Bespoke Brunch Reads: 11/17/19

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, join Bespoke Premium for 3 months for just $95 with our 2019 Annual Outlook special offer.

Florida

Florida’s Sunshine and Tax Benefits Beckon Billionaires by Juliet Chung and Joseph de Avila (WSJ)

The wealthiest are trading New York winters for endless summer, but low taxes are almost certainly a bigger impetus for the zip code shifting. [Link; paywall]

Fuel-theft rings fill South Florida roads with ‘moving bombs’ by Mario Ariza (South Florida Sun Sentinel)

The weather is good but the crews stealing fuel and transporting the proceeds in SUVs are a much less wonderful feature of life in South Florida. [Link; auto-playing video]

Economics

Do Ridesharing Services Increase Alcohol Consumption? by Jacob Burgdorf, Conor Lennon, and Keith Teltser (SSRN)

Increasing access to on-demand transportation has led people to imbibe more aggressively as concerns about the need to drive home have disappeared. UberX entry to a market led to a 9% increase in the prevalence of heavy drinking. [Link]

From Plantations to Prisons: The Legacy of Slavery on Black Incarceration in the US by Melissa Rubio (Dropbox)

In her job market paper, the author identifies a link between counties’ dependence on slavery and the black male incarceration rate immediately after the abolition of slavery and through to contemporary times. [Link; 58 page PDF]

The Effect of District Attorneys on Local Criminal Justice Outcomes by Sam Krumholz (SSRN)

Electing nonwhite district attorneys leads to a 10% decline in incarceration, without any significant impact on local crime or arrest rates. In other words, the choice of district attorney has a big impact on how many people are in jail, but little effect on crime rates. [Link]

Legal Drama

Customer: Wine spill on Hermès bag was $30k mistake. Country club: Our waiter should pay by Rodrigo Torrejon (USA Today)

A New Jersey country club is trying to fob off a ridiculous lawsuit from a customer on one of its employers, the latest in a long string of ridiculous workplace suits. [Link; auto-playing video]

He told a kid to slide. Then he got sued. by Steve Politi (NJ.com)

Instructing a player to slide into third base is now grounds for years of lawsuits. It’s hard to imagine it could get more ridiculous than this most recent litigious lunacy from New Jersey. [Link]

How to Conduct Business with Chinese Companies That See a Dark Future by Dan Harris (China Law Blog)

An extremely interesting rundown on the current legal backdrop in China, where the trade war and a slowing economy are provoking a variety of legal activities that can catch customers abroad by surprise. [Link]

Football

Notre Dame Football Sellout Streak Set to End After 46 Years by Sara Marley (Bloomberg)

It’s been a disappointing run for the Fighting Irish, who may fail to sell out a game for the first time since 1973 in a fight against ranked opponent Navy this weekend. [Link; soft paywall]

The Line of Fire by Natalie Weiner (SBNation)

With gun violence reaching into schools, it should be no surprise that football coaches are on the front lines in trying to keep young people safe. [Link]

Algos Gone Wild

IBM hopes to change weather forecasting around the globe using big data and a new supercomputer by Steve Liesman (CNBC)

Weather models are getting an upgrade, with a new model that uses its new supercomputer DYEUS to model weather in 2-mile blocks (one-third to twenty percent of the smallest units in more traditional models). [Link]

AI can predict if you’ll die soon – but we’ve no idea how it works by Donna Lu (New Scientist)

An interesting example of a machine learning technique picking up on something that a traditional evaluation of data can’t: risk of death based on to electrocardiogram data. [Link]

Goldman faces probe after entrepreneur slams Apple Card algorithm in tweets (Reuters)

A widely-followed VC helped spark outrage over the credit limit assignment process for the new Apple credit card that Goldman Sachs issues. [Link]

Hidden Costs, Hidden Benefits

New Report Examines the Impact of Instagram’s Hidden Likes Experiment on Influencer Engagement by Andrew Hutchinson (Social Media Today)

