The Closer – Weighting, Expectations, Logistics Looking Up – 7/7/26

Log-in here if you’re a member with access to the Closer.

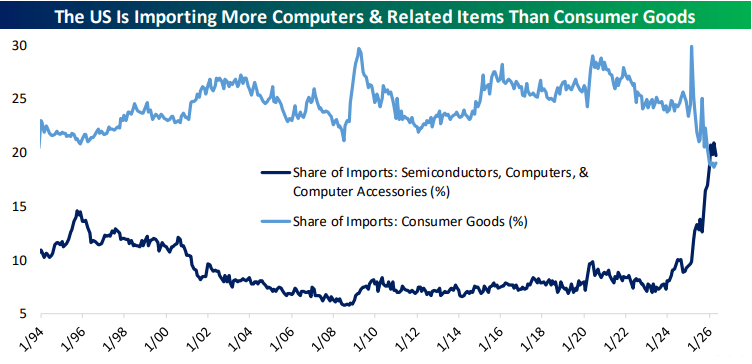

- The US goods imports composition has shifted to a shocking degree over the last two and a half years as imports of semiconductors, computers, and accessories have more than tripled.

- One year consumer inflation expectations have risen to their highest level since September 2023, despite big drops in categories like food and gas.

- Logistic managers have reported robust industry conditions in part due to prices rising at some of the fastest paces on record.

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Daily Sector Snapshot — 7/7/26

Chart of the Day – Economic Momentum

Bespoke’s Morning Lineup – 7/7/26 – Taking it to the Bank

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“You win a few, you lose a few. Some get rained out. But you got to dress for all of them.” – Satchel Paige

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Paul Hickey will be appearing on CNBC’s The Exchange today between 1 PM and 1:30 PM. Check it out if you’re near a screen!

It looks like a terrible Tuesday for the market as Nasdaq futures fall more than 1%, while the S&P 500 faces a more modest loss of 0.23%, and futures on the Dow are modestly higher. Despite the weakness in equities, Treasury yields are slightly higher, with the 10-year hitting 4.5%.

Crude oil is modestly higher after reports that Iran fired munitions at a cargo ship in the Strait of Hormuz. That raises levels of uncertainty for the region, but with WTI prices not even able to muster a 1% gain, markets don’t seem overly concerned. The fact that gold prices and Bitcoin are also lower by less than 1% also supports that idea.

The weakness in US futures traces back to weakness overnight in Asia, where the Nikkei fell over 2%, and South Korea’s Kospi plunged nearly 5%. The weakness in South Korea was tied to memory stocks, which plunged as Samsung declined close to 10% after the company said earnings wouldn’t be quite as stellar as previously thought.

In Europe, stocks are holding up much better. The STOXX 600 is down just 0.2% as world leaders meet for a NATO Summit. German stocks are the biggest laggards, falling more than 0.7% even as May Industrial Production rose 0.9%, versus expectations for an increase of 0.1%. Outside of Germany, most other major benchmarks in the region are modestly higher.

