See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Great ideas come from everywhere if you just listen and look for them.” – Sam Walton

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

If you don’t cut out early for the holiday weekend, make sure to check out Paul Hickey on Making Money with Charles Payne today at 2 PM.

The S&P 500 is looking to extend its streak of gains to eight weeks, and futures are cooperating so far. Both the Nasdaq and S&P 500 are indicated to open 0.15% higher, although they’ve given up much of their earlier gains as crude oil rallies about 2%. Treasury yields are lower, although the 10-year yield still sits above 4.55%. Gold and Bitcoin are both down about 0.5%.

It was another positive session in Asia, as the Nikkei rallied 2.7%, taking its weekly gain to 3.1%, while South Korea rallied 0.4% to finish nearly 5% higher for the week. Chinese stocks also traded up, with the Shanghai Composite rallying 0.9% but still finishing modestly lower for the week.

The catalyst for last night’s rally was weaker-than-expected April CPI, with core rising 1.4% y/y relative to expectations for 1.7%. Also, in South Korea, the index of Consumer Confidence for May jumped from 99.2 to 106.1.

It’s been a broadly positive day for equities in Europe. The STOXX 600 is up 0.5%, taking its weekly gain to more than 2.5%. Germany is leading the way for the week with a gain of 3.4%, while Italy is up less than half a percent. These gains come despite some hawkish commentary from ECB officials concerning inflation.

The only economic report on the US calendar this morning is the Michigan Sentiment report, which continues to hang around near all-time lows even as the stock market sits near all-time highs. Also, since it’s the Friday before a holiday weekend, the bond market closes at 2 PM today, so look for activity to really dry up in the afternoon.

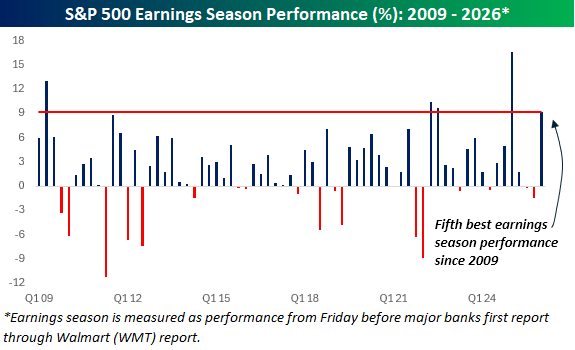

Earnings season came to an unofficial end with Walmart’s (WMT) report on Thursday, and what an earnings season it was. Heading into the reporting period, we highlighted the pace of negative revisions as a bullish contrarian signal, and it played out, as results and guidance both came in much better than expected.

From April 10th through yesterday’s close, the S&P 500 gained 9.2%, which ranked as the best earnings season (Friday before the first large banks start to report through WMT) since the same reporting period last year, coming out of the tariff-tantrum. Back then, it was a similar backdrop; amidst tariff uncertainty, companies had little incentive to give upbeat outlooks, but that’s exactly what we saw. This earnings season saw a similar story unfold, with the main difference being that tariff uncertainty was swapped out and replaced with the war in Iran.

The chart below shows the S&P 500’s performance during earnings seasons since the start of 2009, and while the market rallies an average of 2.2% during earnings season, the 9.2% gain during this earnings season ranks as the fifth best since the start of 2009. The only better ones were coming out of the financial crisis, two quarters coming out of the 2022 bear market, and finally, the Q1 earnings season last year.

Looking ahead, coming out of the unofficial start to summer next week, the S&P 500’s historical performance in the week after Labor Day has been a gain of 0.52% (median: 0.61%) with positive returns 61.8% of the time. The best post-Memorial Day week was a gain of 7.2% in 2000, which turned out to be a major false alarm, while the only two years when the S&P 500 declined 3%+ during the week were in 1973 and 2012.

Start a two-week trial to Bespoke Premium to continue reading today’s full Morning Lineup.