Thankful, Not Thankful 2022

Between travel delays, crowded stores, delayed deliveries, and unhealthy eating and drinking habits, there’s a lot not to like about the holidays. But all of these pale in comparison to the quality time spent with family and friends and the new memories we make each year. Within a few months, you won’t even remember the traffic jam on the way to dinner or that you had to wait until January to get the iPhone 14 Plus. What you won’t forget, though, are the family football games, hanging around the fire, one of ‘those’ stories from your aunt or uncle, a post-dinner game of salad bowl, or that late-night McRib run to McDonald’s with the cousins who are old enough to drive (but not old enough to drink). These are the things in life that really matter.

There has been no shortage of things to complain about in the market and economy this year, but it could be worse, and not everything has been horrible. This Thanksgiving, we are introducing our list of market and economic-related things not to be thankful for this year, but more importantly, what we also have to be thankful for. Enjoy the rest of your weekend! Click here to learn more about Bespoke’s premium stock market research service.

Chart of the Day – Inverted Yield Curves: Not Just a US Phenomenon

Bespoke’s Morning Lineup – 11/25/22 – Half Day

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“If you cannot get rid of the family skeleton, you may as well make it dance.” – George Bernard Shaw

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

We hope everyone had an enjoyable Thanksgiving, and if you have the day off today, we hope you enjoy the long weekend. US equity markets are open but for a half session with trading for the week ending at 1 PM Eastern. Futures are mixed on the session so far with the Dow indicated higher and the Nasdaq trading lower. Shares of Apple (AAPL) are down nearly 1% in the pre-market as workers at Foxconn plants in China have been staging protests over pay and working conditions. The company has even had to offer bonuses of up to a month’s pay to employees willing to quit and board buses to go back home.

In terms of data today, there is none to speak of on either the economic or earnings front. European markets are little changed this morning but with a positive bias. Over in Europe, Q3 GDP was slightly stronger than expected, but Consumer Confidence came in weaker than expected and missed expectations for the 9th time in the last ten months.

Through the first three trading days of this week, the S&P 500 was up 1.56%. For a typically positive week, a gain of this magnitude is strong even for Thanksgiving week and ranks as the 13th best week-to-date performance through Wednesday of Thanksgiving week since 1945. As we noted in a post earlier this week, the majority of the gains from Thanksgiving week typically come on Wednesday and Friday. The S&P 500’s median performance on the Friday after Thanksgiving has been a gain of 0.24% with positive returns two-thirds of the time. In years where the S&P 500 was up over 1% on the week heading into Thanksgiving, the median gain was even stronger at 0.36% compared to a gain of just 0.15% on all other Thanksgiving Fridays. Even more notable is the consistency of positive returns. In those weeks where the S&P 500 was up 1%+ in the first three trading days of the week, the S&P 500 traded higher on Friday 87.5% of the time. On all other Thanksgiving Fridays, however, the S&P 500 was higher barely more than half of the time.

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

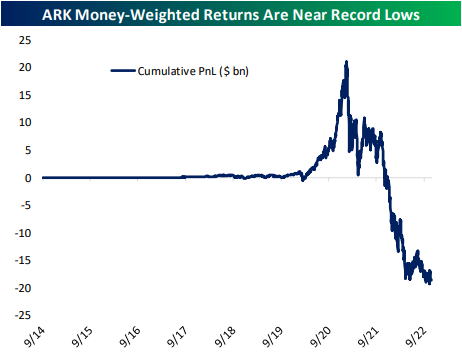

The Closer – Doves Arrive, ARK Flows, Durable Goods, New Home Sales, EIA – 11/23/22

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we begin tonight with a look at what tones were present in today’s minutes. We also check in on flows for the ARK ETF complex (page 1). Next we recap today’s durable good orders numbers (page 2) followed by a rundown of new home sales (pages 3 and 4). We finish with a look at the latest EIA data (page 5).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Bespoke’s Weekly Sector Snapshot — 11/23/22

Chart of the Day: Breadth Intrigue

Continuing Claims Flash Recessionary Warning

Due to tomorrow’s holiday, this week’s jobless claims data was released a day early and were not exactly a release to be thankful for. The latest readings were bad all around with both initial and continuing claims rising more than expected. For initial claims, last week’s level was revised up by 1K to 222K, and this week’s reading rose by 18K to 240K. That is the highest level of claims since the week of August 18th, and the sequential increase was the largest since the end of September. Whereas recent readings on jobless claims have been healthy in the sense that they have remained within the range of low readings from the few years prior to the pandemic, this new high would have been at the high end of the 2008 to 2019 pre-pandemic range.

On a non-seasonally adjusted basis, the current week of the year typically sees claims move higher with a week-over-week increase 82% of the time. However, this week’s increase was around 10K larger than what the comparable week of the year has historically averaged. In other words, from a seasonal perspective, the rise in claims is perfectly normal in terms of direction but less so in terms of size. Now at 248K, claims are in line with levels for the comparable weeks in 2021 and 2019.

