

Give Me Your Tired, Your Poor, Your Pods of Dolphins—New York Welcomes New Immigrants by Alyssa Lukpat (WSJ)

As the rivers around New York have gotten cleaner, dolphins have returned to New York harbor in pursuit of a snack. Fins have been spotted from Brooklyn to Harlem, delighting residents. [Link; paywall]

She died in a Manhattan penthouse but was buried on an island for the poor by Mary Jordan (WaPo)

A tiny one mile slice of Long Island Sound is the largest public cemetery in America, serving as the final resting place for more than 1 million souls interred since 1869. [Link; soft paywall]

Real Estate

Roaring US Rental Market Shows Early Signs of Slowing Down by Paulina Cachero (Bloomberg)

High frequency indicators suggest that rents are starting to fall in a range of markets that were absurdly hot during 2020 and 2021, with large drops for 1- and 2-bedroom apartments alike. [Link; soft paywall, auto-playing video]

The Suburban Lawn Will Never Be the Same by Brian Eckhouse and Siobhan Wagner (Bloomberg)

As drought wracks the American West, homeowners have started to replace dead, dried out grass with artificial turf which doesn’t have the same thirst for scarce water that real blades would soak up. [Link]

Crypto

‘It’s Ruined Me’: Voyager Customers Fear Life Savings Gone After Crypto Firm’s Bankruptcy by Maxwell Strachan (Vice)

A crypto brokerage that promised huge yields for deposits of fiat currency has suspended withdrawals and declared bankruptcy, leaving customers holding the bag. [Link]

Sports

World Cup stadiums in Qatar to be alcohol-free – source (i24)

Thirsty footy fans are going to be totally out of luck at the World Cup this fall, with host country Qatar banning alcohol consumption in public…including the stands of matches at the iconic sporting event. [Link]

Fiscal Policy

Was the Paycheck Protection Program Effective? by William R. Emmons and Drew Dahl (FRB St Louis)

As COVID smashed the US economy in 2020, Congress traded off speed for precision. The consequence is that Paycheck Protection Program loan/grants were much less useful in supporting workers than unemployment insurance or economic impact payments. [Link]

Energy Shortage

Germany dims the lights to cope with Russia gas supply crunch by Guy Chazan (FT)

Russia is cutting off natural gas supplies to Germany, and the result is a nationwide energy crisis that is forcing rationing and massive price inflation onto households used to cheap and reliable gas supplies. [Link; paywall]

That’ll Leave A Mark

Markets Had a Terrible First Half of 2022. It Can Get Worse. by James Mackintosh (WSJ)

Stocks collapsed in the first half of the year, but the pessimist’s perspective offers little hope of a major rebound in the second half given how much risk still remains. [Link; paywall]

Read Bespoke’s most actionable market research by joining Bespoke Premium today! Get started here.

Have a great weekend!

The Bespoke Report — 7/8/22

This week’s Bespoke Report newsletter is now available for members.

In this week’s Bespoke Report, we’ve recapped today’s nonfarm payrolls report, provided an update on inflation trends, taken a look at sector breadth and internals, previewed the upcoming earnings season, and highlighted the recent price action in mega-caps and uber-growth stocks. To read this week’s full Bespoke Report newsletter and access everything else Bespoke’s research platform offers, start a two-week trial to one of our three membership levels.

Chart of the Day: Earnings Still In Decent Shape

Bulls Back Below 20%

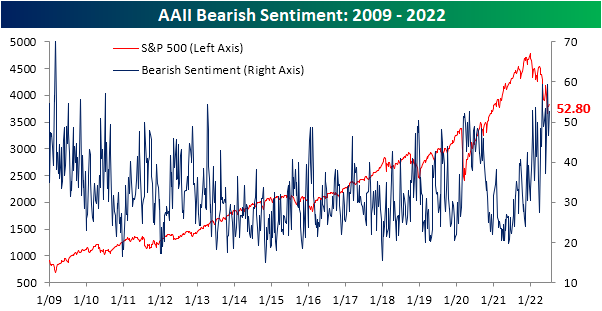

Even though the second half of June and first week of July have seen the S&P 500 climb back from its lows, sentiment appears to show that investors are not buying it. In today’s update of AAII sentiment survey, there was an overall push toward more bearish tones. For starters, the percentage of respondents reporting as bullish fell back below 20%. Even though that is not any sort of new low, this week is the fifth in a row with less than a quarter of respondents reporting as bullish. As shown in the second chart below, such a streak has been unprecedented with the last example of such an extended streak of depressed sentiment being May of 1993.

As bulls have been no where to be found, bears are plentiful with over half of respondents reporting bearish sentiment. This week’s reading came in at 52.8%, up from 46.7% last week. Mirroring bullish sentiment, that is not any sort of new pinnacle for bearish sentiment as there were even higher readings that closed in on 60% last month. Regardless, sentiment remains historically pessimistic with few other periods having seen such elevated readings for as extended of periods.

With inverse moves in bulls and bears, there is now a 33.4 percentage point gap between the two readings which is in the 2nd percentile of all readings since the survey began in 1987.

That leaves neutral sentiment to be the only normal reading of the survey. At 27.8%, neutral sentiment is in the middle of its pandemic range and only 3.6 percentage points below its historical average.

The more bearish turn at the expense of bulls witnessed in this week’s AAII survey was echoed by other readings on sentiment like the Investors Intelligence survey and NAAIM Exposure index. Combining all three of these sentiment readings into one composite, overall outlooks for the market took a further bearish turn this week with the average survey currently 1.8 standard deviations below its historical norm. That is slightly better than earlier this spring, but still, the only period since the mid-2000s with similarly pessimistic readings was in late 2008 and into 2009. Click here to learn more about Bespoke’s premium stock market research service.

