Morning Lineup – Better Than Expected Data in Europe; Breadth Still Positive

We’ve seen some better than expected economic data out of Europe for a change this morning as PMIs for the Services sector mostly came in better than expected. US equity futures are pointing to a slightly higher open after yesterday’s weakness. In Asia, China lowered 2019 GDP growth forecasts and President Trump is threatening to end preferential trade treatment for India and Turkey. Read all about everything driving the markets in today’s Morning Lineup.

Bespoke Morning Lineup – 3/5/19

We’ve been discussing the market’s strong breadth so far in 2019 for several weeks now, but today we wanted to provide another illustration of it. The S&P 500’s 10-Day A/D line typically oscillates between positive and negative territory on what is usually a week to week basis or at least every couple of weeks to weeks. Lately, though, it has been all positive. Through yesterday’s close, the 10-Day A/D had been positive for 39 straight trading days. That’s over eight weeks in calendar days!

These kinds of periods of consistent positive breadth don’t typically happen very often. Going back to 1990, there have only been four other periods where the 10-day A/D line was positive for longer than it has been now.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

The Closer — Lyft Hits The Market, Construction Collapse — 3/4/19

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, on a quiet day in macro data, we turn to the upcoming IPO of ride-sharing giant Lyft. We take a look at the company’s annuals and offer some forecasts as to the growth prospects. We finish with a note on today’s Construction Spending data which showed the weakest YoY growth in the post-recession period.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

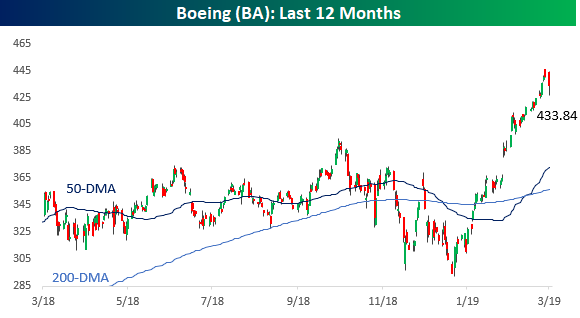

Boeing Soars

To say that Boeing shares have had a good start to 2019 would be like calling the 747 a puddle jumper. With a gain of over 50% from its late 2018 low and a YTD gain of over 36% through last Friday’s close, it has been one of the strongest starts to a year (through 3/1) for a current DJIA component in decades.

Making its move even more noteworthy is that with a share price of more than $400 and the fact that the Dow is a price-weighted index where each component’s weighting in the index is based on its share price, BA’s rally has had a ‘jumbo’ impact on the overall index. BA’s weight in the DJIA currently stands at 11.5%, while its weighting in the S&P 500, which is a market cap weighted index, is less than 1%. As a result, through Friday’s close the DJIA had gained 2,807 points so far in 2019 and BA accounted for 812 of them. That works out to 29% of the DJIA’s entire gain this year! Without BA’s rally, the DJIA would only be up about 8% this year versus its 11.5% gain through Friday. Behind BA, the next closest stock in terms of its impact on the DJIA this year has been Goldman Sachs (GS) which has accounted for 216 points of the DJIA’s YTD gain (7.7%).

As mentioned above, BA’s strong start to the year is one of the best for current DJIA components going back to 1995. Of the 30 current members, there have been just four prior occurrences where a stock rallied more than 30% YTD through the close on 3/1, and two of those were in the stock of Apple (1998 & 2005) well before it was even added to the DJIA. The only two other occurrences were Intel’s (INTC) 41% gain in 2000 just after it was added in late 1999 and then Microsoft (MSFT) the next year in 2001 when it rallied 37%. The key difference between those two occurrences and Boeing, though, is that because of their share prices at the time, they didn’t have nearly the positive impact on the overall index when they rallied.

While bulls have nothing to complain about regarding BA’s big rally this year, the impact of high price stocks on the DJIA cuts both ways. Barring any future stock splits, even just a 10% correction in shares of BA would clip the DJIA by more than 250 points.

Chart of the Day: 2019 Decile Analysis

Trend Analyzer – 3/4/19 – Fewer and Fewer Downtrends

More and more of the major US index ETFs are exiting their long-term downtrends. We are starting the week with only five currently in a downtrend as indicated by our Trend Analyzer tool. The remaining nine are trending sideways. This follows a relatively flat week with each index ETF moving less than 1%. Last week saw some mixed performance from these ETFs as most saw gains but four moved lower. The Nasdaq (QQQ) gained the most at 0.87% while the Core S&P Small Cap (IJR) just about saw the opposite declining 0.85%. Despite some pullback last week, conditions generally remain overbought, though, not at any extreme level as a number of these ETFs are less overbought than they were at the start of last week. This is especially the case for small and mid-caps which were the weakest of the group last week. This is in spite of the fact that these same names have done the best on the year. For example, we are starting the week with the Russell 2000 (IWM) up over 18% YTD. The Micro Cap ETF (IWC) is not far behind up 17.47% on a year to date basis.

