European Markets Stage Comeback

While the S&P 500 remains down 18% from its all-time highs, we’ve seen some positive developments in major European markets over the last few months. As shown below, investors in Germany have recently seen the DAX enter a new bull market with a 23.7% gain off the recent lows. In local currency, the DAX is now just 8.9% below its 1/5/22 high.

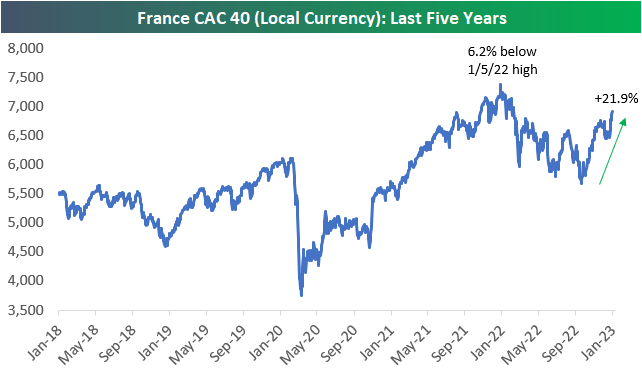

In France, the CAC 40 has also entered a new bull market with a 21.9% gain off the lows, leaving the index just 6.2% below its 1/5/22 high.

Finally, just today in the UK, the FTSE 100 traded to a four-year high after gaining 13.1% off its late 2022 low. From a technical perspective, this clearing above resistance that formed from four major highs going back to 2019 is quite notable. Within US equities, one of the main questions investors face is whether the October lows will hold in 2023, but in Europe, investors are shifting their focus and asking if 2023 will be a year of new highs. Click here to learn more about Bespoke’s premium stock market research service.

Short-Term Treasury Yields Provide the Tell

The yields on short-term Treasuries have been offering up some important tells recently. Below we highlight the yields on 6-month, 12-month, and 2-year Treasuries over the last 12 months. After trading with a positively sloped curve (the longer the duration, the higher the yield) through the first half of 2022, the yields on all three began to converge in late July/early August. In November, the 2-year yield started to drift lower, while yields on the 6-month and 12-month held firm. And just in the last week or so, we’ve seen the yield on the 12-month start to drift lower as well, while the yield on the 6-month has ticked slightly higher. As things stand now, the 2-year yield is at 4.18%, the 12-month is at 4.66%, and the 6-month is at 4.82%. This means the 2-year is inverted with the 6-month by 64 basis points, while the 12-month is now inverted with the 6-month by 16 basis points.

Yields on these three Treasuries are telling investors (and the Fed) where “the market” expects the Fed Funds Rate to be over the duration of the maturities. Right now the market expects rates to peak at some point in mid-2023 before ultimately pulling back. The fact that no points on the Treasury curve are currently above 5% tells you what the market thinks about the Fed’s unanimous support of getting the Fed Funds Rate above 5% and holding it there. It’s not buying it. While “the market” sees inflationary indicators falling pretty much everywhere it looks, Fedspeak has so far been unwilling to acknowledge any meaningful progress. The more inverted we see longer duration yields become with the 6-month T-Bill, the more damage the hawkish Fedspeak will become. Click here to learn more about Bespoke’s premium stock market research service.

Chart of the Day – ISMs On The Decline While Job Growth Holds Up

Bespoke’s Morning Lineup – 1/9/23 – Follow Through

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The finest steel has to go through the hottest fire.” – Richard Nixon

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

It’s a merger Monday to start the week with three relatively small deals by today’s standards. In the biotech space, CinCor (CINC) will be acquired by AstraZeneca (AZN) in a deal that could be valued at up to $1.8 billion while Albireo (ALBO) will be acquired by Ipsen for just under $1 billion. Both of those stocks are trading up 90% or more in the pre-market. Outside of biotech, software company Duck Creek Technologies will be acquired by Vista Equity Partners for $19 per share in cash ($2.6 billion). While the deal represents a 46% premium to Friday’s closing price, it’s worth noting that DCT traded for just under $60 per share in early 2021. So, the price of the deal is still less than a third of where it once traded during the height of the mania in software stocks.

Along with the deal activity, futures are seeing some follow-through from Friday’s big rally, and growth stocks are leading the move higher with Nasdaq futures trading up just over 0.5%. Some of the reasons for optimism this morning include reports that China has removed all of its border restrictions and that the saga to elect a Speaker of the House is finally behind us. Yields are slightly higher on the long end of the curve, and it’s a quiet day on the economic calendar.

