Boeing (BA) Sends the Dow Flying

Turnaround Tuesday has carried into hump day with the Dow up well over 5% again today as of this writing. As we mentioned in an earlier post, that means the Dow is on track for its first back-to-back up days for the first time since early February. Remarkably, even with only two consecutive up days, the index is closing in on exiting a bear market. For that to happen, the Dow would need to close above the 22,310.32 level which is 20% off of the bear market closing low (Monday’s close at 18,591.93). At today’s high, the Dow was less than 300 points or 1.32% from that level.

As for the individual stocks contributing to the rally, Boeing (BA) deserves a lot of thanks. The stock has been hit very hard during the sell-off. Whereas the stock has traded in the mid-$300 for much of the past two years and up to mid-February, as of late last week BA had fallen below $100. That massive drop in price means that day to day movements in the stock would have a lesser impact on the level of the price-weighted Dow. In spite of this, BA has contributed over 400 points to the Dow’s rally in the past two days alone! That is much more than any other stock in the index with the next biggest contributor being UnitedHealth (UNH) who’s 335.44 point contribution comes as its share price is currently around $100 more than BA. BA’s contribution is also almost 200 points more than those of McDonald’s (MCD), Visa (V), and Apple (AAPL). Of all 30 Dow stocks, there is only one that is down over the past couple of days, subtracting from the index’s rally: Walmart (WMT). Given WMT has held up fairly well recently, its performance is yet another example of investors’ focus on the more beaten down names that we have noted earlier today and in last night’s Closer. Start a two-week free trial to Bespoke Institutional to access Closer and full range of research and interactive tools.

Fixed Income Weekly – 3/25/20

Searching for ways to better understand the fixed income space or looking for actionable ideas in this asset class? Bespoke’s Fixed Income Weekly provides an update on rates and credit every Wednesday. We start off with a fresh piece of analysis driven by what’s in the headlines or driving the market in a given week. We then provide charts of how US Treasury futures and rates are trading, before moving on to a summary of recent fixed income ETF performance, short-term interest rates including money market funds, and a trade idea. We summarize changes and recent developments for a variety of yield curves (UST, bund, Eurodollar, US breakeven inflation and Bespoke’s Global Yield Curve) before finishing with a review of recent UST yield curve changes, spread changes for major credit products and international bonds, and 1 year return profiles for a cross section of the fixed income world.

In this week’s report we review corporate issuance.

Our Fixed Income Weekly helps investors stay on top of fixed income markets and gain new perspective on the developments in interest rates. You can sign up for a Bespoke research trial below to see this week’s report and everything else Bespoke publishes free for the next two weeks!

Click here and start a 14-day free trial to Bespoke Institutional to see our newest Fixed Income Weekly now!

Come on Dow, You Can Do It!

The way things have been moving on a minute to minute basis, nothing is guaranteed in this market, but the way things stand now, the Dow is on pace to break its streak of days without back to back daily gains at 32 trading days. That’s right, not since February 6th have we seen the Dow finish the day in positive territory for more than a day at a time. Looking back throughout history, there have only been a handful of other periods where the DJIA went this long or longer without two up days in a row. The last occurrence was all the way back in 1984, and before that, you have to go back to 1969. Other than those two streaks, there were also two other periods in 1931 where the DJIA went more than 30 trading days without back to back gains. While the current streak ranks as tied for the fourth-longest on record, if the DJIA isn’t able to hold onto its intraday gains today, the current streak will extend out to a minimum of at least two trading days and that would move the current streak into second place overall. Start a two-week free trial to Bespoke Institutional to access our Custom Portfolios, interactive tools, and full library of research.

Dash For Trash

Yesterday, the S&P 500 had one of its best days on record and the best day since 2008 as the index soared nearly 10%. As we noted in last night’s Closer, for stocks that have been hit the hardest during the past month’s equity rout, yesterday’s buying spree was a very welcome sign. Yesterday saw a massive “dash for trash” as the current bear market’s worst performers were the best performers in yesterday’s session. The average stock in the bottom 10% of performers over the course of the current bear market dating to February 19th was up an astonishing 18.1%. All five of the bottom deciles in the distribution of returns since the bear market began were up at least double-digit percentage points. On the other end of the spectrum, while the best performing stocks were still positive on the day, their rallies were much more muted as the average stock in the best-performing decile only rose 3.38%. Start a two-week free trial to Bespoke Institutional to access nightly Closer and full range of other research and interactive tools