This Week’s Economic Indicators – 3/4/19

February came to a close with a busy week in economic data. We got 45 releases last week with a small majority (23) coming in below expectations or the prior period. Monday saw the Chicago Fed National Activity Index miss by a wide margin. Conversely, the Dallas Fed’s Manufacturing Activity beat forecasts by a wide margin. December housing data released Tuesday was very weak in terms of Housing Starts, though, permits were a silver lining indicating better future activity. Tuesday also saw a solid increase in Consumer Confidence. Q4 GDP data was the biggest release of the week on Thursday. While it did come in lower, GDP beat expectations by 0.4%. Finally, on Friday the Markit Manufacturing PMI and ISM Manufacturing Index both came in weaker than expectations.

Coming up this week, the delayed Construction Spending data for December is the only release today, expecting a downtick. Out Tuesday are the service portions of Markit PMIs and ISM data. Also scheduled for Tuesday is New Home Sales for December—one of the final delayed releases as a result of the government shutdown. Wednesday, we will get an update on the Trade Balance as well as the Fed’s Beige Book later in the day. Q4 Nonfarm Productivity, Unit Labor Costs, and changes in household wealth as seen through the Fed’s Z.1 Financial Flows report are all out Thursday. We cap off the week with the Nonfarm Payrolls report which is expecting to show a still hot labor market.

With several more releases of December data points this week, we are just about caught up to all of the releases that had been postponed due to the government shutdown. Only two releases have yet to come out: Construction Spending and New Home Sales. Both of these will come out early this week. With the data now out, the revisions should be watched as there potentially could be some large changes in these November and December numbers.

Bespoke Morning Lineup — New Bull in China

A quick programming note — Bespoke co-founder Paul Hickey will be on CNBC this AM at 8:40 ET to discuss our market views. Be sure to tune in!

US equity futures are higher to start the week as trade tensions continue to ease. Catch up on everything you need to know ahead of the open in today’s Bespoke Morning Lineup.

Start a two-week free trial to Bespoke Premium to read our Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Bespoke Brunch Reads: 3/3/19

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, join Bespoke Premium for 3 months for just $95 with our 2019 Annual Outlook special offer.

Politics

Institutional shocks and economic outcomes: Allende’s election, Pinochet’s coup and the Santiago stock market by Daniele Girardi and Samuel Bowles (Science Direct/Journal of Development Economics)

Are violent dictatorships bad for markets? In the case of Chile, the coup overthrowing democratically elected Allende and replacing his government with a dictatorship boosted share prices by some 80%. [Link]

Here’s What Beto Could Unleash on Trump by Sasha Issenberg (Politico)

Forget the headline. This story is a much more useful analysis of dos and don’ts of scaling up an organization to very large size in a very short time than it is as a window on either the candidate in question or the outlook for 2020 elections. [Link]

Beverages

Pour One Out for the Fading American Beer Industry by Craig Giammona and Carmen Reincke (Bloomberg)

While literally every other segment of the American alcohol market is seeing robust growth, beer sales are slowing – and that’s with craft beer volumes up 15% since 2015. [Link; soft paywall]

The curious story of how transatlantic exchange shaped Italy’s illustrious coffee culture by Cosimo Bizzarri (Quartz)

The iconic Italian coffee bar serves a uniquely Italian espresso, but the walk-up method of service is something that came directly from America. [Link]

Race

‘The South Stands at Armageddon’: Breaking the Sugar Bowl color barrier by Ivan Maisel (ESPN)

The invitation of an integrated Pittsburgh Panthers squad to face Georgia Tech in the Sugar Bowl at the end of the 1956 season was a landmark drama as sports helped force integration. [Link]

Who was the real Don Shirley? Family shares dismay at portrayal in ‘Green Book’ by Hamil Harris (MSN)

Best Picture winner The Green Book came at the objection of the subject’s family, who claimed they were shut out by the makers of the film. [Link]

Economics

An MMT response on what causes inflation by Scott Fullwiler, Rohan Grey, and Nathan Tankus (FTAV)

An explanation and argument in favor of the precepts of modern monetary theory (MMT), as the subject has gained traction in broader discussions about fiscal policy. [Link; registration required]