A study found that hiding likes reduced the number of likes for posts across a range of account sizes, consistent with the thesis that removing like totals reduces engagement. [Link]

The move to free stock trading led to a big jump in new accounts for Charles Schwab by Maggie Fitzgerlad (CNBC)

Removing commissions in response to Robinhood, Charles Schwab reported 142,000 accounts opened in October, up 31% MoM as free trading gains traction. [Link]

Investing

Strategists Foresee ‘Boiling Point’. Investors Risk Up. by Christine Idzelis (Institutional Investor)

Investors have pivoted to a very positive outlook that has investors all sorts of nervous. While fund managers are optimistic, their allocations to equities are only at one-year highs. [Link]

Mars

The Curiosity rover detects oxygen behaving strangely on Mars by Ashley Strickland (CNN)

A strange seasonal pattern of oxygen levels has been picked up by the Curiosity rover on Mas, which may point to a variety of new geological possibilities. [Link]

Renewables

Wind Turbines Are Getting Wild by Caroline Delbert (Popular Mechanics)

A new superconducting material is offering possibilities for wind turbines that would result in dramatic efficiency gains and lowered costs. [Link]

Read Bespoke’s most actionable market research by joining Bespoke Premium today! Get started here.

Have a great weekend!

The Closer: End of Week Charts — 11/15/19

Looking for deeper insight on global markets and economics? In tonight’s Closer sent to Bespoke clients, we recap weekly price action in major asset classes, update economic surprise index data for major economies, chart the weekly Commitment of Traders report from the CFTC, and provide our normal nightly update on ETF performance, volume and price movers, and the Bespoke Market Timing Model. We also take a look at the trend in various developed market FX markets.

The Closer is one of our most popular reports, and you can sign up for a free trial below to see it!

See tonight’s Closer by starting a two-week free trial to Bespoke Institutional now!

The Bespoke Report Newsletter — 11/15/19

This week’s Bespoke Report newsletter is now available for members.

A persistent rally in US equity indices has continued this week, with equity markets at all-time highs in the US and confirming price action from other global indices. We take a look at economic data, technicals, and the earnings backdrop in the US and Europe. We also review commodity and credit markets as well as many other topics in this week’s Bespoke Report newsletter. To read the report and access everything else Bespoke’s research platform has to offer, start a two-week free trial to one of our three membership levels. You won’t be disappointed!

Sluggish Manufacturing in the New York Region

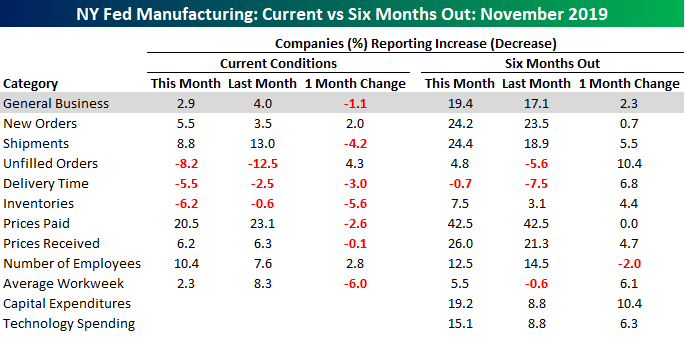

This morning saw one of the first looks at November activity with the NY Fed Empire Manufacturing report. Economists weren’t expecting much of a strong report to begin with as the consensus forecast for the headline General Business Conditions index was for a reading of 6.0 vs last month’s reading of 4.0. The actual reading actually showed a slight decline from last month, though, falling to 2.9. While the current conditions index declined, expectations actually saw a small boost rising from 17.1 up to 19.4.

One interesting thing to note is how little Empire Manufacturing has changed in recent months. With monthly readings of 4.3, 4.8, 2.0, 4.0, and now 2.9, the index has had a five-month range of just 2.8 points. In the history of the survey dating back to 2001, the only five-month window with a narrower range was in late 2011!