Friday’s rally for the bulls was a nice respite from what had been some disappointing sessions. On the positive side, it was nice to see the S&P 500 finally break out of what had been a nearly two-week very tight trading range- and not break out of that range to the downside! For all the optimism about the rally, it’s still important to note that the S&P 500 wasn’t even able to close out the week above its 50-day moving average (DMA). Late in the day Friday, it attempted to take out that level but pulled back modestly into the close after briefly touching it.

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Bespoke Brunch Reads: 1/8/23

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, join Bespoke Premium with a 30-day trial!

State & Local

The Circus Came to Town—and Bought the Place by Kirsten Grind (WSJ)

A company that operates lewd performances on the Las Vegas strip has bought an entire town on the edge of the Mojave desert. Plans for the purchase remain foggy at best. [Link; paywall]

U-Haul Growth States of 2022: Texas, Florida Top List Again (U-Haul)

Trucks and trailers in the U-Haul rental fleet are flowing out of California, Illinois, and New York while Texas, Florida, the Carolinas, and the broader Sunbelt receive the lion’s share of flows. [Link]

Scams

Twitch Streamer and NFT Founder DNP3 Admits to Gambling Away Investor Funds by Rosie Perper (Coindesk)

A personality who made his name on Twitch and launched several crypto projects has admitted to literally gambling away customer funds. [Link]

The Lottery Lawyer Won Their Trust, Then Lost Their Mega Millions by Simon van Zuylen-Wood (Bloomberg)

The rise and fall of a Long Island lawyer with an impressively specific practice: catering to the legal needs of lottery winners. [Link; soft paywall]

Retail

Walgreens executive says ‘maybe we cried too much last year’ about theft by Gabrielle Fonrouge (CNBC)

The CFO of Walgreens cited a significant drop in the “shrinkage” rate of lost inventory after a failed effort at hiring security guards and an admission that management may have “cried too much last year”. [Link]

Labor Markets

FTC Proposes Rule to Ban Noncompete Clauses, Which Hurt Workers and Harm Competition (FTC)

The Biden Administration has proposed a new rule that would ban noncompete agreements. The agreements have already been restricted by numerous states and in specific instances through federal regulation. [Link]

Bond Markets

Global negative-yielding debt wiped out by Japan policy shift by Tommy Stubbington (FT)

Rate hikes, guidance changes, and a global bond market selloff have driven the stock of negative yielding debt from a December 2020 peak of more than $18trn to nothing. [Link; paywall]

Supply Chains

Dell looks to phase out ‘made in China’ chips by 2024 by Cheng Ting-Fang (Nikkei Asia)

In an effort to prevent geopolitics from disrupting the flow of chips into PCs, Dell is getting rid of Chinese suppliers for chips entirely. [Link; soft paywall]

Monetary Policy

Why We Missed On Inflation, and Implications for Monetary Policy Going Forward by Neel Kashkari (Federal Reserve Bank of Minneapolis)

Kashkari makes the argument that bad forecasting was driven by an under-estimate of how significant shocks can be for inflation. [Link]

EVs

The Secret That Explains the Price of the Cheapest Tesla by Tom Randall (Bloomberg)

Unlike traditional auto OEMs, Tesla regularly changes prices for its various models depending on demand and costs. This article discusses why. [Link; soft paywall]

Sports

Pickleball popularity exploded last year, with more than 36 million playing the sport by Jessica Golden (CNBC)

Enthusiasm is building for the cheap, accessible, and low impact sport of pickleball, which is gaining fans and players at an unprecedented rate across the country. [Link]

Read Bespoke’s most actionable market research by joining Bespoke Premium today! Get started here.

Have a great weekend!

The Bespoke Report — Equity Market Pros and Cons — Q1 2023

This week’s Bespoke Report is an updated version of our “Pros and Cons” edition for Q1 2023.

With this report, you’re able to get a complete picture of the bull and bear case for US stocks right now. It’s heavy on graphics and light on text, but we let the charts and tables do the talking!

On page three of the report, you’ll see a full list of the pros and cons that we lay out. Slides for each topic are then provided on page four and beyond.

To read this report and access everything else Bespoke’s research platform has to offer, start a two-week trial to Bespoke Premium.

Bespoke’s Morning Lineup – 1/6/23 – And the Number is…

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The telegraph would bind man to his fellow-man in such bonds of amity as to put an end to war.” – Samuel Morse

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

In what has been an overall trend of weaker economic data, the monthly non-farm payrolls report has been an oasis. Heading into this morning’s report, the headline reading had come in better than expected for a record eight straight months, and this morning’s stronger-than-expected report extends the streak to nine. The only notable current streak we can think of that has gone longer is the 11 unsuccessful votes to elect a Speaker of the House.