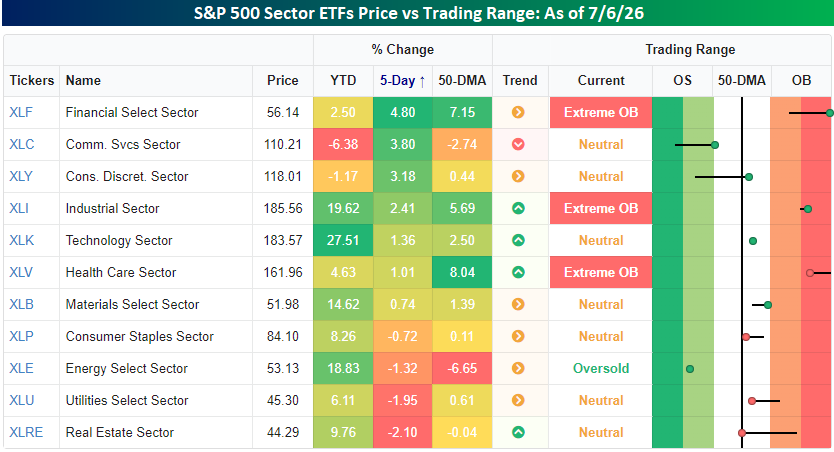

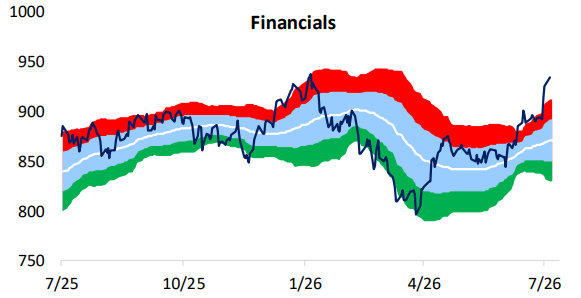

As tech stocks struggle to kick off Q3, Financials have picked up some of the slack. Over the last five trading days (dating back to the start of last week), the sector is up close to 5%. That makes it the top-performing sector, with a rally of a full percentage point higher than the next closest sector (Communication Services), and more than 1.5 percentage points ahead of Consumer Discretionary. As a result of the rally, the sector is more overbought than any other, as it closed more than three standard deviations above its 50-DMA yesterday.

With the rally over the last few days, the Financials sector is back more than three standard deviations above its 50-day moving average, a level it reached back in early June. For more on how the sector has historically performed after reaching such extreme short-term overbought levels, see our Chart of the Day from June 17th (Chart of the Day – Cyclical Surge)

Start a two-week trial to Bespoke Premium to continue reading today’s full Morning Lineup.

The Closer – Record Crack Spread, Sentiment Surge, Housing – 7/6/26

Log-in here if you’re a member with access to the Closer.

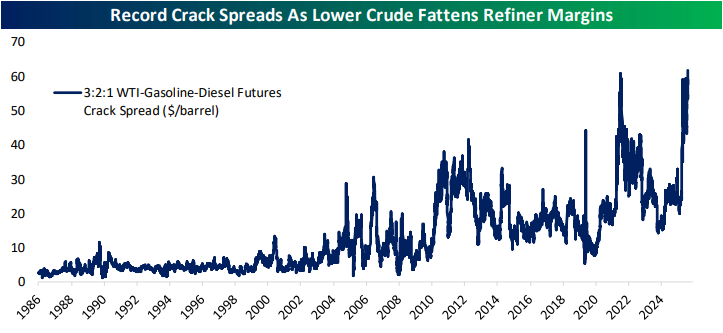

- As crude prices remain in the $60 range and gasoline prices stay stubbornly high, crack spreads have widened out to record levels.

- The Schwab Trading Activity Index readings a multi-year high in June despite the S&P 500 small pullback during the month.

- Housing inventories continued to grow in June although the median listing price is down to the lowest level since April 2022.

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Daily Sector Snapshot — 7/6/26

Chart of the Day: Mega Bounce

Bespoke’s Mid-Year 2026 Investor Sentiment Report

In mid-December 2025, we sent Bespoke’s client base a survey to capture the current thinking of experienced investors on markets, the economy, policy shifts, and portfolio positioning heading into 2026 and beyond.

As a follow-up to our year-end survey, we sent clients our Mid-Year 2026 Investor Survey in the last two weeks of June.

You can read Bespoke’s Mid-Year 2026 Investor Sentiment report by signing up for any of our three membership levels below. Enter the coupon code “OUTLOOK” at checkout for a 20% discount on your first charge. You can review our membership levels here to help make your decision.

Bespoke Newsletter Monthly Payment Plan

Bespoke Newsletter Annual Payment Plan

Bespoke Premium Monthly Payment Plan

Bespoke Premium Annual Payment Plan

Bespoke All Access (Bespoke Institutional) Monthly Payment Plan

Bespoke All Access (Bespoke Institutional Annual Payment Plan

Matrix of Economic Indicators – 7/6/26

Our Matrix of Economic Indicators provides a concise summary analysis of the US economy’s momentum. We combine trends across the dozens and dozens of economic indicators in various categories like manufacturing, employment, housing, the consumer, and inflation to provide a directional overview of the economy.

To access our newest Matrix of Economic Indicators, start a two-week free trial to either Bespoke Premium or Bespoke Institutional now!

Bespoke’s Morning Lineup – 7/6/26 – Falling SOX

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Philosophy is common sense with big words.” – James Madison

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

US futures are coming back from the holiday weekend full of life, with the S&P 500 poised to gap up 0.5% at the open while the Nasdaq rallies more than 1%. Treasury yields are lower, with the 10-year yield moving down to 4.46%. Crude oil prices have seen little movement, with WTI trading right below $69 per barrel, and gold is rallying 1% to $4,167 per ounce. In crypto, Bitcoin is down over 1% and below $62K.