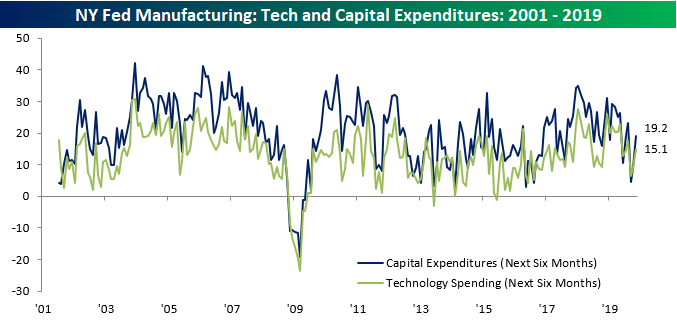

In terms of plans for Capital Expenditures and Technology Spending over the next six months, it was encouraging to see both of these readings rebound after falling sharply in recent months.

Finally, the table below shows the month/month change for each category of the Empire Manufacturing report in terms of both current conditions and expectations. What’s interesting to note about this month’s data is that while there was broad-based weakness in terms of current conditions, expectations rebounded, suggesting that manufacturers are expecting an upturn from current conditions. Sign up for Bespoke’s “2020” special and get our upcoming Bespoke Report 2020 Market Outlook and Investor Toolkit.

Bespoke’s Morning Lineup – 11/15/19 – Retail Sales Friday

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

The Closer – Wal-Mart Reversal, Volatile Fed, Transportation, Iron, Fund Flows – 11/14/19

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, we begin with a look at what Wal-Mart’s (WMT) intraday reversal means for the stock as well as how consumer staples and other defensives have lagged recently. Next, we look into the relationship between the Fed’s balance sheet and volatility before moving onto today’s economic data including freight volumes, EIA data, and ICI Fund Flows.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