The Paper Money of Colonial North Carolina, 1712-1774 by Cory Cutsail and Farley Grubb (University of Delaware Alfred Lerner College of Business & Economics Working Papers)

A fascinating history of the paper money issued by paper money issued by then-colony North Carolina; the story behind that monetary arrangement is fascinating and under-studied in terms of both narrative and data. [Link; 71 page PDF]

Climate

A World Without Clouds by Natalie Wolchover (Quanta)

One of the many possible positive feedback loops that are still completely beyond the comprehension of climate scientists are clouds, which have the potential to exacerbate climate change as the planet warms. [Link]

Old Is New

Wind-Powered Cargo by Lucy Bellwood (The Nib)

A history of shipping technology and a story about the entrepreneurs who are trying to return to wind-powered ocean transport. [Link]

Skyscrapers Made of Wood Are Making a Comeback by Jen Skerritt (Bloomberg)

Advances in durability and flame resistance are prompting a return to the scene of wooden high-rises, which carry a lower cost thanks to similar unit prices but more efficient labor intensity and lower construction times. [Link; soft paywall]

Luxury

Artist Damien Hirst unveils the most expensive hotel suite ever at $200,000 for TWO nights with a private pool overlooking the Vegas Strip and 24-hour butler – but only high rollers can reserve the villa by Ryan Parry and James Desborough (Daily Mail)

Care to drop the price of a small house on two nights in the lap of luxury at the Palms Casino in Las Vegas? We’ve got just the thing for you. [Link; auto-playing video]

Fraud

Financier Who Amassed Insurance Firms Diverted $2 Billion Into His Private Empire by Mark Maremont and Leslie Scism (WSJ)

A North Carolina insurance mogul has amassed a massive fortune thanks to loans from his insurance companies, creating risks for his policyholders. [Link; paywall]

Fox Rocked by $179M ‘Bones’ Ruling: Lying, Cheating and “Reprehensible” Studio Fraud by Eriq Gardner (The Hollywood Reporter)

A California judge passed down a rather dramatic ruling this month that gave an award of $179mm to rightsholders of the detective show Bones; they had been bilked out of millions in income by below-cost sales of the show to other businesses controlled by the same company. [Link]

Literature

Book Written by Detainee via WhatsApp Gets a Top Prize by Isabella Kwai and Livia Albeck-Ripka (NYT)

An asylum-seeker detained by the Australian government has been given a 125,000 AUD reward for a book that he wrote entirely via What’s App messages while in detention. [Link]

Imminent Domain

Many Texans Want a Border Wall Without a Federal Land Grab. That’s Impossible. by Gus Bova (Texas Observer)

While the citizens of the state with the longest stretch of southern border are evenly split about whether a wall with Mexico is a good idea, they’re two-to-one against any wall that uses imminent domain to seize private lands. Of course, the two go hand-in-hand, meaning roughly one-in-six Texans are between a rock and a hard place. [Link]

Tech Dystopia

The Trauma Floor by Casey Newton (The Verge)

Facebook outsources its content moderation to third-party service providers. To say their employees are suffering under the constant deluge of horrific material that gets reported would be understating things quite a bit. [Link]

Remote Work

Liberty Mutual tells over 600 employees to work from home full-time by Greg Ryan (Boston Business Journal)

Instead of paying for office space for employees in Pennsylvania and Indiana, Liberty Mutual is telling them to work from home instead of renting office space for them. [Link]

Read Bespoke’s most actionable market research by joining Bespoke Premium today! Get started here.

Have a great weekend!

The Closer: End of Week Charts — 3/1/19

Looking for deeper insight on global markets and economics? In tonight’s Closer sent to Bespoke clients, we recap weekly price action in major asset classes, update economic surprise index data for major economies, chart the weekly Commitment of Traders report from the CFTC, and provide our normal nightly update on ETF performance, volume and price movers, and the Bespoke Market Timing Model. We also take a look at the trend in various developed market FX markets.

The Closer is one of our most popular reports, and you can sign up for a free trial below to see it!

See tonight’s Closer by starting a two-week free trial to Bespoke Institutional now!

The Bespoke Report — Equity Market Pros and Cons — 3/1/19

This week’s Bespoke Report is an updated version of our “Pros and Cons” edition.

With this report, you’re able to read through it quickly and still get a complete picture of the bull and bear case for US stocks right now. It’s heavy on graphics and light on text, but we let the charts and tables do the talking!

On page two of the report, you’ll see a full list of the pros and cons that we lay out.

To read the Bespoke Report and access everything else Bespoke’s research platform has to offer, start a two-week free trial to one of our three membership levels. You won’t be disappointed!