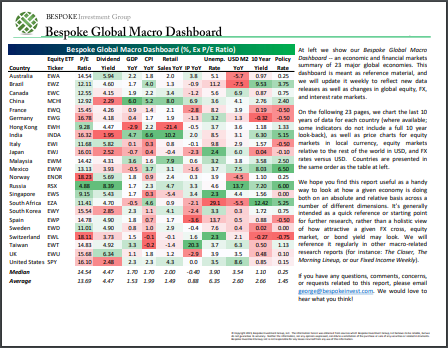

Bespoke’s Global Macro Dashboard — 3/25/20

Bespoke’s Global Macro Dashboard is a high-level summary of 22 major economies from around the world. For each country, we provide charts of local equity market prices, relative performance versus global equities, price to earnings ratios, dividend yields, economic growth, unemployment, retail sales and industrial production growth, inflation, money supply, spot FX performance versus the dollar, policy rate, and ten year local government bond yield interest rates. The report is intended as a tool for both reference and idea generation. It’s clients’ first stop for basic background info on how a given economy is performing, and what issues are driving the narrative for that economy. The dashboard helps you get up to speed on and keep track of the basics for the most important economies around the world, informing starting points for further research and risk management. It’s published weekly every Wednesday at the Bespoke Institutional membership level.

You can access our Global Macro Dashboard by starting a 14-day free trial to Bespoke Institutional now!

Bespoke’s Morning Lineup – 3/25/20 – Volatility Still Reigns Supreme

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

Equity futures are indicating a modestly higher (or lower depending on when you look at the futures) open, but don’t let the numbers fool you. From midnight to around 4:30 eastern, S&P 500 futures rallied more than 4.5% in reaction to news of a deal being struck in DC over the $2 trillion coronavirus relief bill. From 4:30 through now, though, all of those gains have been erased.

Markets are still searching for equilibrium and trying to figure out when the economy will be able to re-open, and right now there is just about zero clarity on that front. Then, when the time comes where certain areas of the country look to be in the clear and can open for business a whole new set of questions will arise. First, how do you cordon off these areas that are no longer hotspots from the areas that are still hot?

Read today’s Bespoke Morning Lineup for a discussion of the details of the relief bill in DC, Asian and European markets, and the latest trends and statistics of the outbreak.

It’s been an exceptionally strong two days for gold as the yellow metal has rallied over 5% on back to back days. With all the liquidity being thrown into the system, some investors are clearly worried about the dollar’s purchasing power down the road. Going back to 1980, there have only been four prior periods where gold has seen similar moves on back to back days, with the last occurrence coming in September 2008. In other words, it has been extremely rare to see these kinds of moves.

The Closer – Epic Dash For Trash Drives Volatility Up – 3/24/20

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, we review what factors drove today’s rally and where that leaves credit markets. We also show other ways that fixed income markets are returning to normal before reviewing today’s 2 year Treasury note auction. We close out tonight with a recap of our Five Fed Manufacturing Composite.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

Warren Buffett Portfolio Check Up

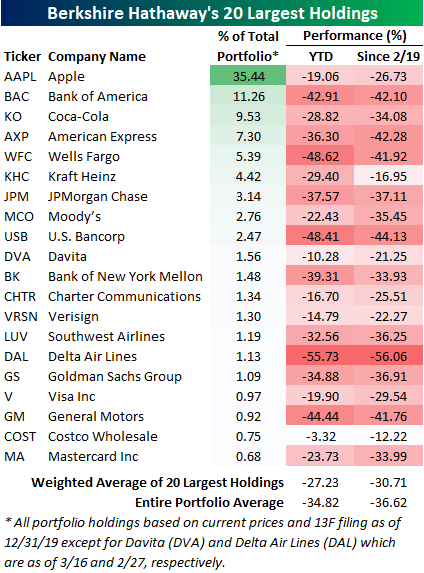

During tumultuous times, investors always turn to the sage advice of the Oracle of Omaha: Warren Buffett. With the S&P 500 down almost 30% from its record high back on February 19th, many are surprised from the silence out of Omaha. While Buffett is well known for weathering the worst market downturns and coming out stronger, the last several weeks have been just as painful on his portfolio as it has on the broader market. Fortunately for him, though, a mountain of cash has helped to cushion the blow of the decline.

