Bespoke’s Morning Lineup – 7/27/22 – If Only Every Day Was a Rate Hike Day

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Learning to fly is not pretty but flying is.” – Satya Nadella

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

We’re nearly halfway through what has been billed as the most critical week of earnings season, and based on where futures currently reside, equities are down just marginally on the week. Don’t rest yet, though. Between today’s FOMC meeting, tomorrow’s GDP report, and some critical earnings reports on Friday, we still have a number of potential bumps on the horizon. Economic data released so far today has been better than expectations, and the only report left on the calendar is Pending Home Sales at 10 AM.

Today’s Morning Lineup discusses earnings news out of Europe and the Americas, a preview of the FOMC announcement today, economic data from around the world, and much more.

One of the primary reasons stocks have put up miserable performance numbers this year stems from the tighter monetary policy of the Federal Reserve. For that reason, we found it ironic that on all three days the FOMC has hiked rates this year, stocks rallied. On 3/16, the Fed kicked off the current rate hike cycle with a 25 bps increase in the Fed Funds rate, and in response, the S&P 500 rallied 2.2%. Seven weeks later, the size of the rate hike doubled, but stocks still rallied with the S&P 500 surging just under 3% in what turned out to be the second-best day of the year. Six weeks later on 6/15, in response to the mirage of surging inflation expectations in the Michigan sentiment report, the Fed dropped a 75 bps hike on the market and yet stocks still managed to rally with the S&P 500 rising 1.5%.

In other words, the S&P 500 is down 17.7% this year, but if you had only invested in the market on days when the FOMC hiked rates, you would be looking at a YTD gain of 6.8% in just three days. Conversely, if you had avoided the market on those three days and been long the rest of the year, you’d be down 23% YTD. Nobody ever said the market had to make sense.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

The Closer – Big Tech, Home Price Cuts, 5y Sale – 7/26/22

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we begin with a recap of the busy night of earnings including a couple of megacaps: Microsoft (MSFT) and Alphabet (GOOGL) (page 1). Next, we provide an update on the rise in rates volatility and other credit market developments (page 2). Switching over to macro data, we give a rundown of new home sales (page 3) and home prices (page 4). Afterward, we update our Five Fed Composite with the addition of the Richmond Fed’s Survey (page 5) before closing out with an overview of the 5 year auction (page 6).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Daily Sector Snapshot — 7/26/22

B.I.G. Tips – Another Bad Day For the Economy

Bespoke Stock Scores — 7/26/22

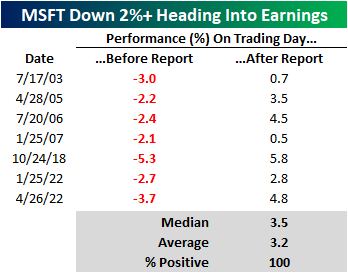

Alphabet and Microsoft Down Headed Into Earnings

Both Microsoft (MSFT) and Alphabet (GOOG) are trading down over 2% heading into their earnings report amidst broader market weakness and wariness towards the tech sector. On a year-to-date basis, MSFT and GOOG are both down over 25% and are trading near their 52-week lows. The charts below show MSFT and GOOG over the last twelve months. On the bright side, the rate of change in the two stocks does appear to have support near current levels. However, they are both still in sustained downtrends. Click here to learn more about Bespoke’s premium stock market research service.

Since GOOG went public in 2004, there have only been four days in which the stock traded lower by two percent or more heading into the earnings report. The latest occurrence was on the day of the Q1 2022 report, which was the only time when it also reacted negatively following the earnings report. On average, the stock has gained 2.5% (median: 2.6%) following the report after trading lower by 2%+ leading into earnings. Historically speaking, GOOG has posted gains on its earnings reaction day 58% of the time, gaining an average of 1.7%. While the average and median returns below are positive, we would note that with just four occurrences the sample size is small.

Since October of 2001 (which is as far back as our earnings database goes), MSFT has traded lower by at least two percent in the session heading into an earnings report seven times. Again, the sample size is relatively small, but following every one of these prior occurrences, MSFT gained in the session following its earnings report, booking an average gain of 3.2% (median: 3.5%). For all earnings reports since October of 2001, MSFT has reacted positively to earnings 60% of the time. Click here to learn more about Bespoke’s premium stock market research service.

Chart of the Day – Hikes Spike the S&P

Bespoke’s Morning Lineup – 7/26/22 – Walmart (WMT) Comes Out of Left Field

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“A good thing never ends.” – Mick Jagger

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

We said it was going to be a busy week yesterday, and that didn’t even include the surprise earnings warning from Walmart (WMT) after the close. While WMT shares are down sharply, it’s surprisingly having little impact on the broader markets where futures are only modestly lower heading into the open. Where they finish the day will be another story, and then after the close, we’ll hear from Alphabet (GOOGL) and Microsoft (MSFT) which are likely to have a bigger impact on how markets trade tomorrow.

Outside of equities, longer-term Treasuries are rallying this morning and sending the 10-year yield down to 2.74% and flattening the 10y3m portion of the yield curve down to just 26 basis points (bps) and closer to inverted levels, but don’t worry “it’s different this time”. As mentioned above, WMT’s warning was somewhat out of left field, and the timing was interesting as it came right before this week’s Fed meeting. It will be interesting to see what, if any, impact the WMT news has on the thoughts of FOMC members.

Today’s Morning Lineup discusses earnings news out of Europe and the Americas, the geopolitical impacts of Pelosi’s planned visit to Taiwan, economic data from around the world, and much more.

First, it was Target (TGT) in May, but yesterday it was WMT’s turn to issue a rare earnings warning outside of its regularly scheduled quarterly earnings report. As noted in last night’s Closer, the company noted that “increasing levels of food and fuel inflation are affecting how customers spend, and while we’ve made good progress clearing hardline categories, apparel in Walmart U.S. is requiring more markdown dollars”. In response to the warning, shares of the retailer plunged close to 10%, and if those levels hold into the opening bell, it will be the stock’s largest downside gap since the 1987 Crash. Including today’s decline at the open, today will be WMT’s second downside gap to make the top ten (since 1985) this year. The only other year with two entries on the list is 2020 in the middle of the COVID crash. There weren’t even two declines of similar levels during the Financial Crisis!

Looking at the chart below, it’s amazing to see how strong WMT was in the late 1980s and 1990s only to stall out, relatively speaking, at the turn of the century. Including dividends, WMT stock has had an annualized return of 4.32% from 12/31/99 through the opening bell today compared to the S&P 500’s gain of 6.5% over that same period.

While the largest downside gap since the 1987 crash may seem a bit excessive, keep in mind that as of yesterday’s close (before the warning was released), WMT was only down about 8% YTD and trading at a premium to the S&P 500 as investors viewed it as a port in the storm. At the opening bell today, WMT will be down less than 18% YTD, which is only slightly weaker than the S&P 500, with a valuation much closer to inline with the broader market. In bear markets, there are no ports.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

The Closer – Weak Growth, Lowered Guidance – 7/25/22

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we start out with a recap of tonight’s earnings reports (page 1) followed by a dive into our latest update of our Five Fed Composite with the addition of the Dallas Fed (page 2). Next, we provide a rundown of the latest release of the Chicago Fed’s National Activity Index (page 3). We close out with a recap of this afternoon’s 2 year note auction and preview the remainder of July Treasury issuance (page 4). We then update the latest positioning data (pages 5 – 7).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!