The Closer – No News Is Good News – 12/02/19

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, given the impact trade headlines have had on the market in the past year, we begin with a look at how little tariffs have been mentioned in the news recently. We also show the rare simultaneous movements of stocks, rates, and the dollar. Next we make note of where global manufacturing activity stands and what it means for the economy and forward equity returns. We finish with a review of today’s construction spending data.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

After Hours vs. Regular Trading Hours

The S&P 500 tracking ETF (SPY) is up roughly 25% year-to-date. But below we have broken out SPY’s 2019 move by after hours versus regular trading hours. The “after hours” strategy represents SPY’s move outside of regular trading hours — its change from the prior day’s close to the current day’s open. Given that most major events that impact the stock market occur outside of regular trading hours from 9:30 AM ET to 4 PM ET (like earnings reports, economic indicator releases, and anything that occurs in Asia or Europe before the US opens for trading), SPY nearly always opens at a different price that it closed at the prior trading day. When you see S&P 500 futures trading up significantly in pre-market trading, SPY’s opening price at 9:30 AM ET is going to be a lot higher than the price it closed at the prior day. When equity futures are down in pre-market trading ahead of the opening bell, it means SPY will open lower that day.

Conversely, the “regular trading hours” strategy represents SPY’s move from its opening price at 9:30 AM ET to its closing price at 4 PM ET. This strategy shows how well the stock market is performing on an intraday basis. When you combine the “after hours” move with the “regular trading hours” move, you get SPY’s full-day change from its prior close to that day’s close.

Below we show how well an investor would have done this year by just owning SPY after hours versus just owning SPY during regular trading hours. As shown, had you bought SPY at the close every day and sold it at the next day’s open, you would have a gain of 11.1%. On the other hand, if you did the opposite and bought at the open every day and sold at the close, you’d be up 12.3%.

Interestingly, the “regular trading hours” strategy started the year extremely strong, making up essentially all of the market’s gains over the first three months of the year. During that time period, the “after hours” strategy was essentially flat, which means SPY was opening flat and then seeing a lot of intraday buying.

During Q2 and Q3, there was a lot of back and forth with the “after hours” strategy. During periods when the trade war was really hot, we saw a lot of lower opens, but that stopped once the trade rhetoric cooled down. As shown, since the beginning of August, we’ve seen the “after hours” strategy go from up 0% YTD to up 11% YTD. Over the same time period, we’ve seen the “regular trading hours” strategy trade lower, although it’s up a little over the last two months. This has caused the two strategies to converge to near even on a year-to-date basis as we approach year-end.

if we run the strategy back to the start of 2018, the “after hours” strategy is still crushing the “regular trading hours” strategy. As shown below, had you bought at the close every trading day and sold at the next open, you’d be up 25.6% since the start of 2018. Had you instead just bought every open and sold at the close, you’d actually be down 7%. This means that more than 100% of the S&P’s gain over this time period has come outside of regular trading hours. Start a two-week free trial to Bespoke Institutional to access our research reports, interactive tools, and more.

Warren’s Loss is Health Care’s Win

From late summer through mid-November, betting markets (electionbettingodds.com) gave Senator Elizabeth Warren a considerable lead in the Democratic primary race. In fact, from late September through mid-October, betting markets gave her around a 50/50 shot at winning the primary. While there have been other spikes of interest in certain candidates like for Harris in July and Bloomberg more recently, no other candidate has been given the same type of high win probability at any point in the past several months. With that said, no other candidate has seen the type of fall from grace that Warren has either. As Warren’s policies and tactics like a wealth tax, attacks on billionaires, and health care reform have come under increased scrutiny, betting markets have retreated in their pricing in of a win for the senator. Warren’s probability to win the Democratic nomination is now down to just 16.5%. That is a 36.4 percentage point drop from the high. The only comparable decline is the 32.2 percentage point fall from the high for Senator Kamala Harris. This decline has led markets to give both Mayor Pete Buttigieg and former Vice President Biden higher chances of winning than Warren.

Taking a look at more primary data, this time from the Morning Consult’s weekly survey of Democratic Primary voters, Warren’s falling out of favor has been less dramatic but is in place nonetheless. After her favoritism among Democratic primary voters was on the rise consistently all year, it peaked out at 21% and has been rapidly declining over the past few weeks while Sanders and other candidates who have held a smaller share of votes, namely Buttigieg, have been on the rise.