Of Berkshire’s top holdings, the average stock is down 36.62% since the S&P 500’s last all-time closing high on 2/19 and down 34.82% YTD. The worst performing of the portfolio’s holdings has unsurprisingly been an energy sector name, Occidental Petroleum (OXY), which is down roughly 75% this year. On the other hand, Amazon (AMZN) has been a top performer in 2020 as it is currently up 3.5% YTD. But neither of these stocks are particularly large holdings. In the table below, we show the 20 largest holdings in the Berkshire portfolio as of the most recent 13F filing (in addition to positions in Davita (DVA) and Delta (DAL) which were added and disclosed more recently). Apple (AAPL) continues to be the crown jewel with a 35.44% weighting in the portfolio. At the S&P 500’s peak, Buffett’s position in AAPL was worth $79.3 bn, but the 26.7% decline since then has brought that value down to $58.13 bn. The next largest position and the only other one taking up a double-digit percentage in the portfolio’s total weight is Bank of America (BAC) which is down even more dramatically at 42%. Other notable weak holdings have been the airlines, Southwest (LUV) and Delta (DAL). For clients with access, we have also created a custom portfolio of Berkshire’s reported equity portfolio so you can track these names. Start a two-week free trial to Bespoke Institutional to access our Custom Portfolios, interactive tools, and full library of research.

Best Performing Russell 3,000 Stocks

The Russell 3,000 is currently down about 35% from its February 19th high. With such a substantial decline in the index in just over one month, it should come as no surprise that only a small handful of individual stocks are higher since the 2/19 peak. In fact, less than 2% of the index has risen in that time. The bulk of these stocks are Health Care names. As shown below, there are 28 Health Care stocks that have risen since 2/19 with two, Tocagen (TOCA) and Vir Biotechnology (VIR) having doubled in price in that time. Sixteen other stocks have seen double digit percentage gains in that time.

Of the stocks that are up in other sectors, many appear to be plays on a socially distanced coronavirus world. For example, in the Consumer Discretionary sector, the best performer has been food delivery and ordering app Waitr (WTRH) which has gone from $0.39 to $1.56. In that same vein, Domino’s Pizza (DPZ) has also performed well. Outside of the Health Care sector, the only sector with a large number of stocks that are up are Consumer Staples. As with many of these other stocks, these seem to be plays on the COVID-19 economy. Multiple grocers, wholesale stores, and food related names make the list alongside cleaning product company Clorox (CLX). Additionally, despite the rout of Energy names, there also are four Energy stocks that have distanced themselves from the pack and risen since 2/19 — TNK, SWN, DHT, EQT. Start a two-week free trial to Bespoke Institutional to access our full range of research and interactive tools.

Bespoke’s Morning Lineup – 3/24/20 – Limited Limits

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

Here we go again. Equity futures were trading on a limit up basis earlier but have since given up some of their gains. As things stand now, the US equity market is still poised to open up by about 4%, but where it goes from there is anyone’s guess. Optimism this morning stems from hopes that both sides of the political divide are closer to a stimulus deal in Washington and that some of the hardest-hit hotspots from the coronavirus are showing varying levels of improvement.

Light at the end of the tunnel in the coronavirus outbreak is obviously important because the sooner we see the light, the closer the US economy will be to moving out of its coma. This has been a contentious topic over the last 24 hours. On the one side, there’s a growing camp voicing concerns over the economic damage of the US and global shutdown. They are calling for at least a plan to be made for when, how, and under what conditions Americans will be allowed to go back to work. On the other side, a number of people argue that it’s still way too early to even start thinking about starting the economy back up as there are many more pressing concerns facing the country.

We’re not quite sure where the disagreement is here. In the words of NY Governor Cuomo, “you have to walk and chew gum in life.” In other words, can’t we address both the pressing Health Care needs facing the country and also start coming up with a plan for how Americans will be able to go back to work when the peak of the outbreak passes? Governments at all levels have come under enormous criticism for being caught flatfooted heading into this outbreak. Now that both Federal and state governments are thinking ahead, though, do they deserve the same criticism now? There are no easy answers in any of this, and no one is looking to get things back up and running if it is only going to make things worse, but that doesn’t mean we shouldn’t be asking the questions and coming up with plans and strategies as new data and treatments come to light.

Read today’s Bespoke Morning Lineup for a discussion of the latest figures in terms of Fed purchases in the last several days, the latest on the competing fiscal stimulus plans, and the latest coronavirus figures.