Cisco (CSCO) Deja Vu

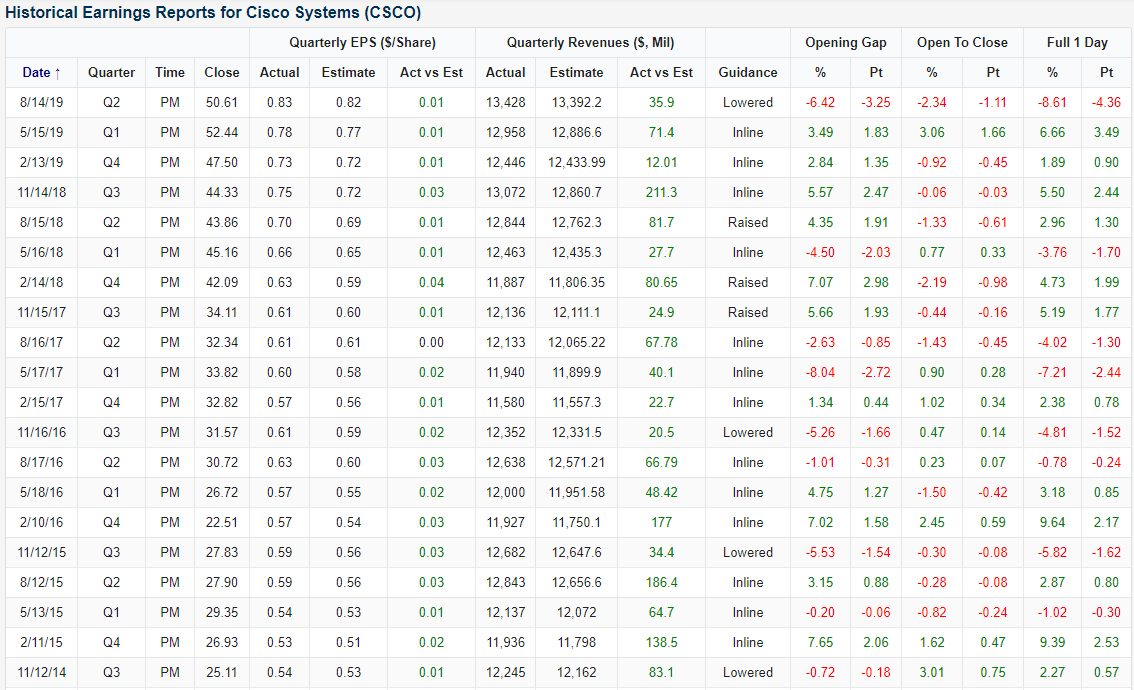

Call it deja vu, but Cisco (CSCO) is seeing a repeat of its August earnings report. Back in the summer, CSCO beat on the top and bottom line but lowered guidance leading the stock to fall 8.61% the following day. Fast-forwarding to today, CSCO reported after yesterday’s close with the same results. The company once again lowered guidance while beating EPS by 3 cents and revenues by $69.4 million. Although the stock’s performance in response has not been quite as bad as last time around, CSCO fell over 7% on Thursday. That is the worst single-day performance for the stock since its last earnings report. Two quarters in a row now, CSCO has fallen substantially on earnings. That is quite the difference from the previous four quarters when the stock rose each time.

Last Monday, we highlighted Cisco (CSCO) in a Dividend Stock Spotlight noting that although it has an attractive dividend, the technical picture was mixed with the stock at a bit of a crossroads at the bottom of a longer-term uptrend thanks to a rough-looking shorter term. The past few months’ declines have come following the aforementioned earnings report in August and a weak quarter from competitor Arista Networks (ANET) further dampening the outlook for CSCO. These catalysts since the summer in conjunction with today’s declines have brought the stock under support between $45-46 and also broken the longer-term uptrend that had been in place over the past few years. Since it’s high on July 15th, CSCO has declines more than 22% and shed $42.8 billion in market cap. To put that into perspective, that decline is within $1 bn of the current market caps of Advanced Micro Devices (AMD), Humana (HUM), Progressive (PGR), and Marriott Hotels (MAR). Start a two-week free trial to Bespoke Institutional to gain full access to our research and interactive tools.

Shrinking Ranges

In the S&P 500’s run to new highs over the last few weeks, overall volatility has really become subdued. For example, the S&P 500 hasn’t had an intraday swing of even 1% in more than a month now. The chart below shows streaks over the last ten years where the S&P 500 didn’t see a 1% spread between its intraday high and low and allows us to compare how the current streak stacks up to prior periods.

While the current 24 trading day streak without a 1% intraday move is far from the longest over the last ten years, there haven’t been a lot of streaks that were longer. Ironically enough, the three streaks that were the longest of the last ten years all occurred in the two years after the 2016 election. For all the turmoil that seems to surround this Administration, market turmoil hasn’t been one of them. Sign up for Bespoke’s “2020” special and get our upcoming Bespoke Report 2020 Market Outlook and Investor Toolkit.

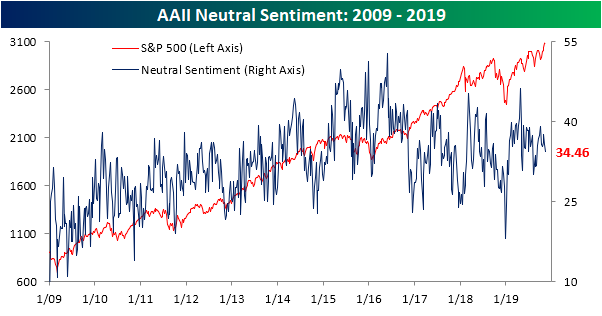

Sentiment Stays the Same

Despite a couple closes at all-time highs in the past week, the S&P 500 is currently right around the same levels as last Wednesday’s close. With little in the way of price changes, sentiment has likewise seen little change. Per AAII’s weekly survey, bullish sentiment rose just 0.42 percentage points to 40.72% from 40.30% last week. That small increase is in the bottom 5% of all week-over-week changes in bullish sentiment in the history of the data.

While little changed, the bulk of investors are still optimistic. Another sentiment survey from Investors Intelligence also echoed these results. In that survey released yesterday, 57.6% reported as bullish. While that is the highest reading since July, it is up only around half of one percent from last week.