While the headline reading has enjoyed a record streak of better-than-expected readings, the trend heading into this month and which still remains in place is one of weaker momentum. As shown in the chart below, while readings have been positive for the last two years, they have generally been trending lower. Combining the streak of better-than-expected readings with the actual readings in the total number of jobs created, economists were correct in forecasting a slowdown in job growth, but they overestimated the pace of it.

Not only that, but average hourly earnings and the length of the average workweek both came in weaker than expected.

Heading into this morning’s report, other indicators of employment that we saw earlier this week, including the ADP Private payrolls and jobless claims, investors were gearing up for a hot number this morning. The fact that the headline reading only came in 20K above expectations and that wage growth was weaker than expected are both modest positives.

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Bespoke’s Consumer Pulse Report — January 2023

Bespoke’s Consumer Pulse Report is an analysis of a huge consumer survey that we run each month. Our goal with this survey is to track trends across the economic and financial landscape in the US. Using the results from our proprietary monthly survey, we dissect and analyze all of the data and publish the Consumer Pulse Report, which we sell access to on a subscription basis. Sign up for a 30-day free trial to our Bespoke Consumer Pulse subscription service. With a trial, you’ll get coverage of consumer electronics, social media, streaming media, retail, autos, and much more. The report also has numerous proprietary US economic data points that are extremely timely and useful for investors.

We’ve just released our most recent monthly report to Pulse subscribers, and it’s definitely worth the read if you’re curious about the health of the consumer in the current market environment. Start a 30-day free trial for a full breakdown of all of our proprietary Pulse economic indicators.

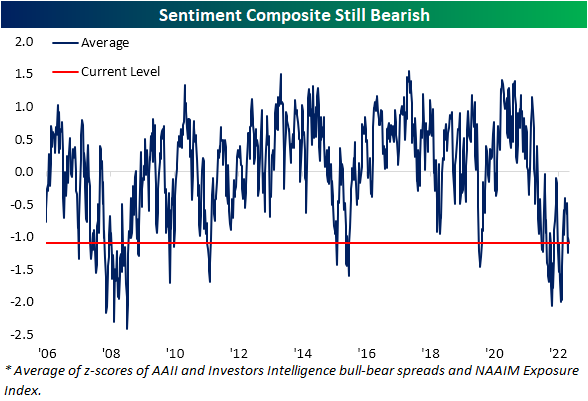

Bulls and Bears Back Off

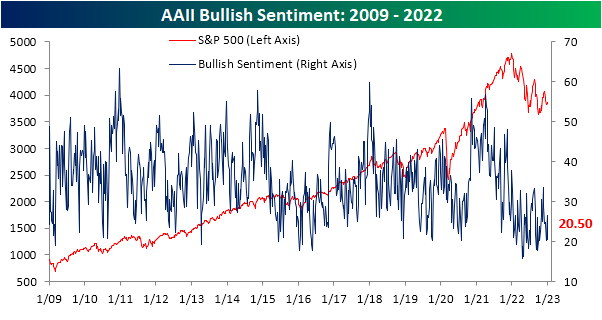

The S&P 500 has seen some choppy price action heading out of 2022 and into 2023, and that has seemed to have sent shivers down the spines of investors. Only 20.5% of respondents to the weekly sentiment survey run by AAII reported as bullish this week. That is down from 26.5% last week and is just shy of the recent low of 20.3% from two weeks ago.

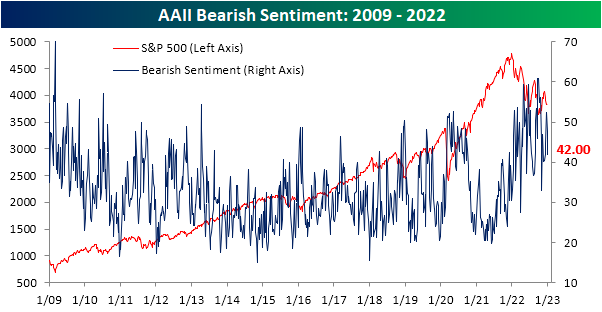

Although bullish sentiment dropped six percentage points week over week, there was not a shift to bearish sentiment as it also fell from 47.6% down to 42.0%. That is the lowest reading since December 8th.