Warren’s costly Medicare For All plan would essentially put private sector health insurers out of business. Her rise in the polls in 2019 did major damage to the insurers, and that held back the broad Health Care sector ETF (XLV) as well. That’s why Warren’s fall in the polls recently has gone hand-in-hand with a sharp rally for the Health Care sector, as shown in the second chart below. Start a two-week free trial to Bespoke Institutional to access our research reports, interactive tools, and more.

Manufacturing ISM-iserable

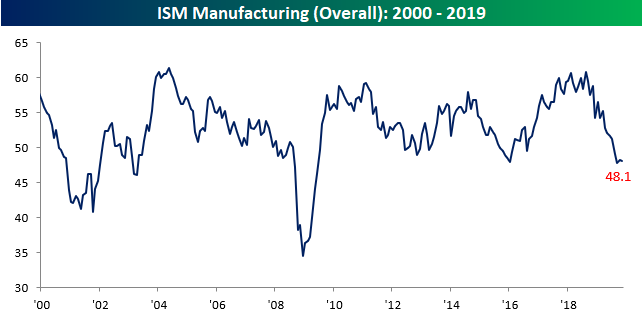

Manufacturing activity contracted more than expected last month as the ISM Manufacturing report for November came in weaker than expected. While economists were expecting the headline index to come in at a level of 49.2, the actual reading was 48.1, which was a slight decline from October’s reading of 48.3. While November’s reading didn’t mark a new short-term low for the ISM Manufacturing index, it’s not far from September’s low of 47.8.

Breadth in this month’s report was also weak. Of the report’s ten subcomponents, six declined on a m/m basis while four increased, but all but one are still in contraction territory for the fourth straight month, which is a trend we haven’t seen since late 2008/early 2009. The biggest increases this month were in Imports and Production, while Inventories showed the largest declines. Looking at the changes in each component relative to last year at this time, though, shows how quickly conditions have changed as all but one (Customer Inventories) are down on a y/y basis.

Two charts we wanted to highlight individually are Employment and Prices Paid. In the case of Employment, that component dropped to 46.6, which is still modestly above the recent low of 46.3 in September. Even still, this doesn’t bode particularly well for Friday’s employment report. More important to watch, though, will be the ISM Services report on Wednesday.

Similar to Employment, Prices Paid also turned back lower this month and is right near its recent lows. This indicator serves as a reminder that inflation readings are still showing no signs of accelerating to the upside. That coupled with the fact that the Fed has suggested on multiple occasions that it is willing to remain on hold until well after inflation rates reach or exceed their target levels indicates that any rate hikes by the FOMC are a way off. Sign up for Bespoke’s “2020” special and get our upcoming Bespoke Report 2020 Market Outlook and Investor Toolkit.

A Better Than Average Decade

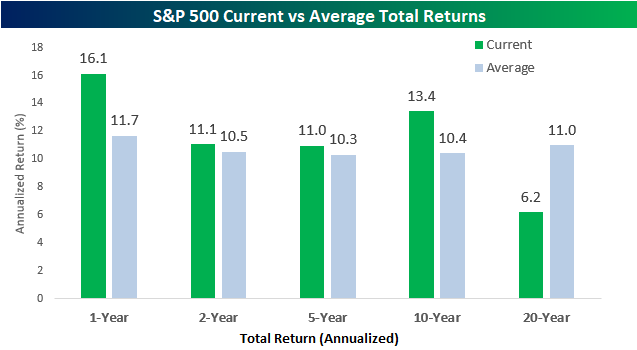

The S&P 500 rallied 3.6% on a total-return basis in November, which was the best monthly return for the index since June but surprisingly only the fourth-best month so far in 2019. That’s how strong equities have been this year! This November was also the best November for the S&P 500 since 2016 after President Trump was elected. While the S&P 500 is currently up 27.6% YTD on a total return basis, over the last 12 months, the index is ‘only’ up 16.1%. That’s how bad last December was!

The chart below compares the S&P 500’s annualized returns over the last one, two, five, ten, and twenty years to the average annualized returns of the index for each time period since 1928. The S&P’s current one-year return is already well above its historical average of 11.7%, and barring a major decline in December, this number will be even more skewed a month from now. While the one-year gain is well above average, both the two and five-year annualized returns are actually pretty much right in line with the historical averages.