Bearish sentiment was also little changed. The percentage of investors reporting as pessimistic rose 0.89 percentage points to 24.82%. Like bullish sentiment, the one week change in bearish sentiment was small relative to history with this week’s change sitting in the 7th percentile of all readings. This week also marked the fourth in a row that bearish sentiment has been below its historical average. That is the longest such streak since a seven-week run from the end of March to early May of this year.

Neutral sentiment moved the most this week falling 1.31 percentage points. Now at 34.46%, neutral sentiment is the lowest since early September and back in the middle of the past few years’ range. Start a two-week free trial to Bespoke Institutional to access our interactive economic indicators monitor and much more.

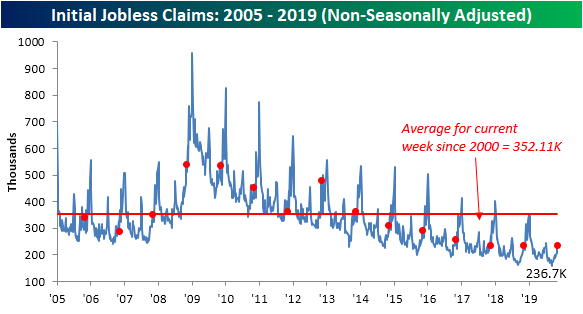

Jobless Claims on the Rise

As we have mentioned over the past couple of weeks (see here and here), initial jobless claims have not done much over the past year as the indicator has been rangebound with an increasingly tighter range. That dynamic shifted a bit this week as claims came in worse than expected, rising to 225K from 211K last week versus forecasts of 215K.

While the record streaks at or below 300K and 250K are still in place by a healthy margin (those streaks now reaching 245 and 110 consecutive weeks long, respectively), this week marked a considerable break out from the upper end of the past several months’ range. This week was also the sixth highest reading for claims of 2019 and the highest since June 21st when claims were 4K higher. The 14K increase from last week was also the joint thirteenth largest one week increase of the past five years and the largest since April when claims rose by 37K right around the Easter holiday (the second-largest such increase of the past five years).

Given the new high in the seasonally adjusted data, the four-week moving average ticked higher to 217K from the previous reading of 215.25K. At 217K, the moving average is now the highest since July 12th when it was 218.75K. Despite this move higher, unlike the seasonally adjusted number, this increase did not break the moving average out of its recent range.

On a non-seasonally adjusted basis, claims rose by 31.1K to 236.7K. That is a slightly smaller change than the average change (+36K) for the current week of the year (45th) over the past ten years. Given these seasonal factors, it was also the largest one week increase to the non-seasonally adjusted data of 2019 and marked a 0.7K increase from the same week last year.

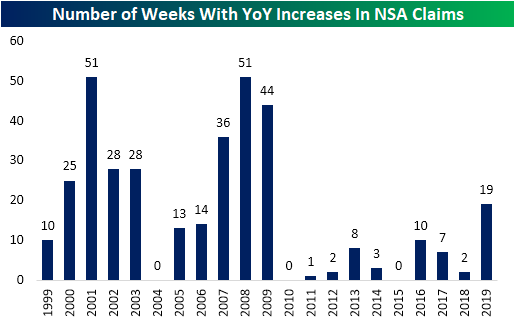

As we have mentioned in the past, 2019 has seen a big increase in the number of weeks with a year-over-year increase in the non-seasonally adjusted data. So far this year there have been a total of 19 weeks were claims have risen YoY. Given there are only 7 weeks left in 2019, it won’t be possible to reach similar levels to the financial crisis, but 2019 has seen the highest frequency these weeks for all years of the current cycle. One interesting point to note though is that weeks with these types of changes in claims have also been subdued in the years following the last recession. As shown in the chart below, of the past 20 years, the years prior to 2009 would typically see a high number of weeks with an increase versus the prior year, but that has simply not been the case from 2010 on. That is, until this year. Start a two-week free trial to Bespoke Institutional to access our interactive economic indicators monitor and much more.