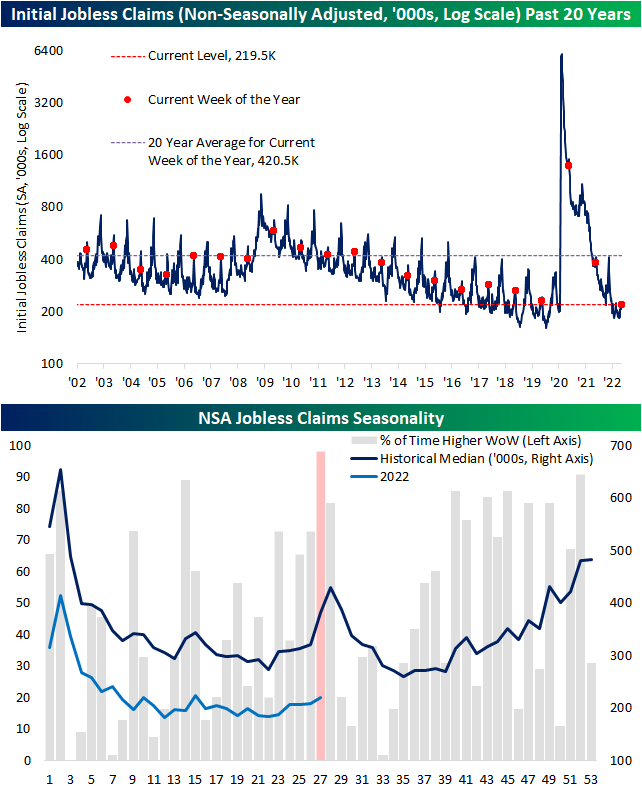

Worst Week of the Year For Claims

Initial jobless claims remain historically healthy in the low 200K range, but the most recent week’s data did mark one of the highest readings of the year. Coming off of last week’s unrevised 231K, claims rose 4K to the highest level since the second week of the year when they clocked in at 240K. That remains a much better reading than what was observed throughout much of the history of the data, but it is at the higher end of pre-pandemic readings (those from roughly 2017 through 2019).

As for the non-seasonally adjusted number, the current week of the year is essentially guaranteed to see a week-over-week increase. The current week has historically been the worst of the year in terms of week-over-week moves only having seen unadjusted claims fall once since 1967. That one decline was in 2020 when claims were working off unprecedented record highs. Given that historically consistent drift higher in claims during this point of the year, next week has historically averaged a temporary peak in claims. While that lends to the possibility of claims continuing to rise next week, the current reading is below that of comparable weeks of pre-pandemic years. In other words, claims are following standard seasonal patterns and are doing so at historically strong levels even if they have come off the absolute strongest levels of the pandemic.

Continuing claims have also begun to come off of the best levels of the pandemic. Adjusted continuing claims were expected to go unchanged at 1.328 million this week. Instead, they rose up to 1.375 million; the highest level since the week of April 22nd when claims were 12K higher. Click here to learn more about Bespoke’s premium stock market research service.

The Closer – Meaningless Minutes, Openings, Housing, Ag – 7/6/22

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we begin with a rundown of the minutes from the June FOMC meeting (page 1) followed by a look at job openings through today’s JOLTS report (page 2) and Indeed data (pages 3 and 4). We then pivot to housing data with the latest delinquency readings out of the Mortgage Monitor report from Black Knight (page 5) and realtor.com data covering inventories and prices (page 6). We then shift into the latest PMIs (page 7) before closing with a look into the declines in agriculture commodities (page 8).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

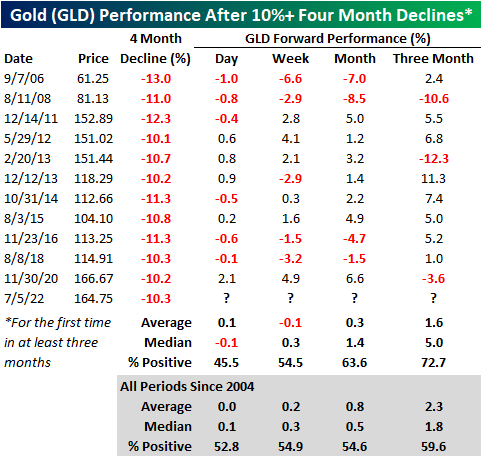

Gold Weakness

Investors often turn to Gold as a safe asset in tumultuous times, as the asset tends to hold its value during market downturns. For example, when the S&P 500 sold off by 34.1% during the COVID Crash, the SPDR Gold Trust (GLD) declined just 3.6%. In 2022, GLD initially acted as a strong hedge to the equity market, gaining 1.0% on a YTD basis on June 16th as SPY entered bear market territory. However, GLD topped out in early March and is now trading 14.0% off of its closing 2022 high. GLD has even underperformed SPY since March 8th, declining 14.0% versus SPY’s drop of 8.2%. Click here to learn more about Bespoke’s premium stock market research service.

Over the last four months, GLD has declined by 10.3%, which is elevated for a relatively stable asset during a bear market. Since its inception in 2004, GLD has declined 10% or more over a four-month period (with no occurrences in the prior three months) twelve times with each occurrence shown in the chart below.

The forward performance following four-month declines of 10%+ has been mixed depending on the time frame. The next day (which would be today), GLD has booked a median loss of 10 basis points, gaining just 45.5% of the time. However, the median return and positivity rate in the next week is inline with historical averages. Over the one and three months, performance tends to pick back up, registering gains 63.6% and 72.7% of the time, respectively. Over the next three months, GLD has had a median gain of 5.0%, which is more than two and a half times the median of all periods. Click here to learn more about Bespoke’s premium stock market research service.