Asian markets kicked off the new week on a quiet note, with Hong Kong (+1.1%) the only benchmark to move up or down by more than 1%. The Nikkei declined 0.1% while South Korea declined 0.5%. China’s Shanghai Composite was also down 0.1%.

The tone for European stocks is similarly muted, but more skewed to the downside. The STOXX 600 is trading down 0.3% in early trading. Spanish stocks are leading the losses, down 0.8%, while French stocks are unchanged. Retail sales and PPI for the region both rose 0.2% in May and were both right in line with expectations.

The only data on the calendar today are Service sector PMIs from S&P and ISM, and the earnings calendar is blank with no real notable reports until Thursday when Pepsi reports before the open.

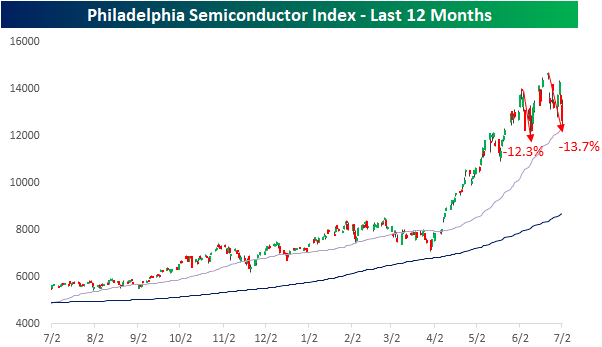

Semiconductor stocks really limped into the holiday weekend as the Philadelphia Semiconductor Index (SOX) fell 5.4% on Thursday following a 6%+ decline on Wednesday. That was the first back-to-back 5%+ declines in the index since April 2025. Those two declines alone were enough to put the SOX into correction territory, but with the index already off its highs heading into Wednesday’s session, it is now down 13.7% from its recent closing high. This current correction for the index comes less than a month after another 12.3% correction that ended in early June. Volatility in the SOX is clearly picking up.

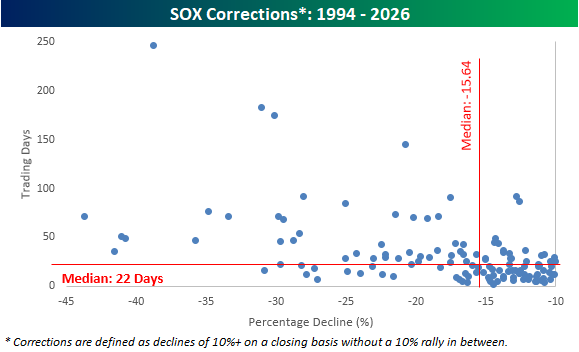

The chart below shows all 127 SOX corrections since its inception in 1994 in terms of time and price. Overall, the median correction has lasted 22 days (current correction has been 10 days) and experienced a peak-to-trough decline of 15.64%. So, the current period is less than halfway there in terms of time, but not far from the median in terms of price.

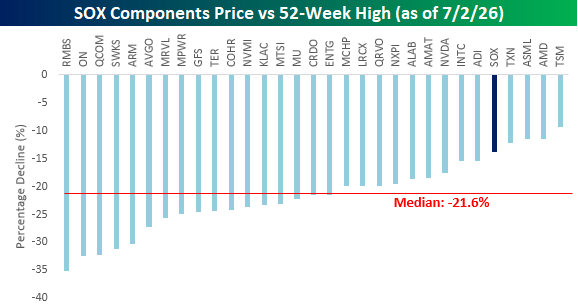

While the SOX itself is down nearly 14%, the individual stocks that make up the index have seen larger declines relative to their respective peaks. Only four of the index’s 30 components are currently in drawdowns of less than 15%, and the median decline has been 21.6%. The biggest losses have been in the shares of Rambus (RMBS), ON Semiconductor (ON), Qualcomm (QCOM), Skyworks (SWKS), and Arm Holdings (ARM), all of which are down over 30%. Nvidia (NVDA), the largest of the stocks in the index, has been a big underperformer on the way up, but on the way down, it hasn’t been quite as extreme as its current drawdown of 17.6% is four percentage points less than the median of the index’s 30 components.

Start a two-week trial to Bespoke Premium to continue reading today’s full Morning Lineup.