Longer-term is where the current returns relative to average are really skewed. Over the last 10 years, the S&P 500’s average annualized return of 13.4% is a full three percentage points higher than average. That may not sound like an enormous difference, but over time it adds up; 13.4% compounded over 10 years works out to a cumulative gain of 252% whereas 10.4% compounds to just 169%. While 10-year returns are well above their historical average, returns over the last 20 years have been well below average at 6.2% vs 11.0%. A three percentage point difference adds up over 10 years, but a spread of five percentage points over a 20-year period is enormous. While one could expect to multiply their original investment by seven times if it compounded at 11% annually over a 20-year period, that same investment wouldn’t even multiply by 2.5 times at a rate of 6.2%!

The chart below ranks the S&P 500’s current one, two, five, ten, and twenty-year returns on a percentile basis versus all other periods. Interestingly, the S&P 500’s current one-year performance only ranks in the 58th percentile relative to all other 12-month periods, and the two and five-year returns are both slightly below the 50th percentile. The real extreme, though, is in the S&P 500’s 20-year performance which ranks in just the 5th percentile of all other 20-year periods in the index’s history. As good as the last decade has been for bulls, the decade before was truly treacherous. Sign up for Bespoke’s “2020” special and get our upcoming Bespoke Report 2020 Market Outlook and Investor Toolkit.

![]()