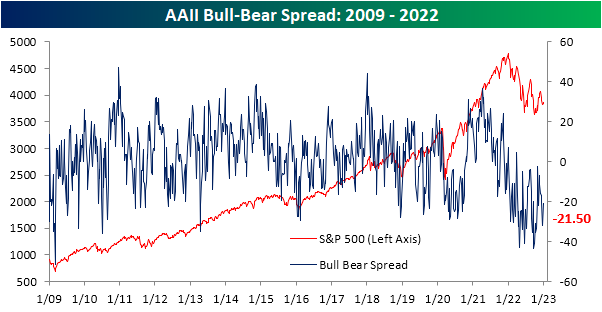

Given both bullish and bearish sentiment fell by similar amounts, the bull-bear spread moved down to -21.5, slightly below the previous week’s reading of -21.1 and extending the record streak of negative bull-bear spread readings to 40 weeks.

With both bullish and bearish sentiment falling, neutral sentiment surged to 37.5% which was the most elevated reading since the last week of March. Additionally, the 11.6 percentage point week-over-week increase was the largest since a 12.6 percentage point surge in July 2018.

Although that may sound like an impressive and notable jump, historically double-digit increases in neutral sentiment in just one week have been followed by somewhat ‘meh’ returns. Both average and median performance are worse than the norm albeit the index has moved higher more than half the time one month to one year out.

As the AAII survey continues to have an overarching negative tone, the same can be said for other surveys like the Investor’s Intelligence and NAAIM readings. Combining all three of these into a composite, this week’s reading was roughly 1 standard deviation below its historical average. While that implies sentiment is extremely bearish, that is only in the middle of the past year’s range. Additionally, we would note that this composite has been negative (meaning these indicators in aggregate are more bearish than historically normal) for a full year. The only other time period since at least 2006 when that was also the case was in the 54 weeks ending June 2009. Click here to learn more about Bespoke’s premium stock market research service.

Higher Claims on the Horizon?

Unfortunately for equities, between a stronger-than-expected ADP payrolls number and stronger-than-expected jobless claims data, today’s data showed some strength in the US labor market. Honing in on the weekly claims print, initial claims dropped all the way down to 204K this week. That marked a 19K decline from last week’s 2K downwardly revised level of 223K and brings claims to the lowest level since the last week of September when we last saw a sub-200K print. Expectations were calling for the reading to go unchanged from the unrevised level of 225K from last week.

Even continuing claims improved falling to 1.694 million instead of the forecasted increase to 1.728 million. Last week’s reading of 1.71 million had been the highest since February 2022 as continuing claims have steadily risen (at a pace consistent with past recessions) in the past several months.

Although both initial and continuing claims had strong showings, there is the caveat that the current period was smack dab in the middle of the holidays. For starters, that could have some impact on the weekly seasonal adjustment, but more importantly, we would note that those are some of the weeks of the year most prone to revisions.

In the chart below, we show the median revision (expressed as an absolute percent change from the first release) for each week of the year since 1997. The final week of the year has typically experienced a revision of +/-3.8%, tying the week of the July 4th holiday for the largest revision of the year. That means that while claims did show improvement this week, it might not be worth reading too deep into that single number. Further data will be beneficial to help confirm this print (via revisions or lack thereof) as well as provide a clearer picture of the trend, which had been one of deterioration leading into the end of the year.

One other slightly more anecdotal factor worth noting on the stronger-than-expected jobless claims data is that the strong reading this week has gone contrary to the number of layoffs that have made their way into headlines lately. Although the company initially announced the layoffs back in November, Amazon (AMZN) announced today that it plans to lay off a higher number of employees than previously stated (18K versus 10K originally). That also follows an announcement of a significant reduction of roughly 10% of the workforce of Salesforce (CRM) yesterday.

Over the past few months, news story mentions (in data aggregated from Bloomberg) of things like job cuts, firings, and layoffs have surged reaching a high of 16.5K on a four-week rolling average basis in November (around the time of Amazon’s initial announcement). Although that reading has pulled back in the several weeks since then, news counts on the topic remained elevated through the end of 2022 and are likely to get a further bump with this week’s headlines. Over the past decade, these story counts have generally followed the path of both initial and continuing claims. More recently, however, there has been somewhat of a divergence with story counts far outpacing actual claims figures.

That divergence could be for an array of reasons such as workers are quickly finding other roles and not needing to apply for unemployment insurance, but another thing to consider is the timing of the announcement of layoffs versus when they actually happen. For example, in the case of Amazon, while the initial announcement was all the way back in November, those cuts were not planned to go into effect until mid-January. In other words, while not in the data now, higher claims may very well be on the horizon. Click here to learn more about Bespoke’s premium stock market research service.