Continuing claims continue to be the more interesting story around jobless claims. Delayed one week to the initial claims number, continuing claims as of the week of November 11th rose for a sixth week in a row. As we noted last week, such a streak of consistent increases in continuing claims has been rare, especially in the years following the Global Financial Crisis. In fact, the rise during the onset of the pandemic in 2020—which lasted for 10 consecutive weeks—was the only other notably lengthy streak post-2009. Prior to that, there have only been a handful of other times in which continuing claims have risen for 10 weeks or more.

As for the current rise in claims, the latest increase leaves the reading at 1.551 million which is the highest level since the first week of March. From a historical perspective, though, that remains an impressively low reading and well below the pre-pandemic range even if it is rapidly deteriorating.

As for just how bad of a stretch it has been for continuing claims, the 187K increase, or 13.7% jump, during the past six weeks would be by far the largest in over a decade outside of the start of the pandemic. Additionally, such a large increase in the span of six weeks is consistent with increases from all prior recessions. In fact, as claims have made their way off of historic lows, the current increase is nearly the same size as the early 1990s recession and is even larger than those in the early 1980s and early 2000s. Click here to learn more about Bespoke’s premium stock market research service.

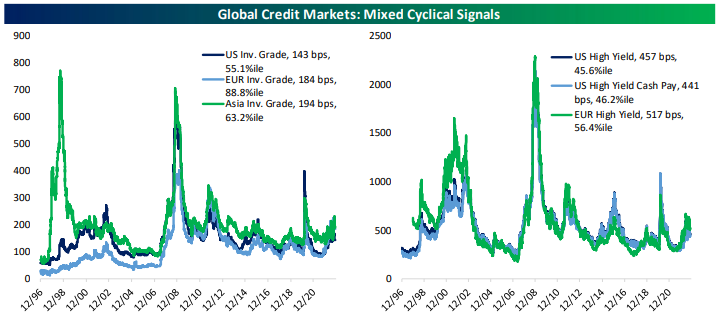

Fixed income Weekly: 11/23/22

Searching for ways to better understand the fixed income space or looking for actionable ideas in this asset class? Bespoke’s Fixed Income Weekly provides an update on rates and credit every Wednesday. We start off with a fresh piece of analysis driven by what’s in the headlines or driving the market in a given week. We then provide charts of how US Treasury futures and rates are trading, before moving on to a summary of recent fixed income ETF performance, short-term interest rates including money market funds, and a trade idea. We summarize changes and recent developments for a variety of yield curves (UST, bund, Eurodollar, US breakeven inflation and Bespoke’s Global Yield Curve) before finishing with a review of recent UST yield curve changes, spread changes for major credit products and international bonds, and 1 year return profiles for a cross section of the fixed income world.

In this week’s report, we take a look at the risk premiums currently reflected in credit spreads.

Our Fixed Income Weekly helps investors stay on top of fixed-income markets and gain new perspectives on the developments in interest rates. You can sign up for a Bespoke research trial below to see this week’s report and everything else Bespoke publishes free for the next two weeks!

Click here and start a 14-day free trial to Bespoke Institutional to see our newest Fixed Income Weekly now!

Bespoke’s Morning Lineup – 11/23/22 – Full Plate of Data

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Those who previously claimed they were too old or ill to work embraced the idea of private property once they could enjoy the fruits of their own labor.” – Caroline Baum, “The Story of Thanksgiving – and Proper Incentives”

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

Investors may be thinking ahead to the Thanksgiving holiday and spending time with friends and family, but there is still a full-day left of trading ahead of us. The earnings calendar is light as Deere (DE) has been the only report on the calendar, but there’s plenty of economic data to tide you over as we try to jam three days worth of reports into one day. Things kick off at 8:30 with Durable Goods and Initial Claims. At 9:45, S&P will release flash PMI readings for the manufacturing and services sector, and then at 10 AM, we’ll get Michigan Sentiment and New Home Sales. Not enough for you? OK. Well, how about we cap it off with some FOMC Minutes at 2 PM? Is that enough for you?

Futures are technically in the green this morning, but they’re pretty much unchanged, and we’ve seen a number of ticks this morning where they were actually unchanged. The same is true in Europe where trading has been uneventful. Economic data in the region, however, has been positive as flash PMI readings for both the manufacturing and services sectors came in higher than expected for the entire Eurozone as well as Germany, the UK, and France individually.

Which of these indices is not like the other? As technicians attempt to divine whether the S&P 500 and other major US equity benchmarks will be able to break above its 200-DMA in this current leg higher, it seems out of place to be talking about the DJIA breaking out to six-month highs. Heading into the Thanksgiving holiday, the DJIA has rallied more than 19% off its Q3 low and is already more than 5% above its 200-DMA. The DJIA isn’t often thought of as a leading indicator for the broader market, but more than a few 401k plans have hopes that the rest of the indices play follow the leader.

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

The Closer – New Highs, UST Volume, Auction Allocations, Business In – 11/22/22

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we start out tonight with a look at equities’ new highs and whether or not high yield confirmed the move (page 1). We then take a look at volumes for this point of the year for Treasuries (page 2) followed by a 7 year note auction recap (page 3) and a look at the latest allotment data (pages 4 and 5). Next, we review the latest non-manufacturing data from the Philly Fed’s (page 6 and 7) before pivoting to an update of our Five Fed Manufacturing Composite (page 8). We close out with the EIA’s monthly update of energy production and consumption.

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!