Above Average Volumes on a Low Volume Day

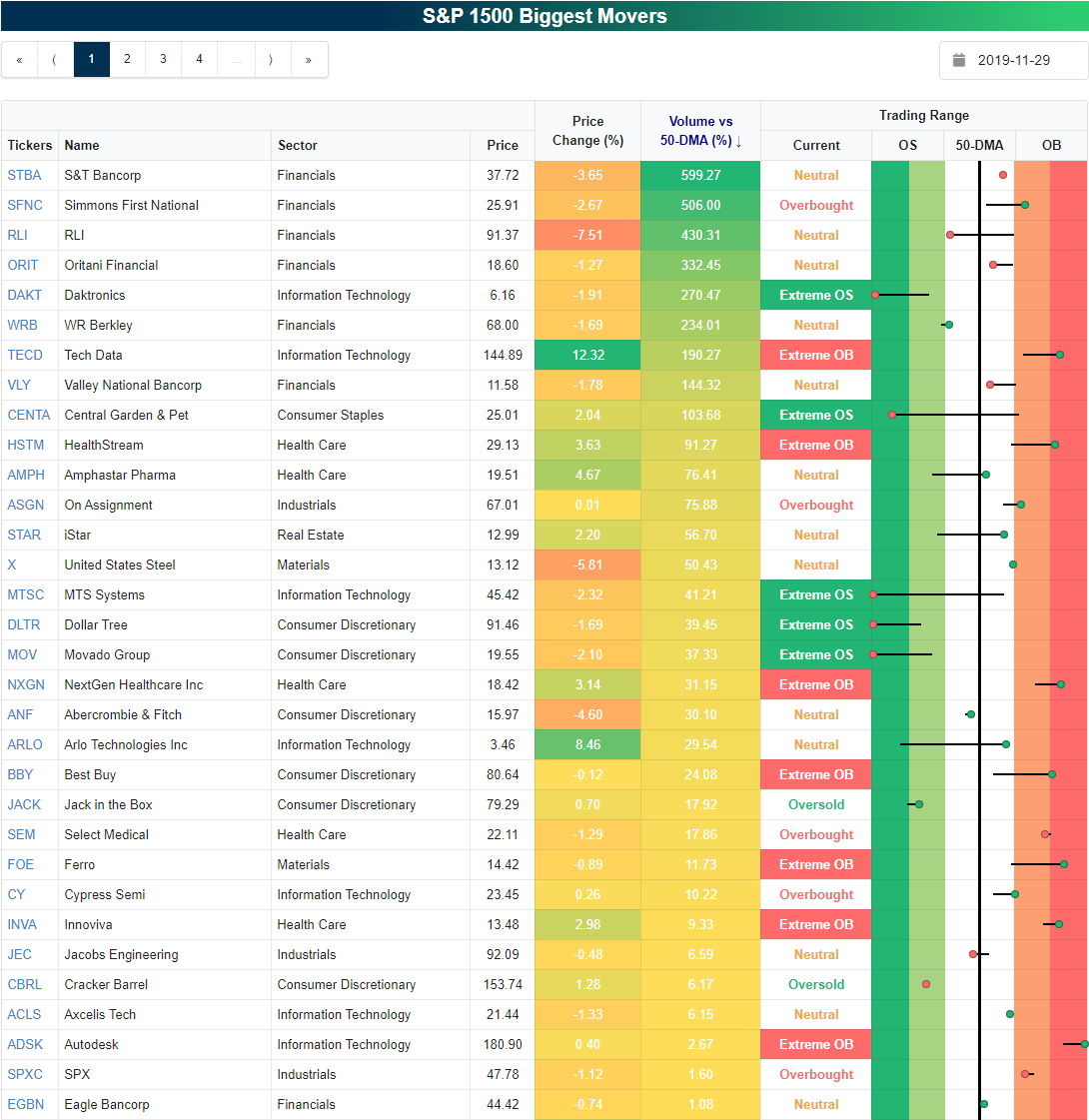

As could be expected due to the shortened session following the Thanksgiving holiday, volumes were very light on Friday. For the S&P 500 (SPY) which declined 40 bps, volumes on Friday were just 62.7% of the 50-day average. In the S&P 1500, there were just 32 stocks that saw above-average volumes. Below is snapshot of them from our Biggest Movers tool, which traders use daily to see the S&P 1500 stocks that rose and fell the most, the highest/lowest volumes relative to their 50-DMAs, and overbought and oversold levels.

Of the 32 stocks that saw above-average volumes on Friday, Tech Data (TECD) rose the most with a 12.32% gain. It was also the best performing stock of the entire S&P 1500 index on Friday. Arlo Technologies (ARLO) also surged on Friday rising more than 8%. While TECD is now extremely overbought with this move, ARLO is not even one standard deviation from its 50-DMA as it was coming off of extremely oversold levels. On the other hand, RLI (RLI) fell the most of the stocks that saw above-average volumes. While TECD was the best stock in the index, RLI was the fourth worst. Most other high volume stocks on Friday experienced more modest price changes.

While RLI and TECD were some of the biggest movers, they also saw elevated volumes of double or more their 50-day average. Other stocks that saw similarly elevated volumes include: S&T Bancorp (STBA), Simmons First National (SFNC), Oritani Financial (ORIT), Daktronics (DAKT), WR Berkley (WRB), Valley National Bancorp (VLY), and Central Garden & Pet (CENTA). Start a two-week free trial to Bespoke Institutional to access our Biggest Movers page and the rest of our popular interactive investor tools.

Bespoke’s Morning Lineup – 12/2/19 – Futures Fading

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

Bespoke Brunch Reads: 12/1/19

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, join Bespoke Premium for 3 months for just $95 with our 2020 Annual Outlook special offer.

Education

The price you can’t pay by Myles Udland (I’m Late To This)

An analysis of why the college admissions scandal that broke earlier this year hit home so hard and was so inevitable given the specific segment of society that it broke from. [Link]

Big Calculator: How Texas Instruments Monopolized Math Class by Maya Kosoff (Medium)

Do you ever wonder why the standard equipment for high school math classes hasn’t changed in decades? It won’t surprise you to discover huge profits behind pricey calculators. [Link]

Tech Mixed-topia

Alexa, Are You Disappointed in Me? Amazon’s Voice Gets More Range by Matt Day (Bloomberg)

While the core functionality of the Alexa voice assistant won’t change, how it speaks to you is getting an expanded range in its latest update. [Link]

Mass. State Police Tested Out Boston Dynamics’ Spot The Robot Dog. Civil Liberties Advocates Want To Know More by Ally Jarmanning (WBUR)

Police in Massachusetts are using a Boston Dynamics robot in tests with their bomb squad, raising questions about the deployment of robotic tools by police forces. [Link]

Economics

A charity dropped a massive stimulus package on rural Kenya — and transformed the economy by Dylan Matthews (Vox)

A summary of new research studying large gifts of cash to the poor in East Africa: obviously there were positive impacts on recipients but there were also large multipliers and limited inflation effects, adding to the overall benefits of the transfers. [Link]

Giving Thanks for Property Rights by Caroline Baum (E21)

Forgive some of the hyperbolic language, because this account of how private property rights helped cement the Plymouth Colony in New England is worth a read. [Link]

Sports

Wall Street Wades Into Sports Gambling as Legalization Spreads by Annie Massa (Bloomberg)

With live legal sports betting spreading across the country, markets hawks are gearing up to dump capital into the evolving market. [Link; soft paywall]

Podcasts

The pod delusion by Matt Labash (Spectator)

Polemic against the spreading scourge of audio content that has come to dominate both the media and the personal lives of many would-be hosts. [Link]

Weather

The weather is big business, and it’s veering toward a collision with the federal government by Andrew Freedman (Greenwich Time/WaPo)

With falling costs to launch satellites and crunch data, private weather forecasters are now competing with NOAA to provide detailed weather information and warnings. [Link; auto-playing video]

Read Bespoke’s most actionable market research by joining Bespoke Premium today! Get started here.

Have a great weekend!

The Closer: End of Week Charts — 11/29/19

Looking for deeper insight on global markets and economics? In tonight’s Closer sent to Bespoke clients, we recap weekly price action in major asset classes, update economic surprise index data for major economies, chart the weekly Commitment of Traders report from the CFTC, and provide our normal nightly update on ETF performance, volume and price movers, and the Bespoke Market Timing Model. We also take a look at the trend in various developed market FX markets.

The Closer is one of our most popular reports, and you can sign up for a free trial below to see it!

See tonight’s Closer by starting a two-week free trial to Bespoke Institutional now!

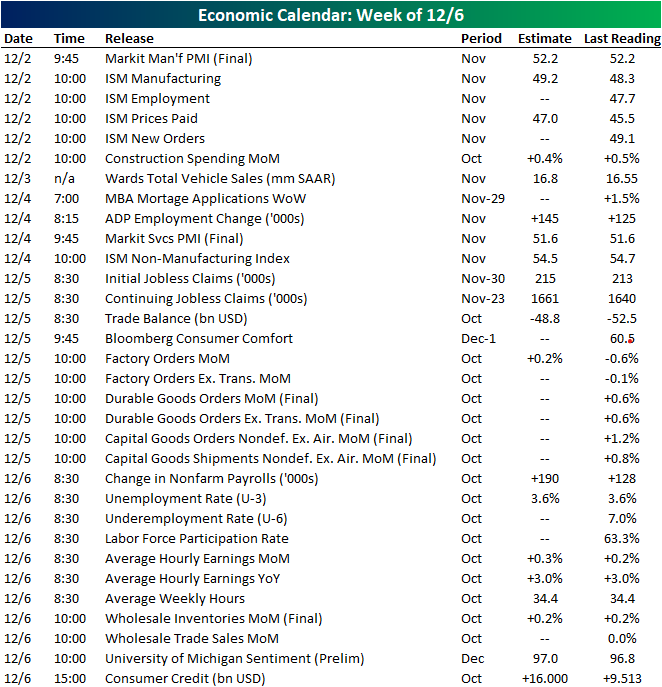

Next Week’s Economic Indicators – 11/29/19

Even with a holiday and a shortened session Friday leaving no US releases in the past 48 hours, it was a very busy week for economic data with 36 releases in the first three days. Most of this data came in stronger than expected or above the prior reading where there were no forecasts. While the bulk of the week’s data was strong, manufacturing data, namely from the regional Fed indices, was mixed. We started off with a weaker Chicago Fed National Activity Index on Monday. The index fell from -0.45 last month to -0.71 rather than the expected improvement to -0.2. The Dallas Fed’s index was also out on Monday and it improved more than expected as well as versus the prior month. On Tuesday, the Richmond Fed’s gauge on manufacturing was also worse than expected. On the bright side, other manufacturing hard data like durable goods came in much stronger than both the previous month and consensus forecasts. Housing data was also solid this week with better than anticipated home price growth shown in two of the three indicators: the quarterly Home Price Purchase Index, FHFA, and Case-Shiller (only the Case-Shiller index was weaker than expected, albeit up from the prior month). The second release of third-quarter GDP was the most notable indicator of the week with a much stronger than expected reading which showed the economy grew by 2.1% QoQ versus estimates of a 1.9% growth rate.

We kick off December with another busy few days next week. Final November Markit and ISM numbers will kick off the week on Monday. While Markit is not expecting any change from the preliminary readings, ISM is expected to improve to 49.2 which would still be a contractionary print. In hard manufacturing data, later in the week we will see final durable and capital goods numbers for November. Vehicle sales figures will be the only release on Tuesday followed by the service counterparts to Markit and ISM indices on Wednesday as the rest of the week’s main focus will be on labor data. After a surprisingly strong release last month, Nonfarm Payrolls is again expecting a strong print showing 190K jobs created in the month of November. Start a two-week free trial to Bespoke Institutional to access our interactive economic indicators monitor and much more.